Many people, when they start paying attention to investing, run into the same problem: the vocabulary is enormous, and nobody explains how the pieces fit together. Stocks, bonds, ETFs, mutual funds, CDs, money markets, private equity, venture capital… it sounds like a different language, and the financial world tends to assume you already know it. Or as people I know would say, the financial world makes everything way more complicated than it needs to be, and maybe they are on to something.

Think of this as a map, not necessarily a recommendation. It will tell you a good chunk (but certainly not everything) of what exists, what each thing is fundamentally doing for you, what it has historically delivered, and what you give up to get it. The real question is not just what each investment means; it’s more specifically what role it plays in a portfolio.

The Fundamentals

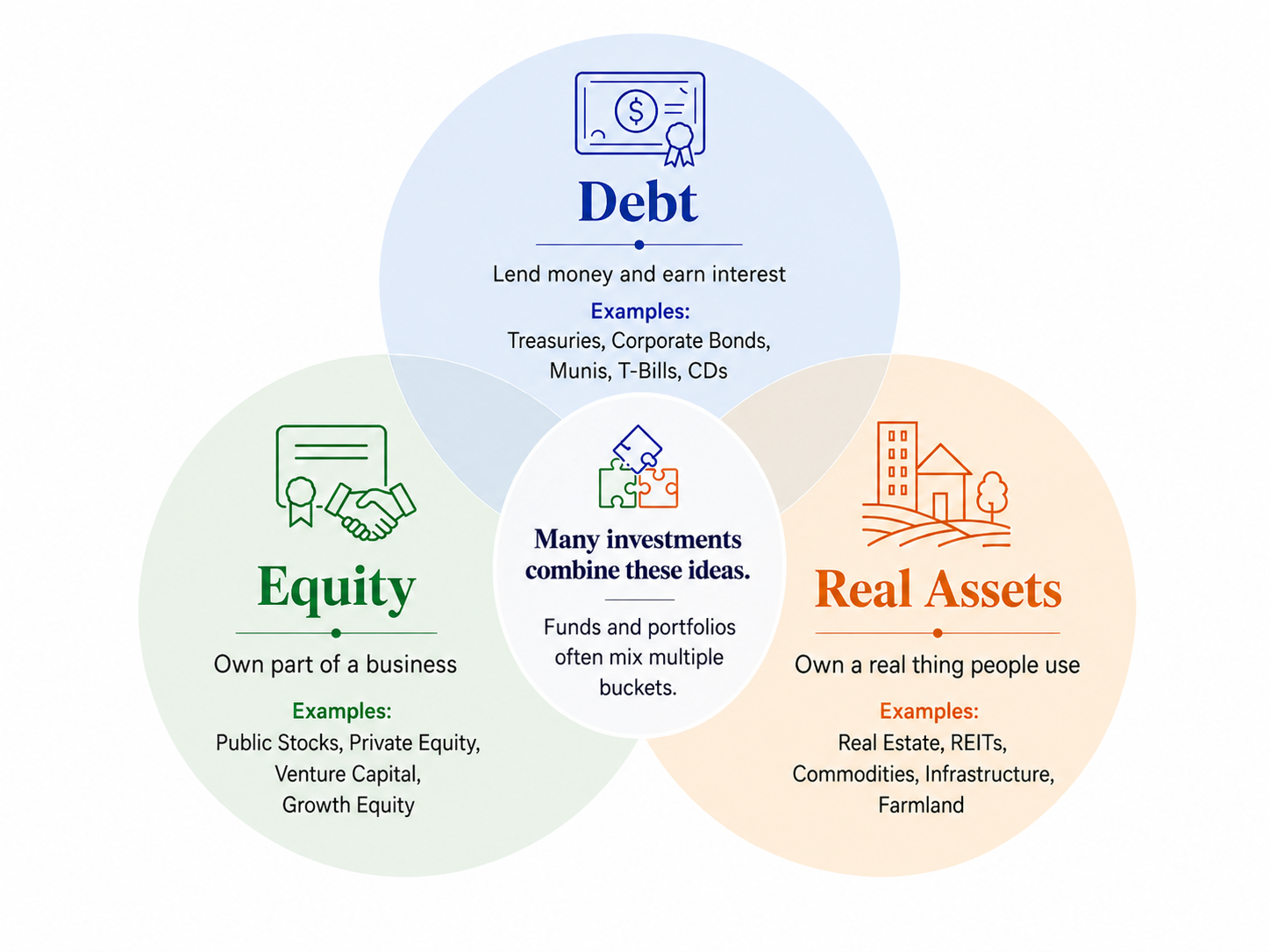

Strip away the labels, and many investments are doing one of three things:

- Lending money to someone (a government, a company, a bank) and getting paid interest for the privilege. This is debt.

