We are so proud to release our 2026 Midyear Outlook, “Still Riding the Wave.” We’ve been bullish for years, and we think the second half of this year should still see nice gains, thanks to the combination of accelerating artificial intelligence (AI) investment, strong corporate earnings, fiscal expansion, and a Federal Reserve expected to look past elevated inflation, which should continue to support equities.

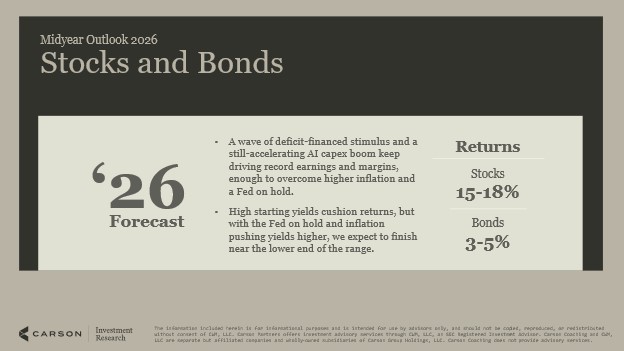

We are raising our full-year S&P 500 total return forecast to 15-18 percent, up from its prior 12-15 percent target, after the index delivered a 10.2 percent total return in the first half of the year. After a huge spike in oil, the war in Iran, and equity volatility in March, many other places cut their targets, but we never did. Even when the S&P 500 was down close to 5% for the year, we remained steadfast that the bulls would once again prevail in 2026.

Carson’s investment research team expects bonds to finish the year with returns of 3-5 percent, supported by higher starting yields but challenged by persistent inflation and a Federal Reserve that is likely to remain on hold.

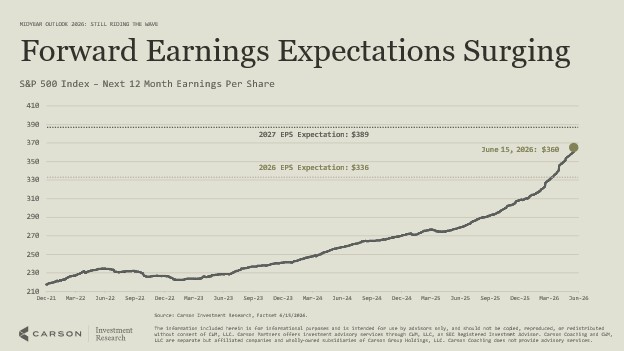

There have been many big stories this year so far, from the war in Iran to new leadership at the Federal Reserve Bank (Fed), to inflation worries, to oil surging, to a historic bounce in equities in the second quarter, to consumers feeling down and out, yet spending more and more. In the end, though, earnings drive long-term stock gains. At the start of the year, the S&P 500 was expected to see earnings growth of 14%, and that has now risen to 24%. Earnings drive long-term stock gains, and this is why stocks have done so well this year so far.

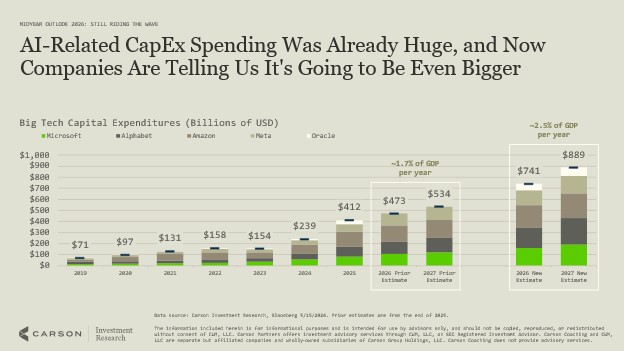

AI remains a big part of our economy, as the scale of the AI infrastructure buildout is a central driver of the current market environment. Over the last five quarters through the first quarter of 2026, real GDP growth averaged 1.9 percent annualized, with real investment spending on information technology equipment and software contributing roughly 0.9 percentage points per quarter. The outlook notes that 2026 capital expenditure estimates for major technology firms have increased to approximately $740 billion, or about 2.3 percent of GDP, more than four times the level seen in 2023.

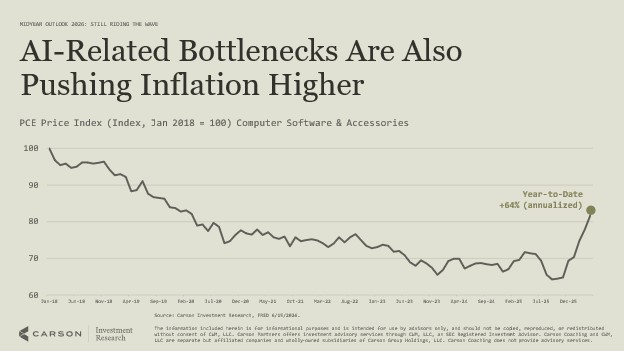

Inflation has remained stubbornly high and is a key risk for the rest of this year, but we came into the year expecting inflationary growth, so we’ve positioned our models accordingly. Still, the massive demand for AI has created historic moves, including AI-related bottlenecks, with the PCE price index for computer software and accessories rising at a 64 percent annualized pace through April 2026.

