Interest rates are the price of money. They touch everything: your mortgage payment, the cost of a new car, how much the government pays to service its debt, and how investors value every stock in their portfolio. And right now, the Federal Reserve is staring at a set of circumstances that makes its job harder than it has been in decades.

Huge thanks to Sonu Varghese, Chief Macro Strategist, for helping me put this together. With that being said, let’s walk through why.

How Interest Rates Work

Before we get into the current mess, it’s worth grounding ourselves in the basics because these concepts may matter a lot in the months ahead.

The Federal Reserve sets the federal funds rate, which is the overnight rate at which banks lend to one another. Think of it as the anchor for the entire interest rate complex. When the Fed raises or lowers this rate, it ripples outward: into Treasury yields, corporate bond rates, mortgage rates, auto loans, and eventually the cost of capital for every business in America.

The mechanism is straightforward in theory. When the economy runs too hot, and prices rise too fast, the Fed raises rates to make borrowing more expensive, slowing spending and investment, and cooling inflation. When the economy weakens and unemployment rises, the Fed cuts rates to make borrowing cheaper, which stimulates activity.

This is the dual mandate in practice: stable prices and maximum employment.

The problem is that this toolkit was designed for demand-driven economic cycles. The Fed can influence how much people want to spend. What it cannot do is create barrels of oil, reopen shipping lanes, or grow fertilizer. And that distinction between demand-pull inflation and cost-push inflation is the central tension of this moment.

