There’s always some uncertainty around a new Fed chair and how they’ll handle the communication of monetary policy. But it’s usually more around style rather than substance. In Kevin Warsh’s case, the concern is substance, or lack of it. While 12 FOMC members set policy, the chair plays the central role in explaining the thinking behind decisions and how the Fed would respond under different scenarios. The Fed is ultimately managing two-sided risk: higher unemployment and higher inflation. Markets need confidence that it can do that, especially during a shock.

The chair also clarifies the Fed’s reaction function: what it does, why it does it, and how it responds as the data changes. There is always uncertainty around policy, but ideally that uncertainty comes from the economy, not confusion about how the Fed interprets it.

Warsh just completely disengaged from that framework. By rejecting “forward guidance,” he may be trying not to telegraph the next move, which is reasonable when even Fed officials don’t know the timing. But he also left markets with little sense of the Fed’s reaction function. The uncertainty band around policy just widened, which means more volatility.

Instead, Warsh is focused on creating task forces covering Fed communication, the balance sheet, data, productivity, jobs, and the inflation framework. That is a lot. He’ll be busy building commissions while markets are looking for clarity.

The Fed Holds Rates Steady, but Dot Plot Shows a Hawkish Pivot

The problem is that Warsh is effectively stepping back from leading the Fed, rather than coordinating a consistent message across differing views within the committee. The other 18 Fed officials will keep offering their own interpretations of the data and the Fed’s reaction function, potentially adding to confusion. Who leads now? Which data points take priority? And are markets supposed to look to new private data sources, which may be even less reliable than the public ones?

Case in point: the June meeting.

The Fed held rates steady in the 3.50%–3.75% range, as expected. But Warsh’s new no-guidance approach was obvious in the statement. It was shorter, simpler, and largely limited to what the Fed had just done: leave policy unchanged. That may reduce the risk of overcommitting, but it also strips away useful context. Markets got the decision, but not much of the reasoning behind it.

