Life is transitory, and so are inflation shocks (caveat: on a long enough timeline).

The Federal Reserve (Fed) held rates steady in the 3.50-3.75 range at its March meeting, as expected. But all eyes were on the Fed’s updated Summary of Economic Projections (the “dot plot”), where each of 19 members jot down their estimates for GDP growth, unemployment rate, and inflation under “appropriate “ monetary policy. Since there are 19 members, there’s always a variety of opinions (or dots), but generally the median dot tells you something useful about the Fed’s reaction function, i.e., what they would possibly do if the economy followed a certain path, and therefore, how they’d likely act if it didn’t.

This time, the dots were a complete mess, and the story was completely incoherent. Which is why Fed Chair Jerome Powell told everyone:

“If there was ever going to be a time to skip producing an SEP, this would be it”

He said that people put something down because they had to. What’s striking is that members just completely ignored what’s happening in the Middle East, and there was hardly a hint of that in the projections. Powell underlined that the whole situation is beyond their control, and that it’s too soon to know the scope and duration of its impact on the US economy.

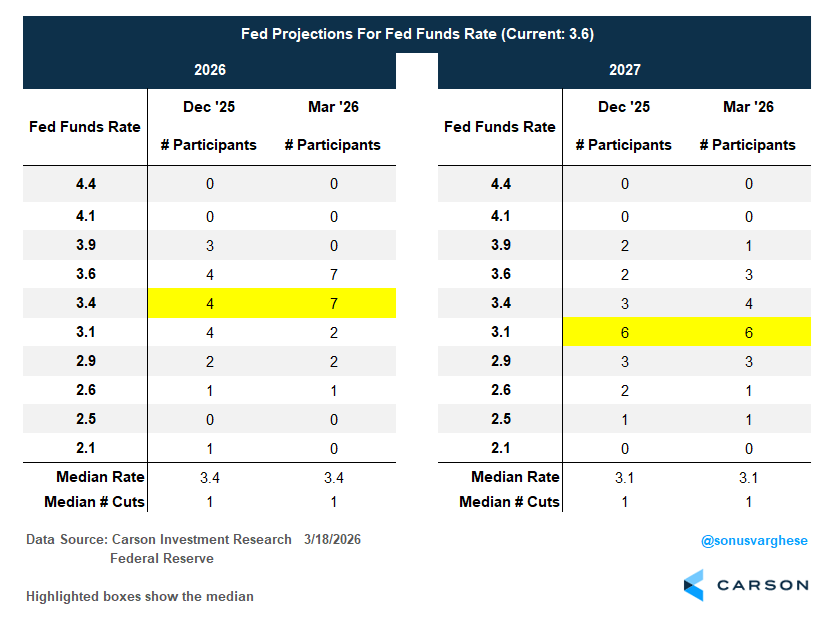

The median dot was basically unchanged:

- A projected policy rate of 3.4% in 2026 (the current rate is 3.6% and so that implies 1 cut this year)

- A policy rate of 3.1% in 2027, implying one more cut next year

Not a single member projected a rate increase in 2026, and just 1 projected a rate hike next year.

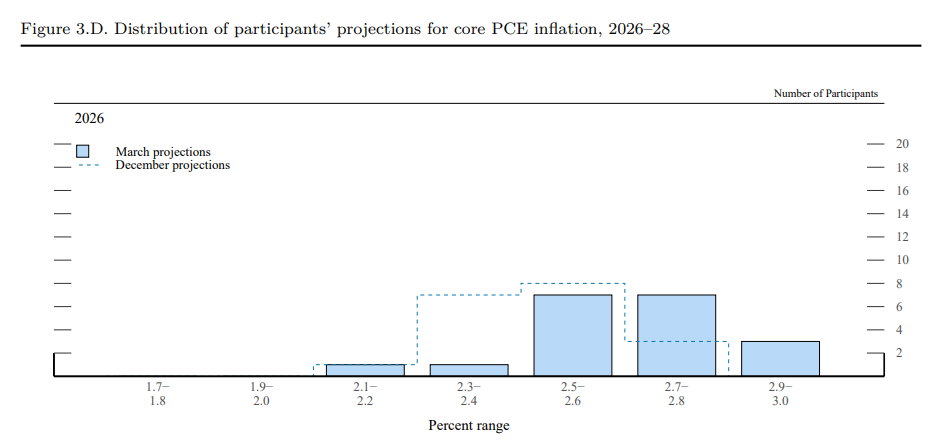

At the same time, they increased their projections for GDP growth (from 2.3% to 2.4% for 2026 and 2.0% to 2.3% for 2027) and for core inflation (from 2.5% to 2.7% for 2026 and 2.1% to 2.2% for 2027). This is presumably driven by optimism about AI-based productivity, as well as increased capex, which is putting some upward pressure on inflation.