- Owning a piece of a business and sharing in whatever it earns, loses, or eventually sells for. This is equity.

- Owning a real thing: Real estate, commodities, or infrastructure, which has value because people want to use it.

Most of everything else is a wrapper, a structure, or a combination. A mutual fund is a wrapper. A 60/40 portfolio is a combination. A private equity fund is just equity ownership in private companies with a different liquidity profile and fee structure.

Once you have those three buckets in your head, the rest of this becomes much easier.

Source: Carson Investment Research, OpenAI 6/4/26

Public vs. Private

Every investment also lives somewhere on a spectrum from highly liquid and publicly traded to fully private and locked up.

Public means it trades on an exchange, you can buy or sell on a Tuesday afternoon, and the price is set by millions of participants every second. Private markets are the opposite. You’re typically locked in for years, the price is whatever the manager says it is until a transaction occurs, and access is often limited to accredited investors. Accredited investors are investors who meet SEC wealth or income thresholds, granting access to private investments unavailable to the general public.

Public isn’t better or worse than private. They have different uses. But for most people, the public side is where the vast majority of an actual portfolio lives, and that’s where we’ll spend most of our time today.

The Public Side

Cash and cash equivalents (T-Bills, money markets, CDs)

You’re lending money for a very short period to either the U.S. government or a bank, and getting paid a modest rate of interest. Risk is minimal for this kind of investment. For T-Bills, essentially zero default risk (i.e., backed by the full faith of the U.S. Government); for CDs, FDIC insurance up to certain limits; for money market funds, risk is very low but not quite zero.

What you get: Whatever short-term rates are paying. As of June 2026, with the federal funds rate target range at 3.50%–3.75%, many short-term cash-like instruments are yielding in the mid-3% range, though actual yields vary by product.

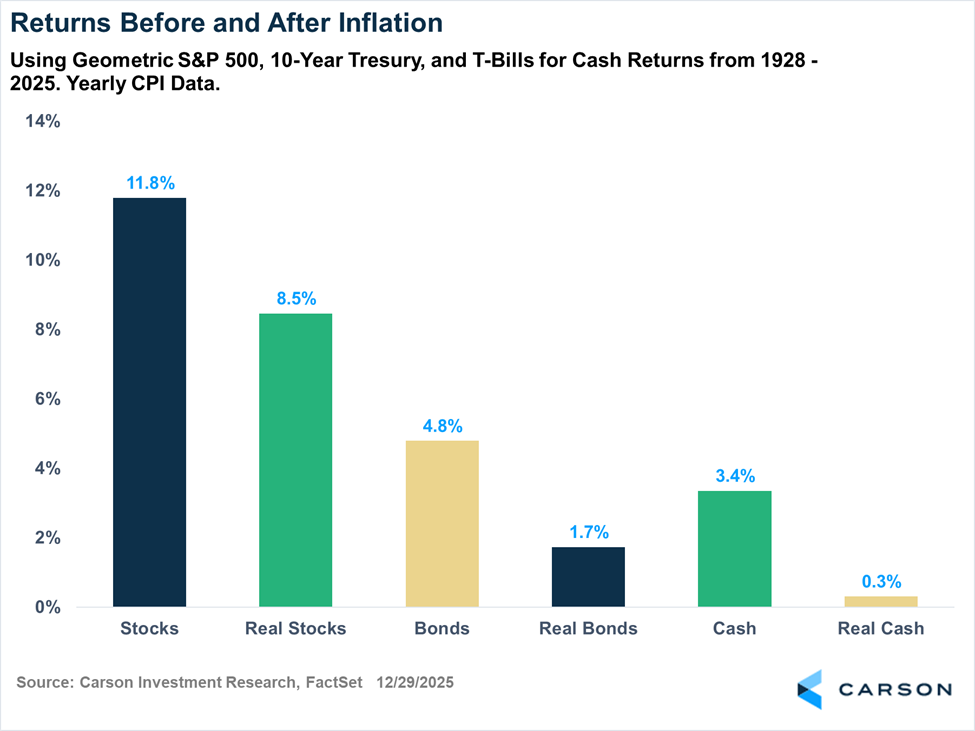

When you’d want this: Money you may need in the next year or two. For example, an emergency fund, or potential dry powder you’re waiting to deploy into a new stock/sector. In our view, cash is not a long-term wealth-building tool. Over the decades, cash has barely kept up with inflation, as shown in the chart below.