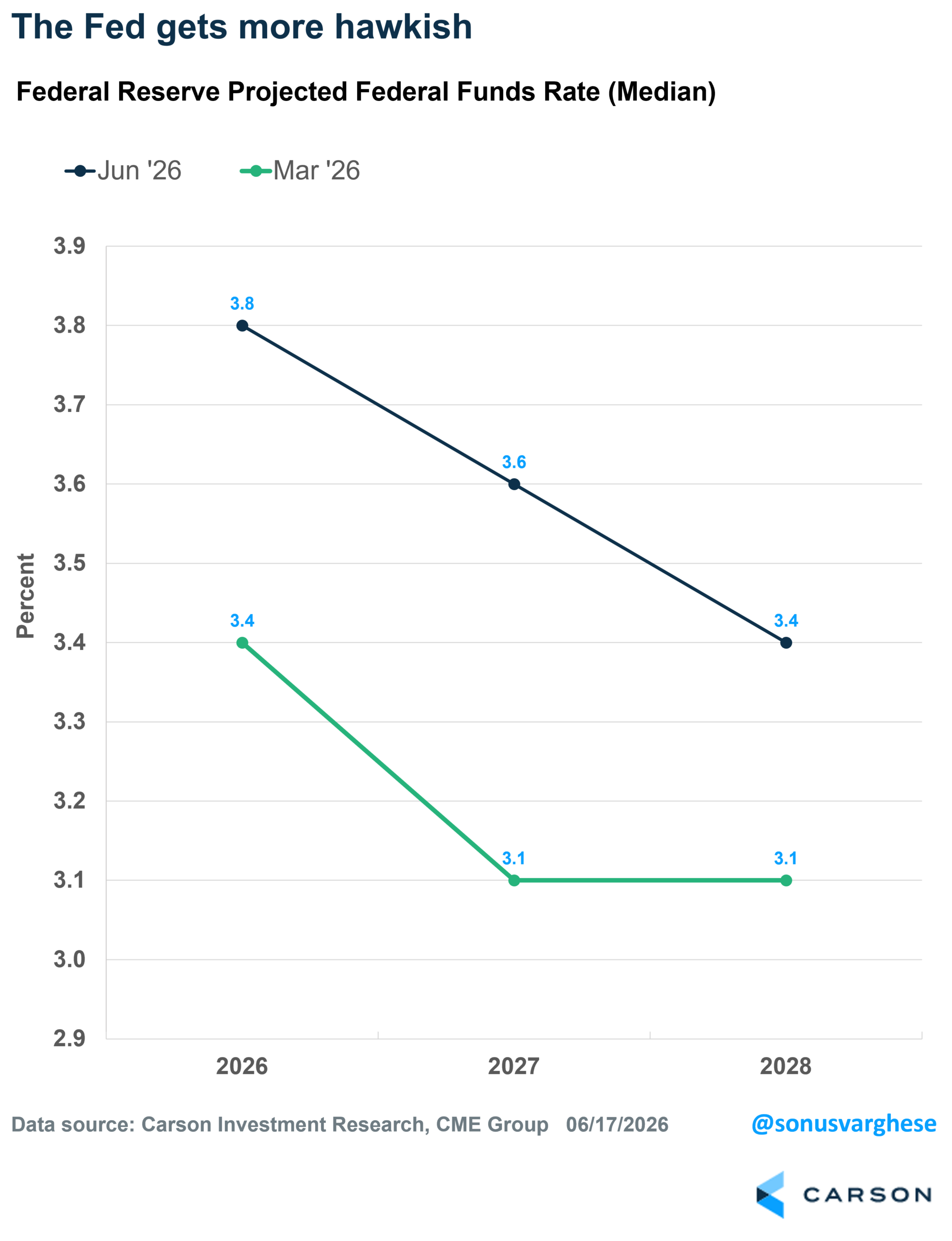

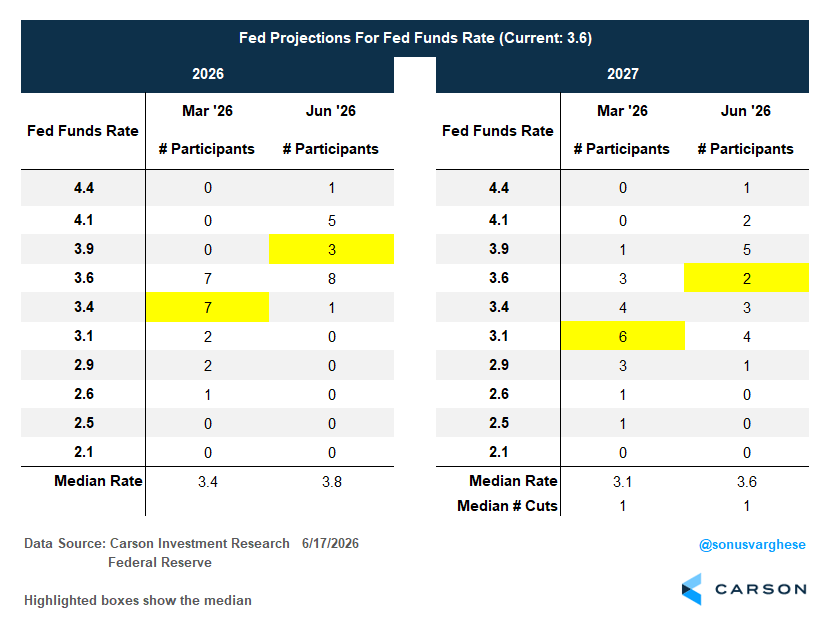

The June meeting was also important because it’s one of the four meetings in which the Fed puts out their Summary of Economic Projections (including the “dot plot” of policy rate expectations). The last one was in March, and all eyes were on what the dot plot would show.

The bad news is that the dots took a much more hawkish turn relative to March. At the same time, Warsh did not submit a dot for himself, which meant we have only 18 dots.