Yet, there’s a lot of uncertainty here. If you look at the distribution of members’ projections of core inflation, you see a wide distribution. Members’ estimates ranged from 2.1% to 3.0%. Though only 3 members projected core PCE to be 2.9-3% at the end of 2026. The other 16 members think it’ll be lower.

Source: Summary of Economic Projections, March 18, 2026, FED

This beggars belief for two reasons

- One: Core inflation (defined by the Fed’s preferred metric, the personal consumption expenditures metric) was already at 3.1% pre-crisis, and that’s not just driven by tariff-impacted goods but core services ex-housing as well.

- Two: The outlook looks quite bad, given Middle East events, which will put upward pressure even beyond just gasoline prices, thanks to higher fertilizer prices, jet fuel prices, and shipping costs.

Setting aside the Middle East events for a moment, the Fed is essentially looking through tariff-impacted inflation and believes inflation will fall once tariffs pass through. In theory, tariffs should result in a one-time price increase, but in the real economy, tariff pass-through can take quite a long time. Still, Powell and co believe the tariff impact will pass, and that’ll send inflation closer to their target.

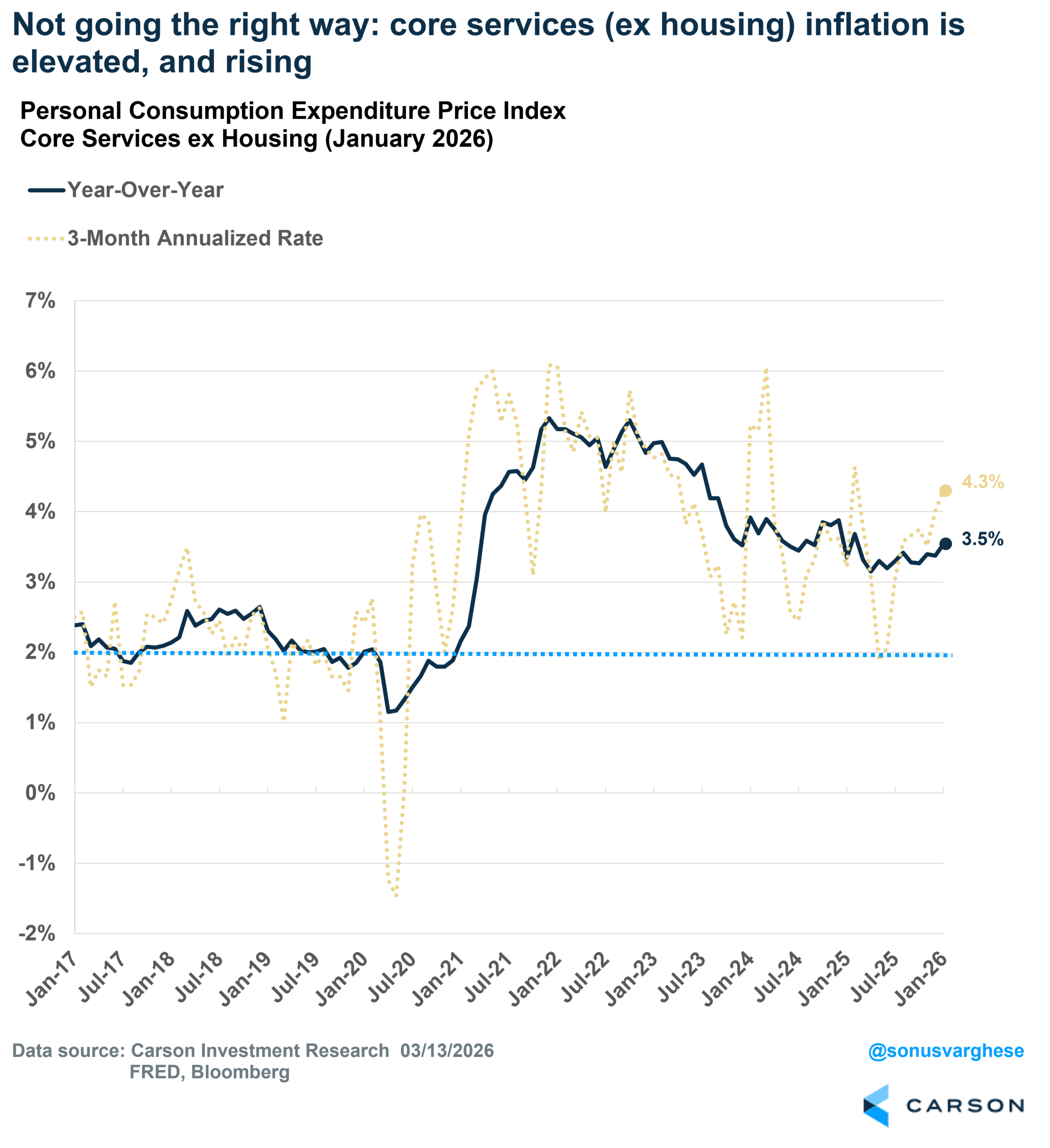

The Fed doesn’t think core services’ ex-housing inflation is a problem, despite inflation for this category running at an annualized pace of 4.3% over the past 3 months and 3.5% year-over-year – well above the pre-pandemic pace of around 2%.

When asked about elevated core services inflation, Powell responded that a softer labor market ought to drive it lower, but obviously that’s not happening, and he’s uncertain about the cause.