Where are we different than many others? There are two main places. The first is that we think the Federal Reserve Bank (Fed) will be on hold this year and won’t make any interest rate changes. Many expect them to potentially hike, maybe as soon as the next meeting in July, but we continue to think they will ‘run it hot’, which will help the economy and markets, while creating a difficult backdrop for bonds. Similarly, the team notes that higher borrowing costs will drag on certain areas of the economy, such as housing.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

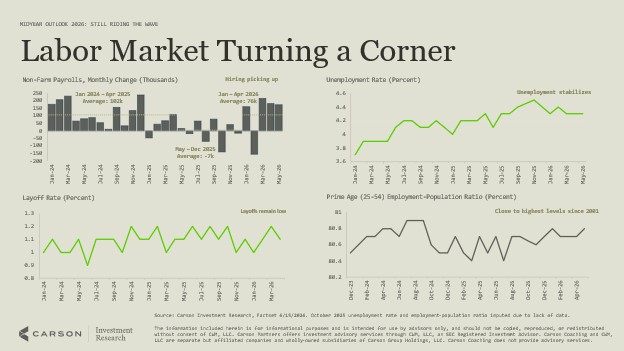

The second place we differ is that we said all year that the labor market was in better shape under the surface. The past three months, we’ve seen things pick up, with jobs averaging 110k, which might not sound like much, but remember we made about 120k jobs all of last year. Should the labor market continue to improve in H2 as we expect, this will provide a nice backdrop for consumers and, potentially, for confidence.

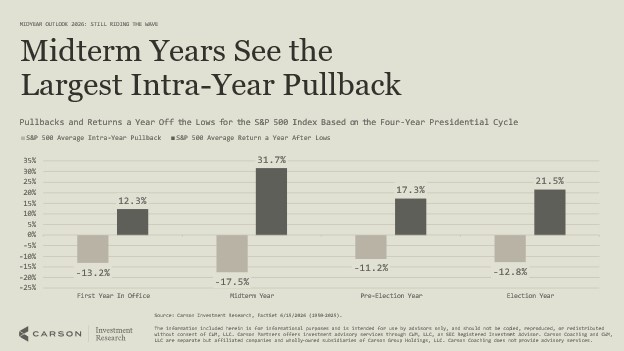

One big story for the back half of this year will be the midterm elections. We continue to stress not to mix investing and politics, but be aware that midterm years tend to be quite volatile. In fact, midterm years tend to see the largest peak-to-trough correction in the four-year presidential cycle, but stocks have also been up more than 31% per year off those lows and have never been lower. No pain, no gain comes to mind here.

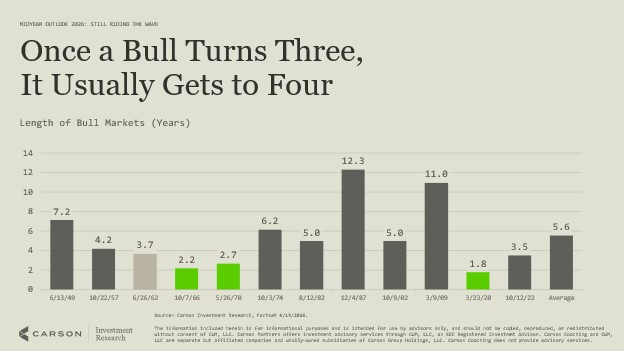

One big concept we’ve shared for a couple of years now is that this bull market isn’t as old as you might think. We found that once prior bull markets made it past their third birthday (which was last October for our current bull market), they usually made it to at least their fourth birthday, with many going many, many more years.

Additional takeaways from the 2026 Midyear Outlook include:

- Carson remains overweight equities relative to bonds, supported by an inflationary growth environment, strong earnings, expanding profit margins, and continued AI-related capital spending. It’s important to remember that gains come from fundamentals, not sentiment.

- The team believes recession risk over the next year remains low, with job growth improving, unemployment holding near historically low levels and nominal consumer spending running well above recent trends.

- Carson expects the 10-year Treasury yield to end the year near 4.5 percent, with a bias toward lower outcomes, and continues to target below-benchmark interest rate sensitivity within fixed income allocations.

- Carson continues to favor balanced global equity exposure, noting that while the U.S. remains the leader in AI innovation, the AI trade is broadening internationally and relative valuations outside U.S. large-cap growth have become more attractive with large gains in Korea and Taiwan.

- The team notes that midterm election years have historically brought larger market pullbacks, but also says investors should avoid letting political views drive investment decisions, as broader macro forces tend to matter more for markets.

We appreciate you reading what our team has to say about markets and the economy, as you have many places to get this information. No, we won’t always be right; we won’t always be wrong. But we will be honest, actionable, against the grain when the data supports it, timely, and we will do all we can to make sure what we say is easy to understand.

You can read the full report here.

For more content by Ryan Detrick, Chief Market Strategist, click here.

9022180.1. – 14JULY26A