- The median expected policy rate for 2026 was increased from 3.4% to 3.9%, i.e. a move from one cut to one hike.

- The median expected policy rate for 2027 was increased from 3.1% to 3.6%, which still reflects one cut relative to the 2026 expectation.

However, the committee is very divided.

- 9 members (out of 18) expect to hike rates in 2026, with 5 expecting two rate hikes and 1 expecting three.

- 8 members expect to leave rates unchanged this year, and only 1 expects to cut.

- Back in March, a clear majority of 12 (of 19) expected to cut rates at least once in 2026.

- Even for 2027, 8 of 18 members expect to keep rates unchanged (or higher), while 10 expect to cut next year.

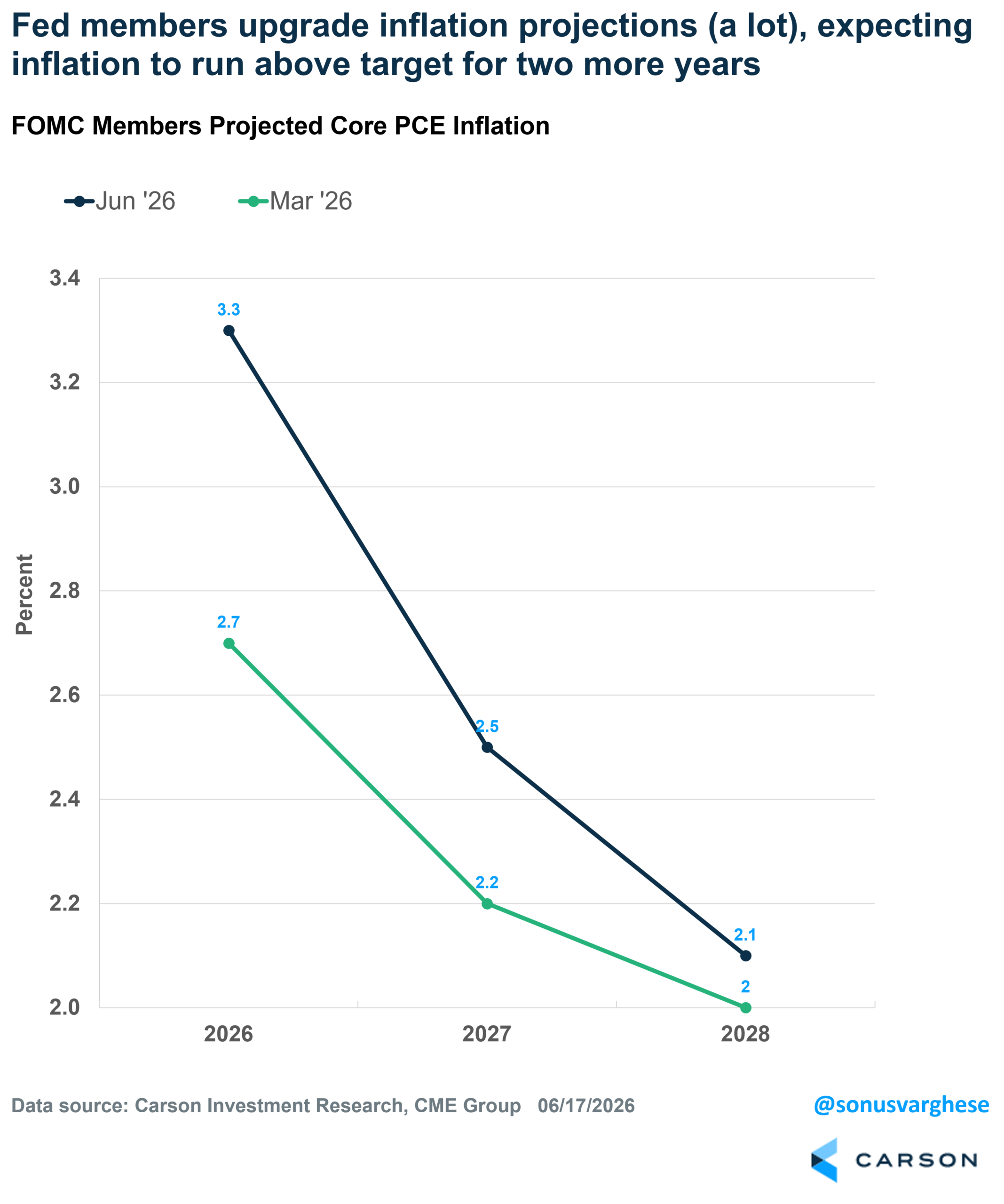

This shouldn’t be a huge surprise given the inflation backdrop, which was reflected in the inflation projections:

- Core PCE for 2026 was revised up from 2.7% to 3.3%

- Core PCE for 2027 was revised up from 2.2% to 2.5%

Two things jump out:

- The Fed expects inflation to run above target for another couple of years, at least.

- The fact that they revised core PCE higher tells you that even Fed members don’t think higher inflation is just about energy prices.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