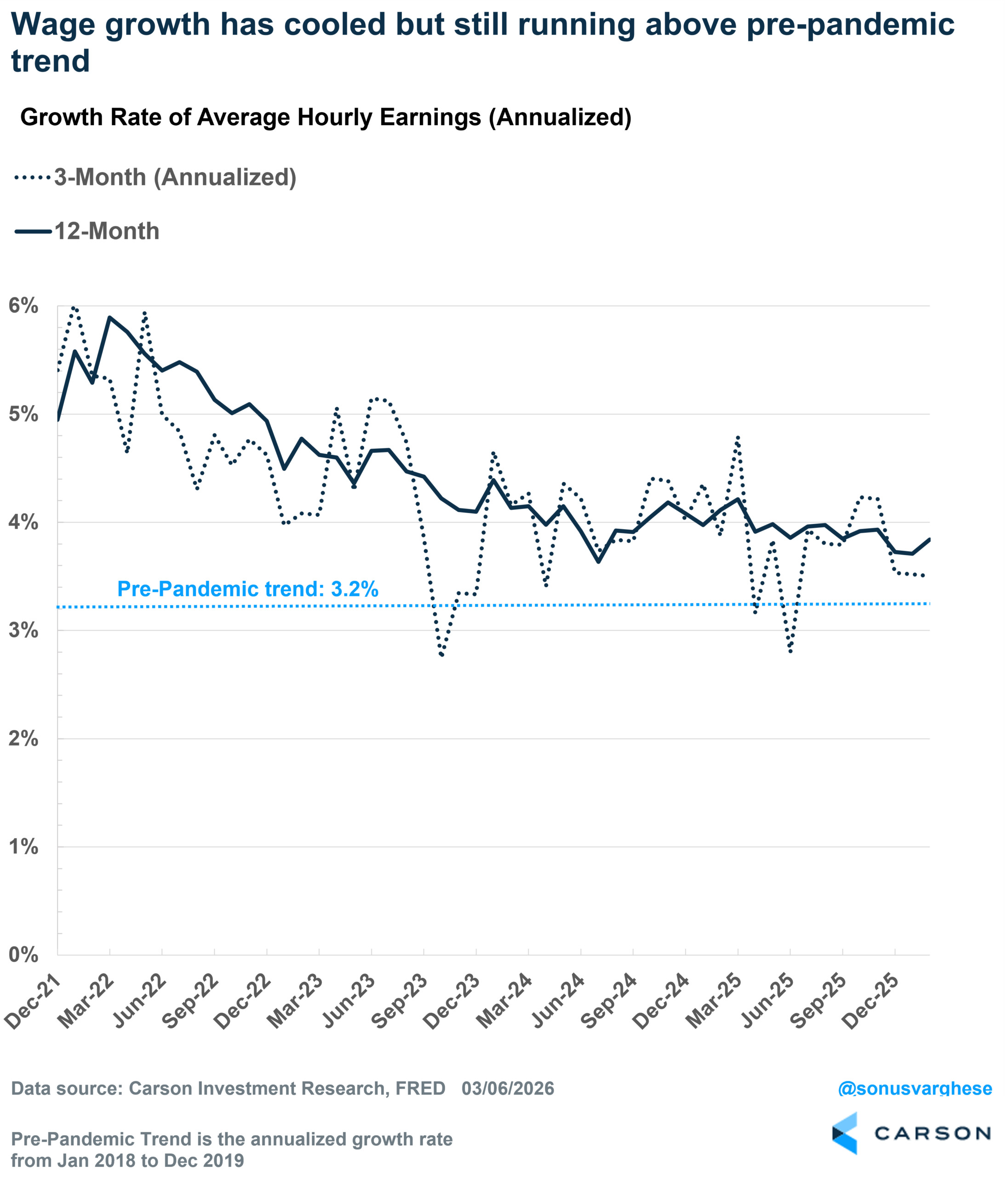

In reality, it’s likely the labor market isn’t as soft as weak headline payroll growth suggests. The unemployment rate is low relative to history, and the prime-age employment rate is higher than at any time during the last two expansions. Ultimately, wage growth is still running quite strongly, and that’s probably why services inflation is hot.

All this would also imply that the policy is not too tight.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Hope Is The Strategy

If there was one message in the projections, it’s that the Fed may treat the energy shock as transitory. Or perhaps they’re hoping it’ll be transitory. In this case, hope certainly seems to be the strategy.

For now, they’re focusing on what they know and what they think they know is that the tariff shock is also transitory.

Now, it probably makes sense to look through a supply shock, or two. The problem is that we’ve had 5 shocks in 5 years.

- The post-covid inflation surge as supply chains got snarled

- The Russia-Ukraine war, which sent energy and food prices much higher

- The tariff shock on goods inflation

- The immigration shock, likely putting some pressure on wage growth

- The latest Middle-East crisis

You can dismiss each of these as one-offs and transitory, but when they repeatedly occur (never mind the cause) and have the same upward impact on inflation, that means the Fed is not getting back to its 2% target any time soon. Over the last 5 years (2021-2025)

- The Consumer Price Index (CPI) has averaged a 4.5% annual inflation rate.

- The Fed’s preferred inflation metric, the Personal Consumption Expenditures Price Index (PCE), has averaged 4.0%.

At some point, 3% becomes the new 2%, but then it’s possible it starts creeping up to 4%. That’s a problem.

The Fed is clearly aware that it’s missed its target by a wide margin over the past 5 years, and despite the dots (which Powell told us to ignore anyway), it’s probably disinclined to cut anytime soon. Or put another way, we need inflation to head lower and the unemployment rate to head higher if the Fed is to cut again. Safe to say, the inflation rate is not heading much lower this year (if at all).

That means rate cuts are unlikely.

