Technology earnings season for the second quarter is fast approaching. Investors are facing the most divergent performance among sector constituents in recent history, with semiconductors having surged in performance while software continues to struggle. Capital expenditures and revenue growth are likely to be under scrutiny this earnings season as companies try to show they’re on the right side of change.

An Historic Gap

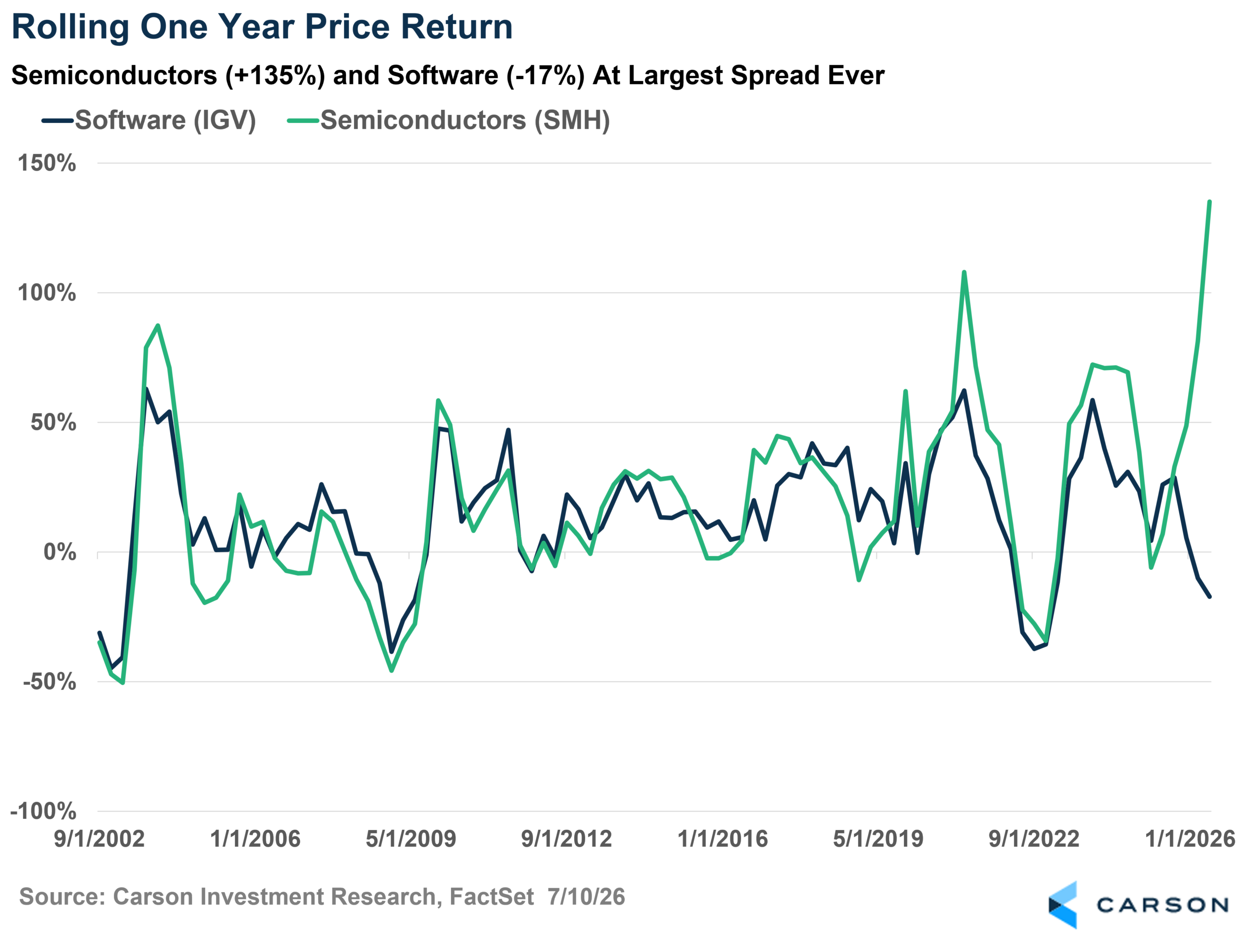

The technology sector in public stocks is dominated by two industries – semiconductors and software. Historically, these two industries grew and shrank in relative harmony, as it was perceived that their fates were intertwined. But that’s changed in 2026! Price performance between the two industries has never been wider. As shown below, semiconductors (SMH) have returned an astounding 135% over the past year ending June 30, 2026. Meanwhile, software (IGV) returned -17% over the last year, leading to a 152% difference in price performance. This is the largest one-year performance spread ever between the two industries since these two ETFs were introduced in 2001.