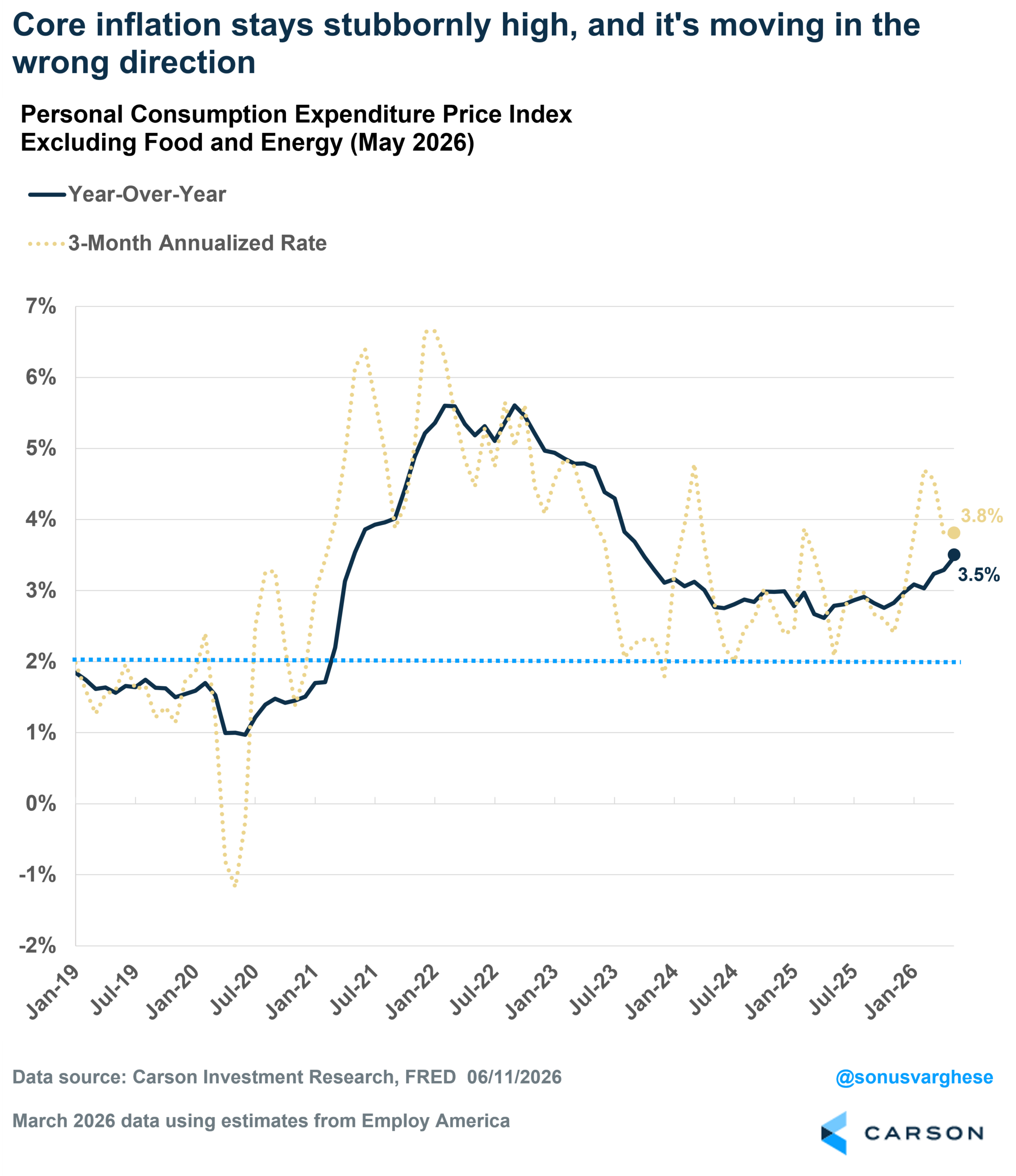

Note that core PCE is expected to hit 3.5% year over year in May and run at an annualized pace of 3.8% over the last three months. There’s a good chance that core PCE will be higher than 3.3% by year end.

Policy Is Actually Dovish, While the Economy Runs Hot

It sounds odd to call policy dovish after a hawkish pivot in the dot plot. But policy has to be judged against the Fed’s own growth and inflation projections (which we have for the moment).

One way to measure how easy or tight policy is: expected “real” policy rates, i.e. expected policy rate minus expected inflation. The Fed’s long run policy-rate expectation is 3.1% while inflation is expected to settle at 2%, implying a “neutral” real rate of 1.1%. Against that baseline, the Fed’s thinking (excluding Warsh) actually became easier from March to June:

- In March, the median rate projection for 2026 was 3.4% while core PCE was projected at 2.7%, i.e. a real rate of 0.7%.

- In June, the median rate projection rose to 3.8%, but the core PCE projection rose even more, to 3.3%, implying a real rate of just 0.5%.

In other words, policy was already expected to be on the easy side in March. By June, it had become even easier. The current policy rate is 3.6%, while core PCE is running at 3.5% year over year, implying a real rate of just 0.1%. Using headline PCE at 4.1%, the real rate would be negative. Either way, policy is well below the Fed’s estimated neutral real rate of 1.1%.

And remember, the 3.8% median rate projection for 2026 is just that, the median of 18 officials. Only half expect hikes this year, which means there is still meaningful uncertainty around whether any hikes happen at all. A Fed that holds rates steady while inflation remains elevated is not running restrictive policy.

