Retirement portfolio management presents a fundamentally different set of challenges than accumulation-phase investing. The transition from building wealth to distributing it introduces risks that traditional asset allocation frameworks were never fully designed to address. Among the most compelling structural solutions to emerge from decades of practice is the bucketing investment approach, a time-segmented framework that brings discipline, clarity, and behavioral resilience to one of the most complex financial challenges investors face.

This is not a strategy built to chase alpha. It is a risk management architecture designed to protect against three of the most consequential threats to retirement financial security: sequence of returns risk, inflation risk, and longevity risk. Understanding why it works, and why an increasing number of sophisticated advisors and institutional practitioners have adopted it, requires an honest examination of what actually causes retirement portfolios to fail.

The Problem With Conventional Portfolio Construction in Retirement

Traditional asset allocation is built around a deceptively simple premise: blend equities and fixed income in proportions consistent with an investor’s risk tolerance, rebalance periodically, and allow long-term average returns to do the work. In the accumulation phase, this framework is largely sound. In the distribution phase, it carries a critical vulnerability.

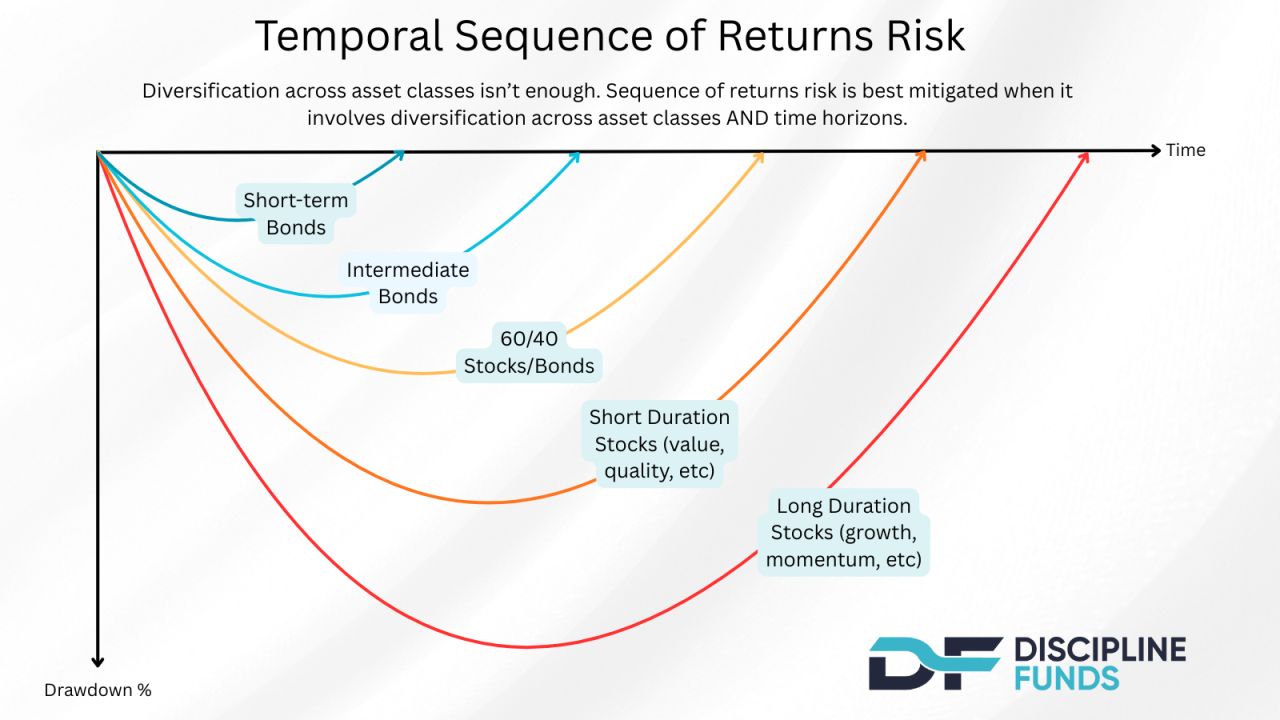

When a retiree begins making systematic withdrawals from a unified portfolio, the sequence of market returns becomes as important, and arguably more important, than the long-term average return itself. A portfolio that suffers significant losses in its early distribution years, while simultaneously funding living expenses, may never fully recover. The mathematics are unforgiving: selling depreciated assets to meet income needs permanently reduces the capital base available to participate in any subsequent recovery.

This is sequence of returns risk, and it is not a theoretical concern. It is the single most common mechanism by which well-constructed retirement portfolios are prematurely depleted. A bucketing framework addresses this vulnerability at its root.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The Architecture of a Bucket Strategy

The bucketing approach segments portfolio assets into distinct pools, or buckets, each defined by its time horizon, purpose, and risk profile. While implementations vary, the foundational structure typically consists of three tiers. Note that these buckets apply across someone’s entire asset base and shouldn’t be viewed as a strategy that can be implemented in a single account alone.

The Short-Term Bucket holds liquid, capital-stable assets sufficient to fund one to four years of living expenses outside of other cash flows in retirement. Money market instruments, short-duration Treasuries, and high-quality cash equivalents are typical holdings, but also checking and savings accounts. This bucket functions as the portfolio’s operational reserve, the source from which withdrawals are funded regardless of what equity markets are doing. Its purpose is not to generate meaningful return. Its purpose is to ensure that no retiree is ever forced to liquidate growth assets at a distressed price.

