News of a potential ceasefire deal hit Tuesday evening, and markets didn’t wait around. The S&P 500 surged 2.5% on Wednesday, the Dow gained 2.85%, and the Nasdaq rallied 2.8%. The S&P 500 is now down less than 1% year-to-date. The Dow is actually in the green.

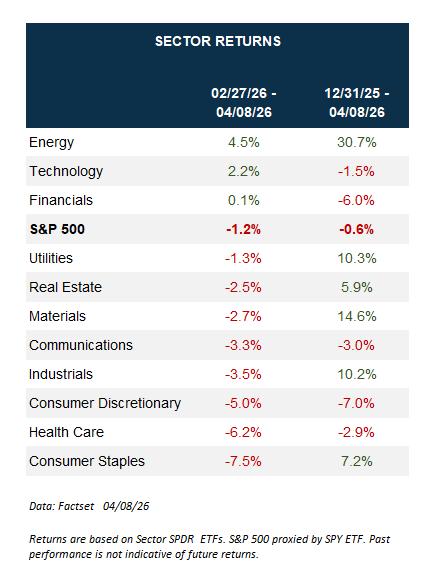

That’s the good news, and it’s worth acknowledging. A broad-based rally across sectors, cap sizes, and geographies is exactly what you’d want to see from a legitimate de-escalation of geopolitical risk. Industrials and materials led the day, up 3.7% and 3.3% respectively. Small caps outperformed large caps. International stocks surged, the MSCI EAFE gained 4.7%, and MSCI EM gained 5.5%, aided by a weaker dollar. Even the style box tells a constructive story: small value is now positive since the crisis began on 2/27 and is up nearly 10% year-to-date.

All of that points to a healthy, cyclical backdrop. The kind of environment where the underlying economy is doing real work, not just riding momentum from a handful of mega-cap tech names.