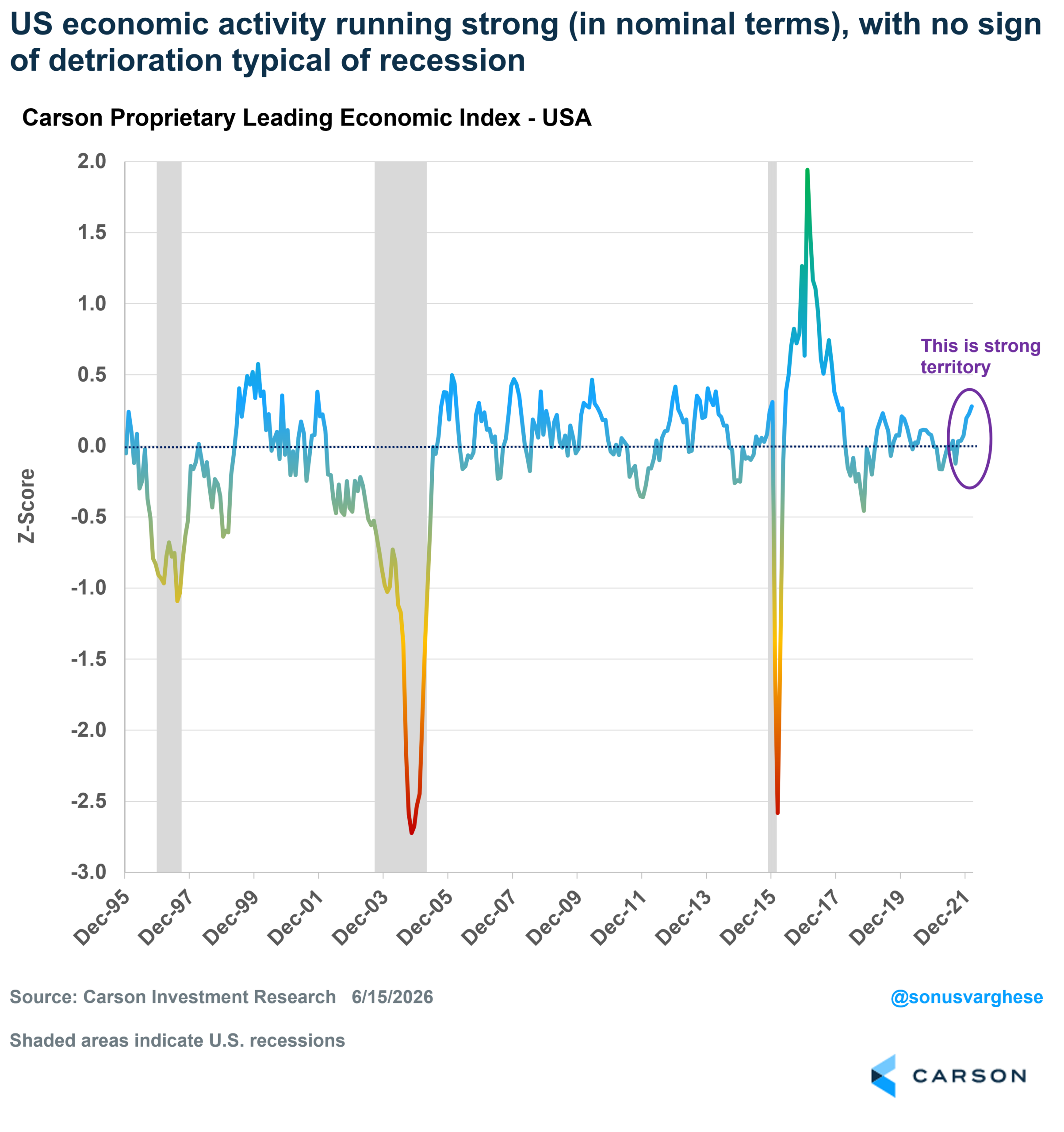

That would be more defensible if labor market risks were rising, but they are not. As I wrote a couple of weeks ago, the labor market has clearly stabilized, and if anything, things may be improving. Core retail sales (excluding things like gasoline and autos) are up 8.7% annualized over the last three months. Our own Leading Economic Index, which captures a diversified group of economic indicators, points to robust activity. Yes, these are nominal measures, but it gets to the point that inflation is hot.

More Uncertainty in Markets

The immediate reaction from markets to Warsh’s commentary (or lack thereof) was not positive. The S&P 500 fell 1.2% on the day, though this may easily be reversed once the focus shifts back to AI. But the action in the bond market was more telling. Treasury yields climbed, especially for shorter tenors. The 2-year yield rose to 4.15% (from 4.05), the highest we’ve seen this year. The 10-year yield saw relatively less movement but is still at 4.43%, well above levels we saw before the war (close to 3.95%).

