“Are we in a bubble?” The question echoed over the sounds of Memorial Day weekend. As markets continue to make new highs – in some ways in extraordinary fashion – many investors are likely asking this same question. How long do you ride a wave until it crashes ashore?

The short answer is there is no telling, especially in the face of new and transformative technology. As we have discussed regularly, one way to root yourself in some semblance of reality is to look at the actual numbers and data, and in this case, boring old valuations. All the adages apply here – time in the market is more important than timing the market, and so on – and given that is true, then markets become a relative game. Looking at stocks on a relative basis means one area of overvaluation is another area’s undervaluation – and a potentially attractive rotation opportunity.

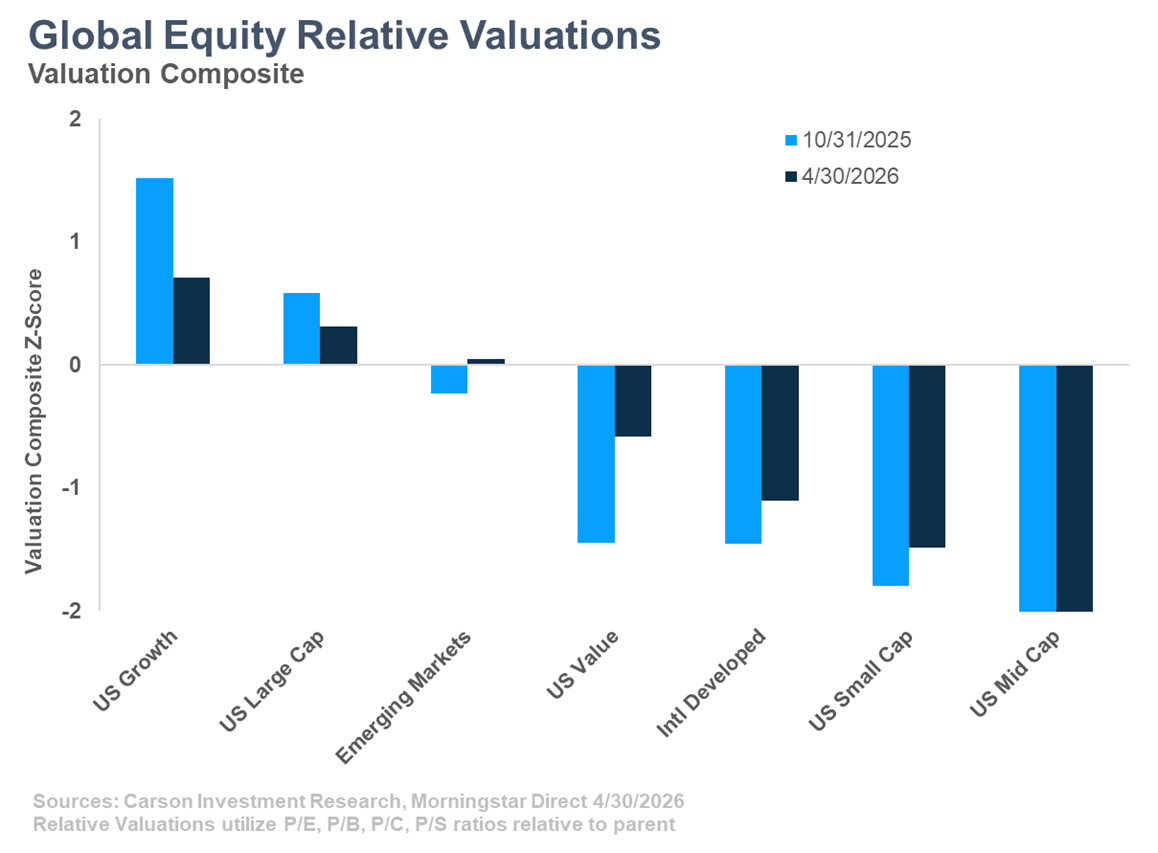

Since our 2026 Outlook was published, relative valuations have seen important changes. Large-cap US growth stocks have actually gotten cheaper – relative to other areas of the market. In particular, strength in value, international, emerging markets, and small-cap stocks has adjusted the valuation picture to be a bit less lopsided. As always, there are a variety of reasons for the outperformance of these areas. One would expect that as the AI “trade” continues to develop, it will spread to other areas of the market over time.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Valuation ‘Chaos’

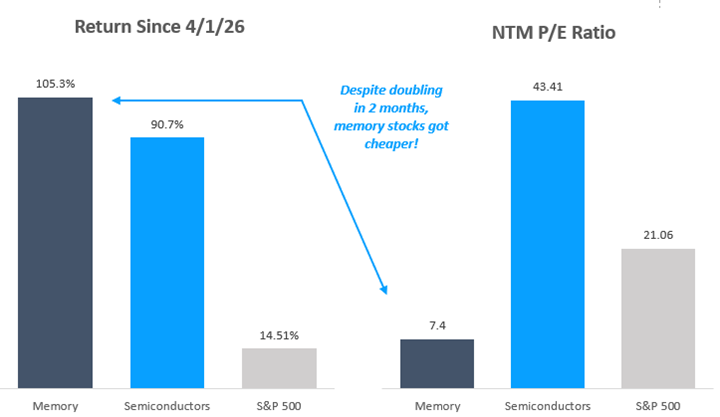

This AI trade and the expected impact surrounding its growth continue to create huge winners and losers, and even several winners that have become losers and vice versa. One microcosm of this phenomenon has occurred in just the last two months. Surging AI server demand, which relies on specialized memory at a time when that memory is scarce, has created a large supply/demand imbalance that has propelled a subset of stocks substantially higher. On top of this, future demand expectations and pricing power are so high that earnings expectations have increased even more than prices, in many cases causing the P/E ratios of the stocks in that space to fall. Compare traditional semiconductors, which have had a great run of their own. Traditional semis trade at 43x the next 12-month’s earnings, versus just 7x for memory stocks (which are typically classified as semiconductors)! “Chaos” may be a strong word here – more precisely, the market is readjusting rapidly to future earnings expectations.

Source: Carson Investment Research, Morningstar Direct 5/27/2026

This memory surge encapsulates how difficult it is to call the current stock market a bubble. Are there areas that might be overheated? Absolutely – but that is where relative valuations and a systematic process come into play. There are plenty of other beneficiaries of AI – but also other global forces – that can provide value for diversified investors. Earnings will ultimately decide whether areas of the market are in a bubble or not. Strong, continued earnings-growth momentum and a pickup in M&A and IPO activity are a couple of factors that keep us riding the wave.

For more content by Grant Engelbart, VP, Investment Strategy and Research, click here.

8949928.1. – 29MAY26A