Capital Spending Fuels Semiconductors

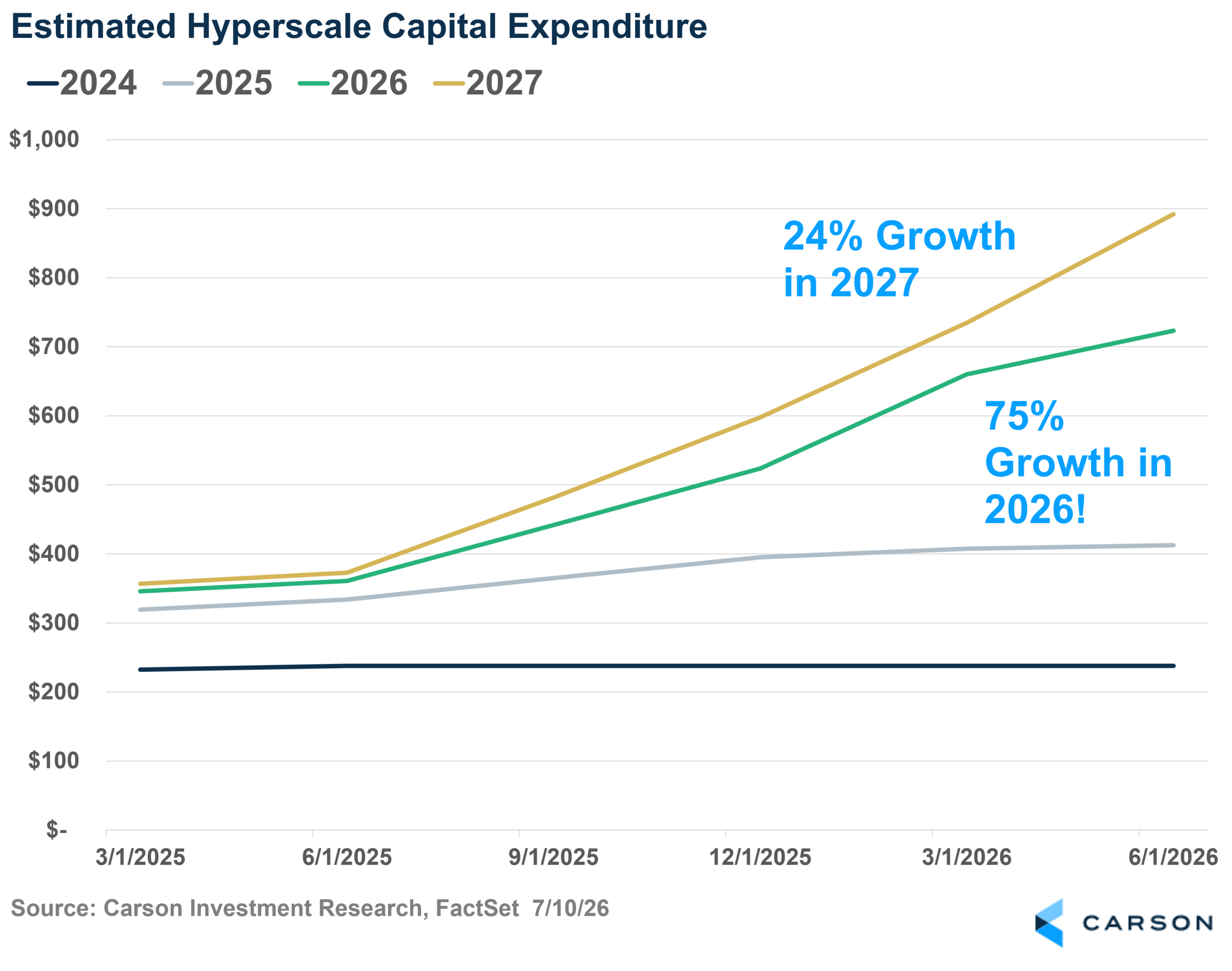

A main driver of the performance of semiconductor stocks has been the capital spending boom from hyperscale cloud computing companies (mainly MSFT, AMZN, META, and GOOGL). As shown below, these spending estimates have only increased as of late. Cumulative CapEx in 2026 for the hyperscalers now stands at an estimated $723 billion according to FactSet as of 6/30/2026, up from $660 billion on 3/31/2026.

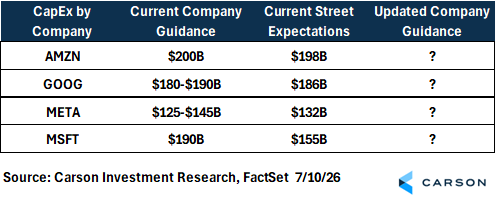

Below is a company-by-company breakdown of current guidance and street expectations for CapEx. With semiconductors having run so far, investors may be expecting company guidance to be raised.

Software’s Struggles

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

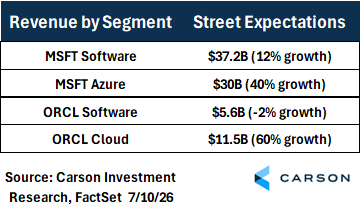

Software has struggled in the past year as the market believes this CapEx will equip AI with tools to severely disrupt current industry business models. And the numbers don’t lie. As shown below, two software heavyweights (Microsoft and Oracle) are expected to have their data center-focused business significantly outgrow their once-core software businesses. Are they ahead of the times by equipping their software with homegrown AI, or are they looking to ensure the future of their enterprises by diversifying revenue streams, perhaps at the cost of their legacy business? A slowdown in software growth and an acceleration in data center growth may likely be deemed by investors as an implicit admission that these businesses are competing against each other instead of complementing each other. However, an acceleration in both businesses may prove that the two can thrive in harmony and rewrite the script of Software’s Struggles.

Investors this earnings season will have to deal with uneven bars. The surge in semiconductors comes on the heels of heightened capital spending expectations, while software’s struggles continue to linger. Many high-profile software firms have pivoted to aggressively spending on data centers, but the debate remains whether this is to ensure or enhance their income streams. As results flow in, semiconductor investors will keep a keen eye on spending expectations. With such a large return dispersion between industries, expectations vary widely.

For more content by Blake Anderson, CFA®, Director, Portfolio Management, click here.

9019247.1. – 13JULY26A