The Inflation Backdrop: It Was Already Sticky

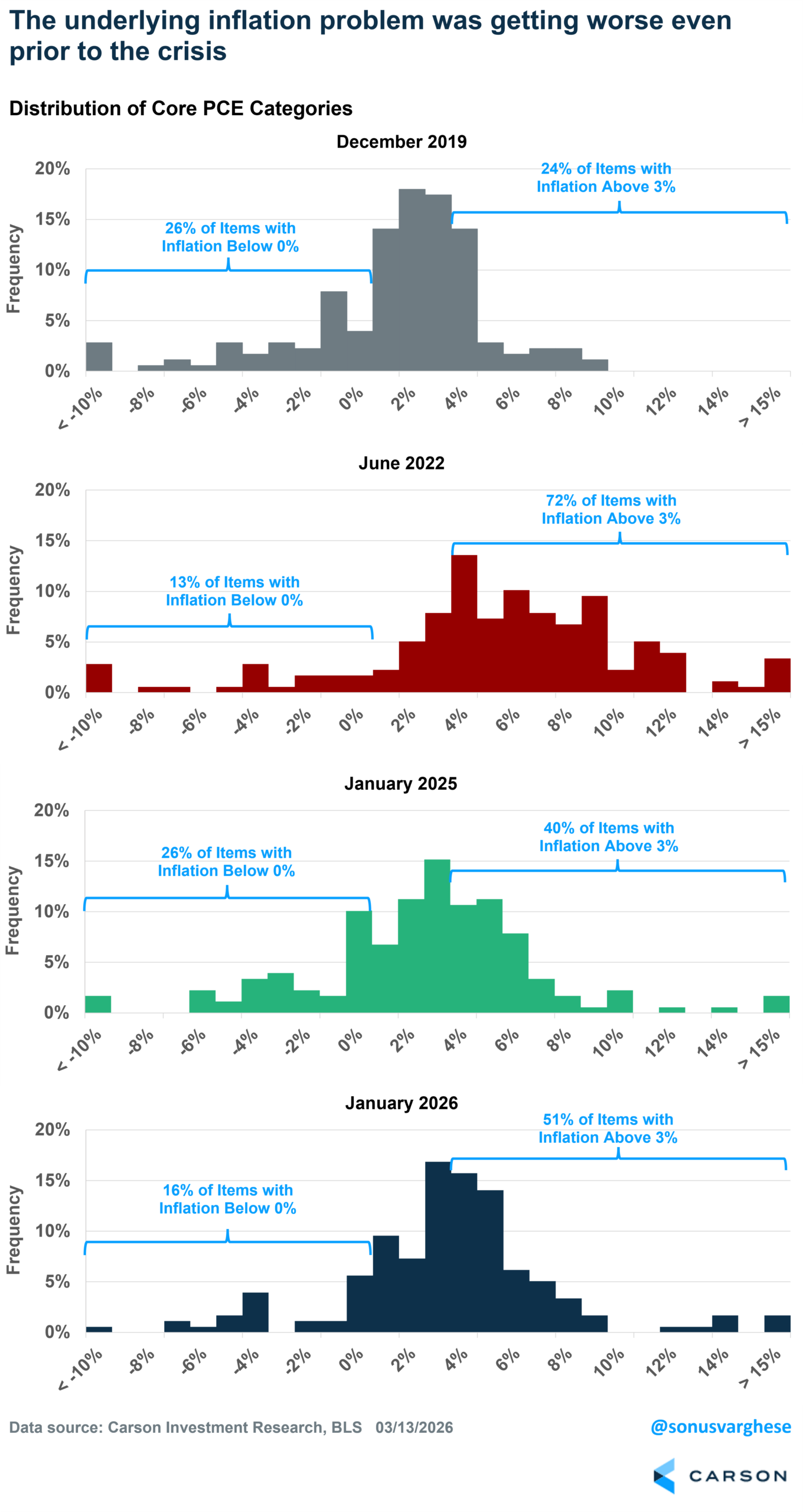

Even before the conflict in the Middle East, inflation was not cooperating with the Fed’s plan. As our own Sonu Varghese has detailed, core PCE was running at 3.1% year-over-year as of January 2026, well above the 2% target, and the breadth of inflation was widening, with over half of PCE basket items running above 3% (read more here). Core services (excluding housing), the category most sensitive to domestic monetary conditions, is running well above their pre-pandemic trend and accelerating.

At the March meeting, the Fed held rates steady at 3.50-3.75% and released projections that even Chair Powell acknowledged were essentially a placeholder exercise. The median dot implied one cut this year and one next year, with not a single member projecting a rate hike. As Sonu wrote in his post-meeting analysis, this beggars belief given both the pre-existing inflation trajectory and the Middle East supply shock layered on top of it (full analysis here).

The Fed is treating the energy shock as something it can look through. The question is whether that’s prudent patience or a repeat of 2021’s “transitory” miscalculation.

The Supply Shock: You Can’t Print Oil

The Strait of Hormuz closure has removed approximately 20 million barrels per day from global oil flows, roughly 20% of the world’s supply. Even with Saudi Arabia and the UAE rerouting oil through bypass pipelines (~6.5 million bpd capacity) and coordinated SPR releases (~3.5 million bpd flow), the world remains roughly 10 million bpd short. That is a physical shortage that no amount of monetary policy can fix. Like it or not, only politics can fix that, as the ceasefire (hopefully) takes hold.