The Intermediate Bucket serves as the portfolio’s replenishment engine. Allocated to investment-grade fixed income, dividend-producing equities, balanced strategies, and other moderate-return instruments, this tier is designed to generate consistent income and capital appreciation over a three-to-seven-year horizon. When the short-term bucket is drawn down, the intermediate bucket provides the structured refill, transferring assets in a disciplined, rules-based manner rather than reactively.

The Long-Term Growth Bucket is the portfolio’s compounding engine and its primary defense against inflation and longevity risk. Allocated to equities, real assets, and other growth-oriented investments, this tier operates on a time horizon of seven or more years. Because near-term spending needs are fully addressed by the first two buckets, the growth bucket can remain invested through complete market cycles, compounding without interruption and without the forced liquidation that so frequently impairs total-return portfolios during periods of volatility.

Why This Framework Works: The Intersection of Mathematics and Investor Behavior

The analytical case for bucketing is straightforward. By isolating near-term liabilities from long-term growth capital, the strategy eliminates the forced selling that drives sequence of returns damage. Growth assets are given the time they require to recover from inevitable market dislocations. Liquidity is pre-positioned with precision rather than sourced reactively. The result is a portfolio that is structurally more resilient than its unified-pool alternative, not because it generates superior returns in isolation, but because it avoids the value destruction that undisciplined withdrawal sequencing creates.

Yet perhaps the more compelling argument for bucketing is behavioral rather than quantitative. The financial planning literature is unambiguous on this point: a significant proportion of retirement plan failures are not caused by flawed assumptions or inadequate returns. They are caused by investor behavior, specifically the emotionally driven decisions that market volatility provokes in retirees who depend on their portfolios for income.

Bucketing reframes the investor’s relationship with market volatility in a fundamentally important way. When a client understands, viscerally and not just intellectually, that the next 12 to 24 months of income is already set aside in a stable, liquid reserve, the psychological impact of a market correction is meaningfully diminished. The conversation shifts from “my portfolio is down” to “my income is protected while my growth assets recover.” That reframe is not cosmetic. It is the difference between a client who stays the course and one who makes a decision they cannot undo.

Liquidity Management, Tax Efficiency, and Operational Discipline

Beyond its risk management and behavioral merits, a well-implemented bucket strategy delivers meaningful advantages in liquidity planning and tax efficiency, areas that are frequently underweighted in conventional retirement portfolio discussions.

In a unified total-return portfolio, withdrawal sourcing is often reactive and operationally inconsistent. Assets are sold as needed, without systematic consideration of timing, tax lot selection, or the impact on long-term allocation targets. Bucketing introduces intentionality to this process. Cash reserves are established and maintained in advance. Refill policies are defined, typically triggered by strong equity performance, periodic rebalancing events, or predetermined calendar schedules, rather than dictated by short-term market conditions.

This operational discipline creates meaningful downstream benefits. Advisors can source withdrawals from the most tax-advantaged positions available. Rebalancing events become opportunities to replenish lower-risk buckets while trimming appreciated growth positions. The result is a more coherent, more consistent, and more defensible withdrawal strategy across the full retirement horizon.

An Honest Assessment of the Tradeoffs

Intellectual honesty demands acknowledging that bucketing is not without limitations. Holding a meaningful allocation in cash and short-duration instruments introduces a performance drag relative to a fully invested total-return portfolio, particularly in extended bull markets. If the short-term bucket is oversized or the replenishment rules are poorly calibrated, the strategy can sacrifice return without a commensurate reduction in risk. In some scenarios, a highly disciplined total-return approach with systematic rebalancing and pre-defined withdrawal rules may produce comparable long-term outcomes.

The resolution to this tension lies in implementation quality. A well-designed bucket strategy, with appropriately sized tiers, clearly defined replenishment policies, and regular portfolio review, captures the structural advantages of time segmentation without incurring unnecessary performance costs. The framework succeeds not because of the concept alone, but because of the discipline with which it is executed.

The Case for Structural Clarity in an Uncertain Environment

Markets are inherently unpredictable. Retirement horizons are long and growing longer. Inflation is a persistent and underappreciated threat to purchasing power. And investor behavior, even among sophisticated individuals, remains one of the most significant variables in long-term financial outcomes.

The bucketing investment approach does not eliminate these realities. What it does is introduce a structural framework that manages them with greater precision and consistency than most alternatives. By segmenting time horizons with purpose, protecting near-term income needs with appropriate liquidity, preserving long-term growth capital through complete market cycles, and establishing the behavioral scaffolding that keeps investors committed to their plan during periods of stress, bucketing addresses the full complexity of retirement risk in a way that is both analytically sound and practically effective.

For advisors committed to delivering durable outcomes for their clients, and for investors serious about protecting the financial security they have spent a lifetime building, the bucketing framework represents not merely a portfolio construction technique, but a fundamentally more thoughtful approach to the challenge of retirement income management.

By Lewis M. Young, Portfolio Strategist

8971317.1. – 11JUNE26A