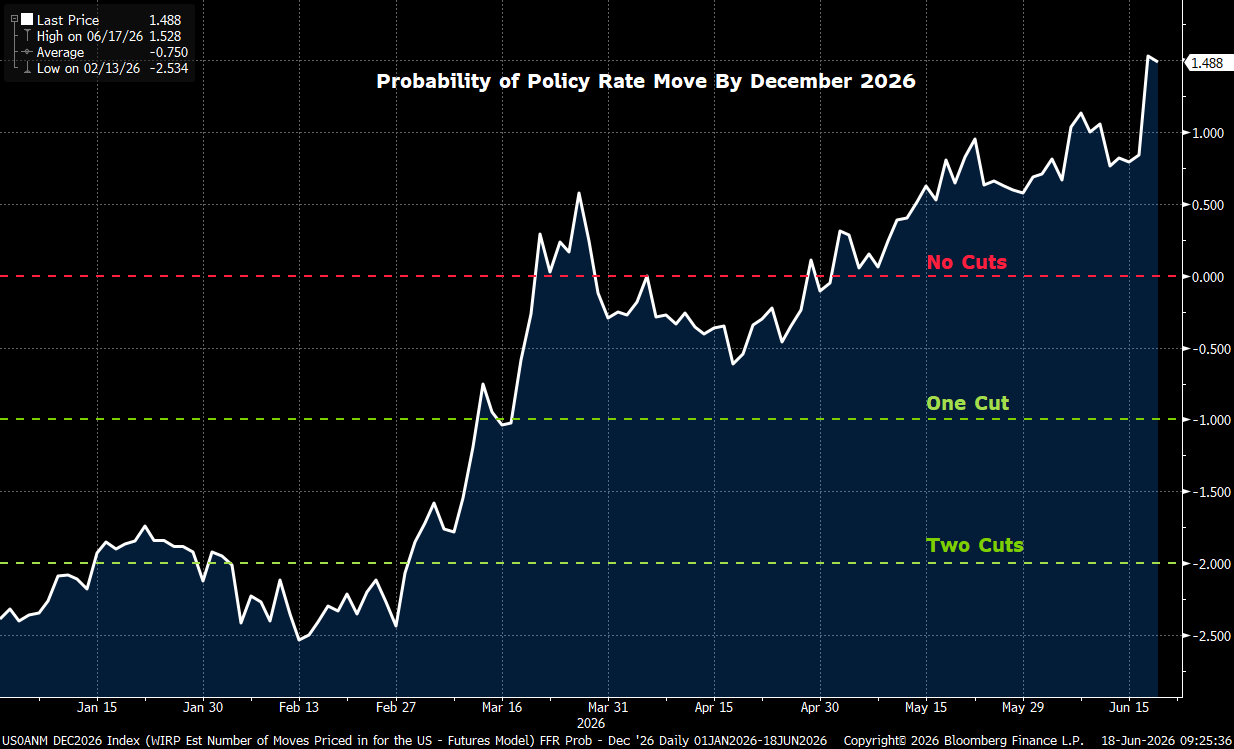

Higher yields get to the fact that inflation is running hot, and the jump in shorter-term yields tells you that markets expect the Fed to raise rates this year. But there is enormous uncertainty around this as well:

- The probability of a rate hike in July jumped from 10% to 32%.

- The probability of a rate hike by October surged from 42% to 100%, i.e. a rate hike is fully priced in.

- The probability of a rate by December jumped from 84% to 150%, implying one hike is fully priced in and there’s 50% probability of a second.

The cost of the war is clear in bond yields, and policy rate pricing. On the eve of the war, markets were pricing in two rate cuts by year end. The outlook is much less clear now. Add in new uncertainty around the Fed’s reaction function and it isn’t surprising that the probability of a July rate hike (just six weeks away) is closer to a coin flip than zero.

I wouldn’t be surprised to see rate hike probabilities move toward 50% before each meeting if three things persist: 1) inflation remains elevated, 2) the Fed Chair stays disengaged from communication, and 3) the rest of the committee remains split between those looking for hikes and those willing to wait out inflation (once again).

For now, our base case is that the Fed refrains from hiking (or cutting) this year, with a slim majority choosing to tolerate elevated inflation rather than tighten further. But the confidence band around that view has widened a lot. Policy uncertainty is higher, and markets will have to price that in.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8984813.1. – 18JUNE26A