But the Bond Market Tells a Different Story

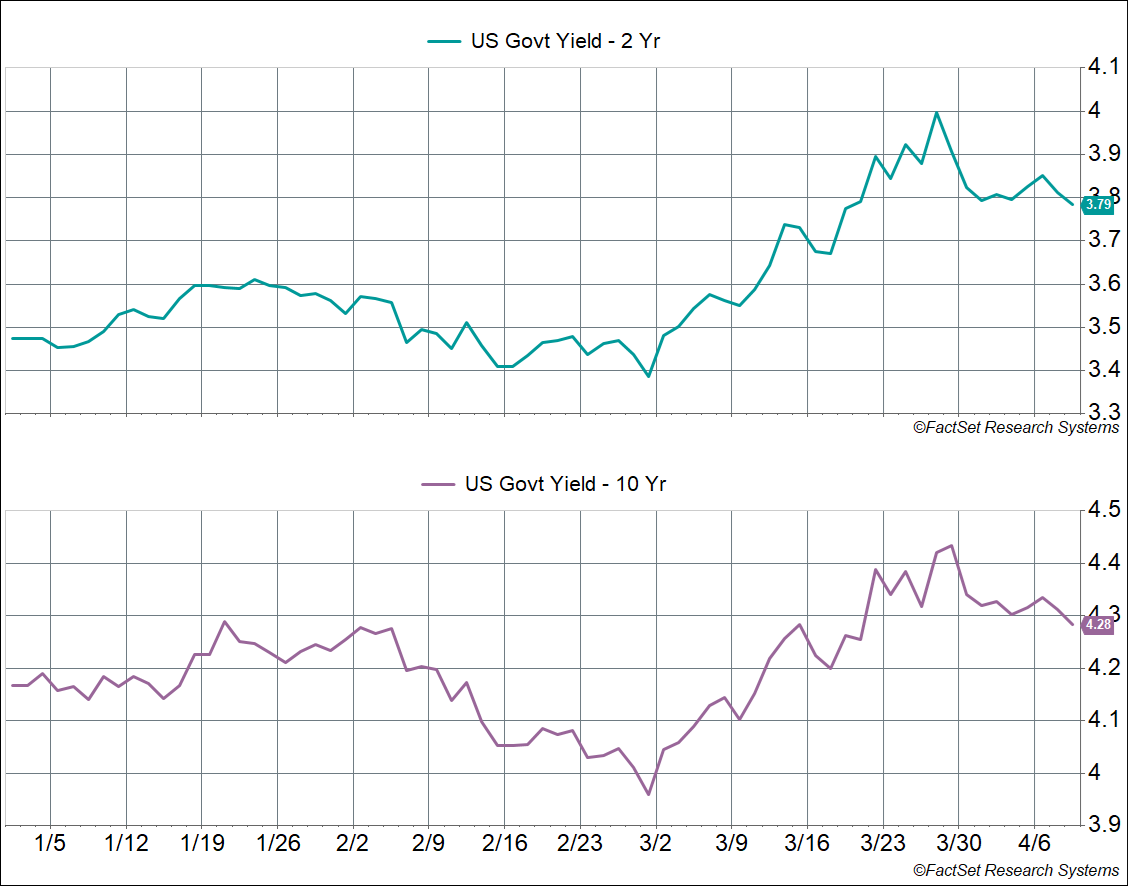

Here’s where it gets interesting. Yields barely moved on the ceasefire news. The 10-year pulled back just 3 basis points to 4.28%, and the 1-year yield actually rose 1 bp. For context, yields remain significantly higher than pre-crisis levels: the 2-year is up 40 bps since 2/27, and the 10-year is up 32 bps.

In short, the bond market is pricing in 1-2 fewer rate cuts over the next couple of years than before the crisis started. That hasn’t changed with the news of the ceasefire.

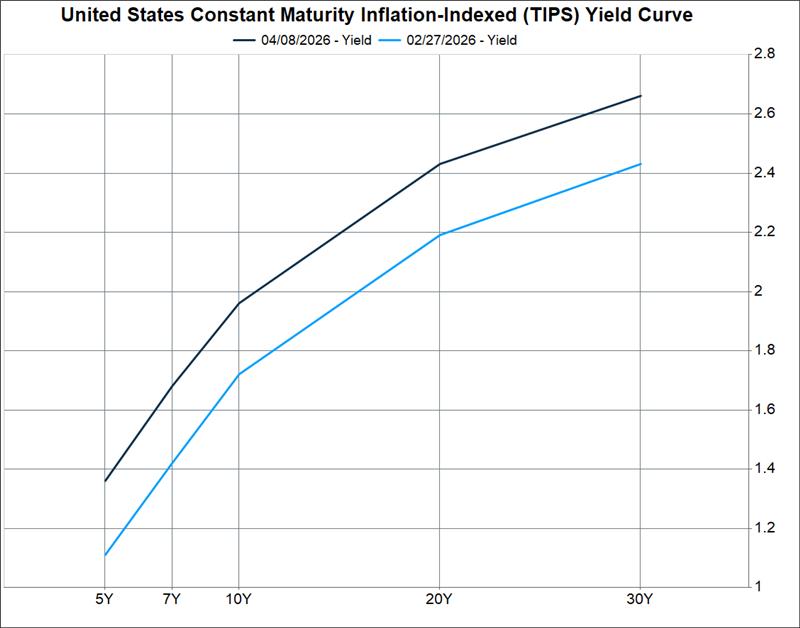

Perhaps more telling: real yields on TIPS barely budged after the announcement. The 5-year TIPS yield is up 25 bps since 2/27 to 1.36%, and the 10-year is up 24 bps to 1.96%. These real rates are well above the Fed’s own estimate of the long-run neutral rate of about 1%, suggesting the market thinks the Fed will need to keep rates meaningfully higher than the Fed expects to keep inflation contained.

The 30-year TIPS yield of 2.6-2.7% offers an attractive real return after inflation, which is a noteworthy level for long-term investors. But the reason it’s that high is because the market is telling us something uncomfortable: the inflation impulse from this crisis may not be easy to reverse, ceasefire or not.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Oil

Oil crashed on the news, as expected. WTI fell 16.4% on the day to $94/barrel. But here’s the pattern worth paying attention to: every time there’s been an apparent de-escalation since this crisis began, oil has dropped sharply, and then each successive low has been higher than the last. WTI hit $77 on the March 10 Trump comments, $84 on the March 23 comments, and $91 on this ceasefire. As of Thursday morning, WTI was already back up around $96.

The futures curve is telling a similar story. December 2026 oil is trading at $74/barrel, versus $64 pre-crisis, and December 2027 is at $70/barrel, versus $62/barrel. The spread between the two contracts has widened from $2 to $4, suggesting the market sees supply as tight even looking out more than a year. In other words, the oil market is not treating this ceasefire as the end of the story.

What This Means for Investors

The equity rally is welcome, and the breadth is encouraging. Cyclical leadership, small-cap outperformance, and international participation are all constructive signals for the economy. But the bond and oil markets are telling us that the inflationary consequences of this crisis have likely not been fully unwound.

That’s not a reason to panic, but it is a reason to stay diversified. As we wrote in our 2026 Outlook: Riding the Wave, the economy came into this crisis with real cushions: strong balance sheets, fiscal tailwinds, and solid earnings momentum. Those haven’t gone away. But the risk profile has shifted, and a well-diversified portfolio, one that accounts for the possibility that inflation remains stickier than expected, is more important now than it was at the start of the year.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8867908.1. – 9APR26A