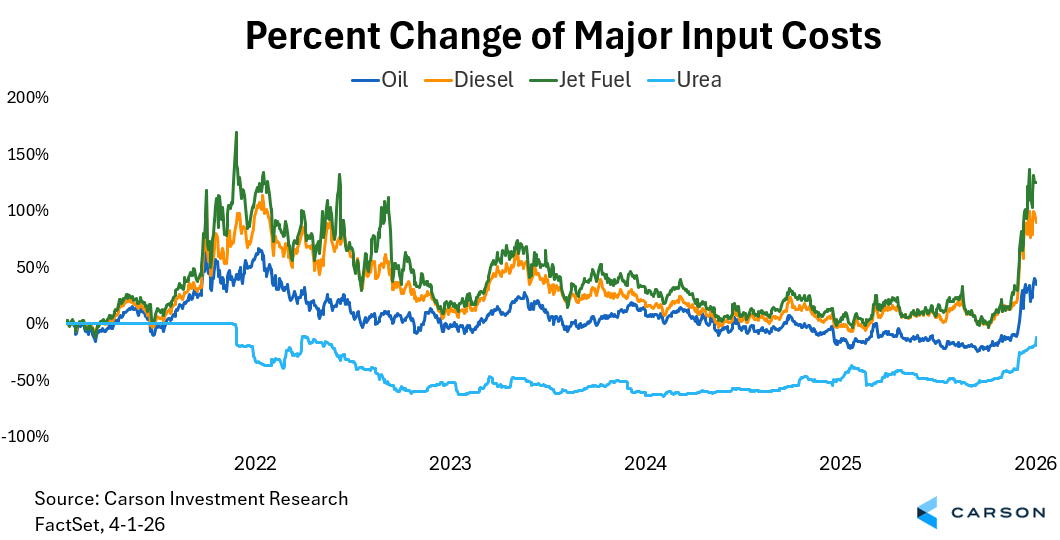

Gasoline accounts for less than half of U.S. petroleum product consumption. Diesel prices are up approximately $1.70 per gallon, even more than gasoline’s ~$1 increase. Jet fuel has surged to $4.62 per gallon at major U.S. airports. Urea, a critical fertilizer input manufactured from natural gas in the Persian Gulf, has spiked in price. Polyethylene, the building block of plastics, has surged in price. And helium, which is critical for semiconductor manufacturing, was supplied by Qatar through the Strait. That flow has stopped.

Here’s where timing matters: we’re in the middle of sowing season. Fertilizer shortages now mean lower crop yields 9-12 months from now, which may mean higher food prices long after the Strait situation resolves.

This is cost-push inflation at its purest. Prices aren’t rising because consumers are spending too much. They’re rising because the physical inputs required to produce goods and move them around the world have become scarce and expensive.

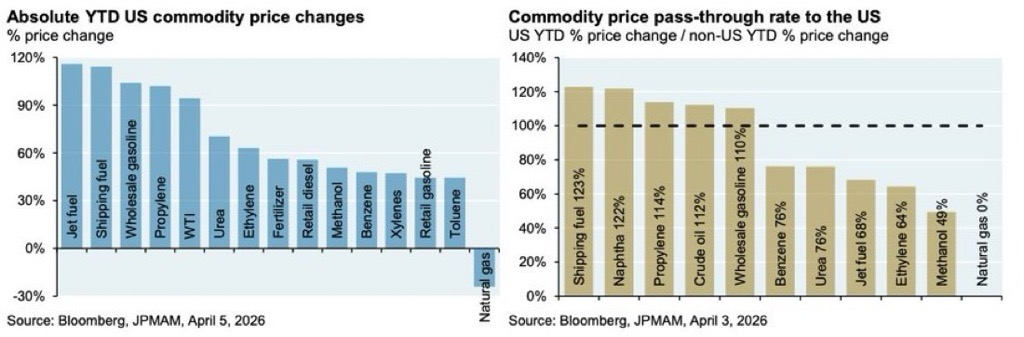

Note that while the US is “independent” from foreign oil production, we’re not immune from higher prices for commodities. That’s because prices are set globally, and this chart from JPMorgan illustrates, there’s a lot of pass-through from global commodity prices to US businesses and consumers.

Why Raising Rates Doesn’t Fix a Supply Shock

This brings us to the Fed’s core dilemma. The standard playbook for fighting inflation, raise rates to cool demand, was designed for a different kind of problem. When inflation is driven by excessive demand (consumers flush with cash, overheated labor markets, too much credit), higher rates pull demand back in line with supply. The medicine is painful but effective.

Cost-push inflation is fundamentally different. The problem isn’t that demand is too high; it’s that supply is too low. Raising rates won’t create more oil, reopen shipping lanes, or rebuild fertilizer supply chains. What it might do is raise borrowing costs across the economy, increase the government’s own debt service burden, crush rate-sensitive sectors like housing, and push unemployment higher.