Bonds

A bond is a loan with a schedule of payments. You give a company or government a sum of money, and in return they pay you a fixed rate of interest for some number of years (with the exception of zero-coupon bonds). After that designated period of time is complete, you get your initial principal amount back. These two components of a bond drive what a bond does in your portfolio.

Duration: Roughly, how long until you get your money back. A longer duration means greater sensitivity to interest rate changes. A 30-year Treasury and a 2-year Treasury are both “Treasuries,” but they behave very differently. When rates rise, the price of long bonds get hammered, while the price of short bonds barely move. The trade-off here is that longer-duration bonds generally have a higher yield to maturity (i.e., holding through the entire life of the bond).

Credit risk: How likely the borrower is to pay you back. The U.S. Treasury is at one end of this spectrum (effectively low default risk). Investment-grade corporates (Baa and above) are next. Below that, you get into high-yield, also called junk bonds, where default rates are meaningfully higher, and yields compensate you for that because of the higher risk, or in other words, higher default rates.

When you’d want bonds: Income in a portfolio (high-quality bonds tend to rally when stocks fall, though 2022 reminded us that’s not always true, and you can read more about that dynamic here), and capital preservation as you get closer to needing the money.

Stocks

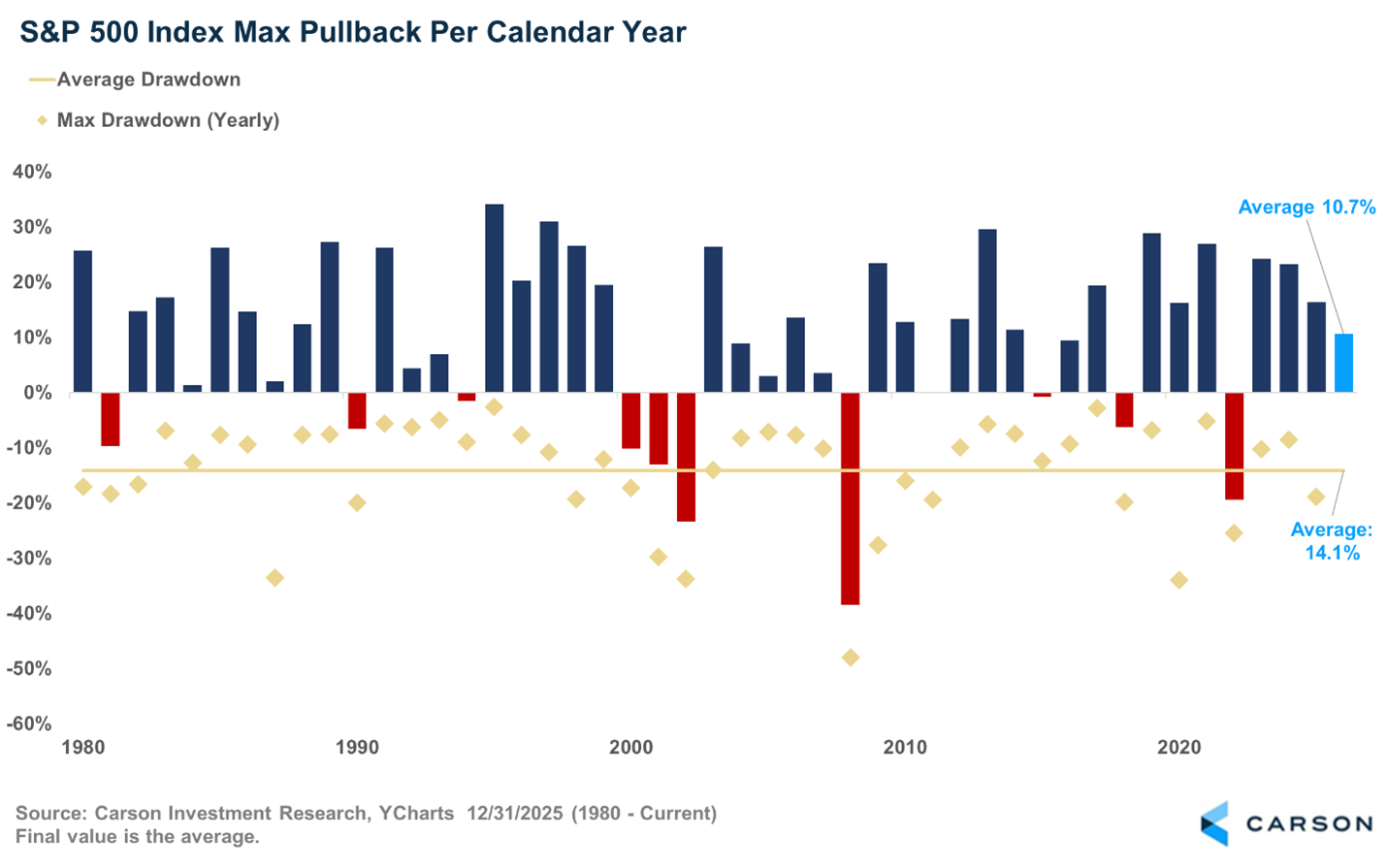

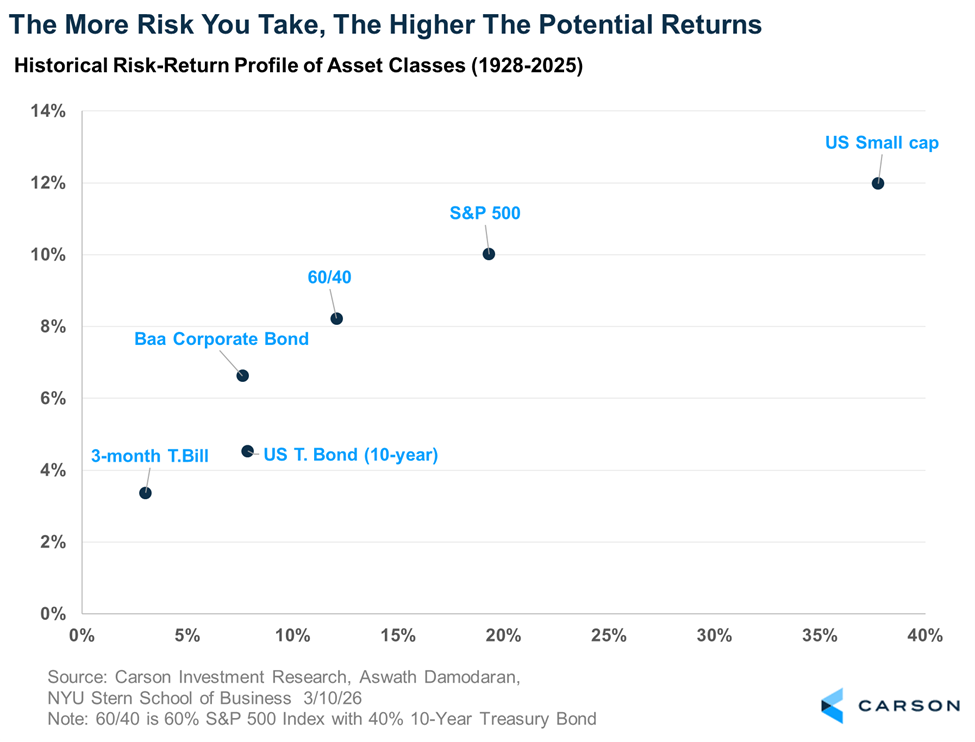

Ownership in a public company. You make money in two ways: the share price goes up, or the company pays you a dividend. Over long periods, public equities (stocks) have been among the highest-returning major liquid asset classes. Historically, they return roughly 10% on average using the S&P 500 as a proxy, but they get there through regular, sometimes brutal drawdowns.

A Few Classifications of Stocks:

- Large cap vs. small cap: Large and small cap stocks are derived from how big a company is based on its market cap (market price x shares outstanding). Large-cap stocks are mainly a part of the S&P 500, whereas smaller companies have historically delivered higher returns with much higher volatility.

- Domestic vs. International: The U.S. has dominated the last 15 years; however, that wasn’t always true and may not stay true (like last year!).

- Growth vs. Value: Growth stocks are a type of stock with high growth rates of revenue. They usually come with more volatile earnings, and trade at higher multiples. Value stocks are companies with lower growth, but more stable cash flows. For this reason, they trade at lower multiples.

When you’d want stocks: Long-term wealth building. Anything you don’t need for at least 5–10 years, and the stomach to ride out potential 30%+ drawdowns without selling. Stocks are historically the engine behind growing a portfolio, however, they only may work if the investor can survive the volatility when times get tough.