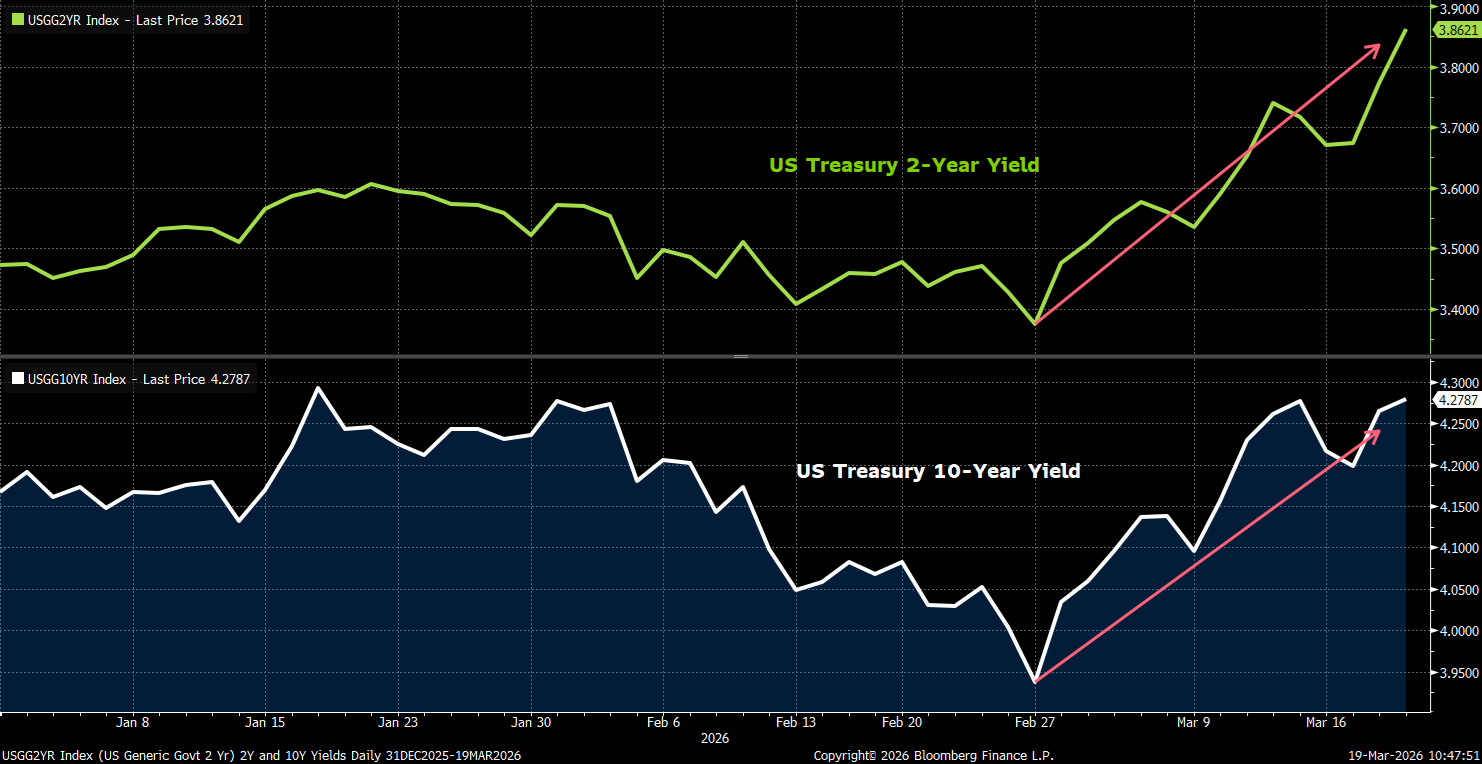

However, as I wrote in my previous blog, there’s a good chance that the Fed shifts its rhetoric to rate hikes as well. For now, everyone’s focused on higher gasoline prices, which could reverse if the crisis ends soon. But we are on Day 20 of this crisis, and the world is now short of 250-300 million barrels of oil from the Middle East, which would have been used in refineries to make all sorts of petroleum-based products needed around the globe. This is a recipe for higher inflation across the board, and at some point, the Fed may no longer be able to ignore its impact. Especially if the crisis lasts a few more weeks (let alone months). There’s a reason why bond yields are rising:

- 2-year yields, which are essentially an estimate of Fed policy rates over the next 2 years, have surged almost 0.5% points over the last 3 weeks (to 3.86%)

- 10-year yields have jumped 0.34% points to 4.28%

This is a double whammy: not only does it increase borrowing costs across the economy (like mortgage rates), but it also means bonds aren’t providing protection amid a crisis.

The Fed pivoted to a much more hawkish policy path in April 2022, which roiled markets. That was because they waited too long. The longer they wait this time around, the larger the eventual pivot they may have to make, and that’s going to create more volatility in markets. Just don’t be surprised when it happens.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8832401.1. – 19MAR26A