The 1970s taught us exactly this lesson. After the 1973 OPEC embargo, the Fed under Arthur Burns adopted a stop-and-go approach: tightening policy when inflation spiked, then loosening when the economy weakened, then tightening again when inflation returned. The result was a decade of stagflation, where both inflation and unemployment remained stubbornly high. It took Paul Volcker’s willingness to push the fed funds rate above 20% and accept a brutal recession to finally break the cycle, but even then, the underlying supply disruptions had to ease.

The dynamic creates a vicious loop. The supply shock pushes prices higher. The Fed tightens to defend its inflation credibility. Higher rates slow the economy. Congress spends to offset the pain (especially in a mid-term year). Deficits widen. Bond supply increases. Long-end yields rise. The Fed’s tightening is partially offset by fiscal looseness. Inflation stays sticky. Repeat.

May 12 Is the Date to Watch

The March CPI report, which covers the reference month of March, the first full month of the Strait closure, is scheduled for release on April 10. That print will capture the initial surge in energy prices and will almost certainly show an uptick in headline inflation. But it will only be a partial picture.

The April CPI report, scheduled for May 12, will be the first print to fully capture the downstream effects of the supply shock: diesel feeding into shipping costs, jet fuel into airfares, and fertilizer into food production inputs. This is when the second-order effects start showing up in the data the Fed watches most closely. It’s also the data that will likely force the Fed’s hand on whether they can continue “looking through” the energy shock or need to change course.

Here’s the important nuance: the Fed normally uses “core” inflation (excluding food and energy) as its policy guide, specifically because energy prices are volatile and often don’t persist. But as several commentators have noted, core inflation excludes only energy directly purchased by consumers (gasoline and utility bills). It does not exclude diesel, jet fuel, or petrochemical costs that show up as higher prices for shipping, airfares, plastics, and virtually everything businesses produce. So even if the Fed tries to “look through” gasoline, the supply shock will contaminate core measures through the back door.

Fed Leadership Transition: Another Variable

Adding to the uncertainty, Chair Powell’s term expires on May 15. President Trump has nominated Kevin Warsh to succeed him. Warsh, a former Fed Governor from 2006-2011 who helped navigate the 2008 financial crisis, is known for hawkish views, particularly on the Fed’s balance sheet. He has historically been a critic of quantitative easing and has advocated for the Fed to return to a “Treasury-only” balance sheet.

The Senate Banking Committee is expected to hold confirmation hearings as early as the week of April 13. However, the process faces potential delays. Senator Tillis has vowed to block Fed nominees until an investigation into the central bank’s headquarters renovation is completed.

The practical implication for markets: we’re entering a period of genuine uncertainty about who will lead the world’s most important central bank in what could be the most challenging monetary policy environment since the early 1980s. Warsh may prove more or less hawkish than his reputation suggests. He has recently signaled he favors policy easing driven by AI productivity gains, but the uncertainty itself is a factor that investors should be aware of.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

What This Means for Markets

The bond market is not providing its traditional safe haven. When inflation is the dominant risk, stocks and bonds tend to fall together (read more about my 60/40 blog here). We saw this in 2022, and we’re seeing it again now. Since the start of the conflict, 2-year yields have surged nearly 50 basis points (to ~3.86%), and 10-year yields have jumped roughly 34 basis points (to ~4.28%). That means bond prices are falling even as equities are under pressure.