ETFs and Mutual Funds (the wrappers)

These aren’t a separate asset class; they are simply containers. The best way to explain an ETF is it is a container that trades like a stock that holds a group of selected securities. For example, SPY (a common ETF), is designed to track the S&P 500 which is the market-cap weighted version of the S&P 500. The wrapper determines fees, tax efficiency, how easily you can trade it, and the minimums that apply.

ETFs are usually cheaper, more tax-efficient, and trade like stocks. Mutual funds price once a day and have historically been higher fee, though that gap has narrowed. There are 2 types of mutual funds: closed and open end. Most traditional mutual funds are open-end funds: investors buy or redeem shares at the fund’s net asset value, typically once per day after the market closes. Closed-end funds are different: they issue a fixed number of shares and then trade on an exchange, meaning they can trade at premiums or discounts to NAV.

Smaller Other Examples

- TIPS: Treasuries indexed to inflation. They are boring until inflation shows up, then suddenly very interesting, especially where things are today. While TIPS can help protect purchasing power when inflation arises, their prices can still fall when real interest rates rise.

- Municipal Bonds: Bonds issued by state and local governments. Interest is often tax-free at the federal level, which makes it attractive to potential high earners.

- REITs: Companies that own real estate, traded on exchanges. This is the most accessible way to get real estate exposure without becoming a landlord.\

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The Private Side

This is where much of the financial press attention has gone lately, especially on IPOs/private credit, but for most investors it’s either inaccessible (often limited to accredited or qualified investors), illiquid in ways they don’t fully appreciate, or both.

So why bother? Because of access and correlation. A growing share of economic value is being created at companies that stay private for longer than they used to, and that exposure isn’t replicated in public markets. Private returns also behave differently across cycles, partly because the underlying businesses, capital structures, and exit timelines differ from public equivalents. Done well, a private market allocation can also tap into return streams — illiquidity premiums, operational improvements, and manager skill in inefficient markets — that are hard to replicate publicly.

Private Equity

“Private equity” technically covers everything from a $50K seed check into a two-person startup to a $10B buyout of a public company. They’re very different businesses with very different return profiles.

- Venture capital: Equity investments in early-stage companies. Seed, Series A, B, C, and so on, as the company matures. Returns are power-law distributed which means a small number of huge winners pay for everything else. This is high risk, high reward with a high number of investments going to 0.

- Growth equity: Investments in more mature private companies that are scaling but not yet ready (or willing) to go public.

- Buyouts (traditional PE): Taking established companies private, usually with significant leverage, improving operations or financial structure, and selling for a profit several years later.

Private Credit

One of the fastest-growing corner of private markets. Instead of equity, you’re lending money to private companies. Often ones that are too small or too leveraged to issue public bonds. This includes direct lending, mezzanine debt (a hybrid that sits between senior debt and equity), and distressed debt.

Yields may be higher than public credit. So is illiquidity, and so is the risk that you can’t actually mark these loans honestly until something goes wrong. The trade-off between public markets and private markets is that private investments can look smoother on paper precisely because they do not trade every day which is called mark to model while public investments are called mark to market, meaning you can see quoted prices on a brokerage.

Real Assets (private)

Direct real estate, infrastructure, farmland, timberland. Long-holding, income-producing assets are often used as inflation hedges and portfolio diversifiers.

Source: Carson Investment Research, OpenAI 6/4/26

So, when do you want what?

There’s no clean answer because it depends on three things: your time horizon, your tolerance for volatility, and what you’re trying to accomplish.

But the general framework looks like this:

- Money you need in the next 1–2 years: Cash, T-Bills, CDs.

- Money you need in the next 3–7 years: Mostly bonds, some stocks.

- Money you don’t need for a decade or more: Mostly stocks, some bonds, with private market exposure if you have the access and tolerance.

- Income generation: Bonds, dividend stocks, REITs, and some private credit.

- Inflation protection: TIPS, real assets, equities over long periods.

A 25-year-old saving for retirement and a 70-year-old funding it should own different mixes of the exact same set of building blocks.

The Point

You don’t need to know everything in this post. You need to know that when someone uses a term you don’t recognize, it almost certainly fits into one of three buckets: debt, equity, or real assets, and lives somewhere on the public-to-private spectrum. From there, the questions become: what’s the time horizon, what’s the risk, what’s the cost, how is it taxed, and what’s it doing in the portfolio to help me accomplish my goals. It is worth noting that we didn’t cover everything today; we merely scratched the surface. However, this general framework may do much of the heavy lifting for you.

By Harry McDonald, Analyst, Investment Research

8961931.1. – 4JUNE26A