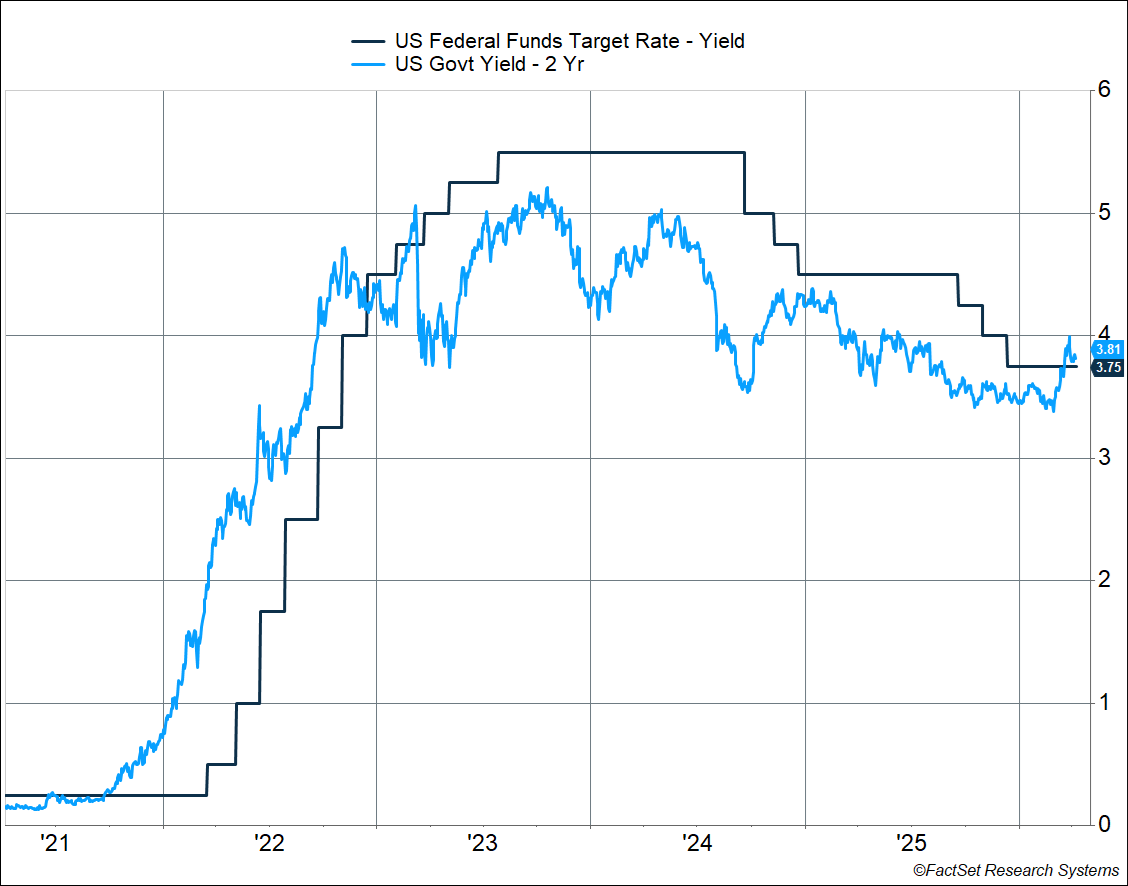

The Fed funds futures market. As of today, the market is pricing a 99.5% probability that the Fed will hold rates at 3.50-3.75% at the April 29 meeting. The probability of a hold extends deep into the year. Looking further out, the market doesn’t begin pricing meaningful probability of lower rates until well into 2027. Not a single member of the FOMC projected a rate hike in their March projections, but the 2-year yield trading above the fed funds rate for the first time since early 2023 suggests the bond market is at least contemplating the possibility.

Rate-sensitive sectors face the most direct headwinds. Housing, commercial real estate, utilities with high debt loads, and growth stocks whose valuations depend on low discount rates are vulnerable in an environment where rates stay higher for longer or even rise further. The maturity wall compounds this: companies that need to refinance in the next 18-24 months will do so at significantly higher costs, compressing margins and, in weaker cases, pushing toward distress.

Pricing power matters more than ever. In an inflationary environment driven by input cost increases, the companies best positioned are those that can pass rising costs through to customers without destroying demand. This has always been important, but in a supply-shock-driven regime, it becomes the single most critical characteristic to evaluate.

Duration is a risk. Short-duration fixed income continues to offer attractive yields (the front end of the curve is yielding 3.5%+) without exposing investors to the interest-rate risk embedded in longer-dated bonds. In an environment where the direction of long-end yields is uncertain, and the term premium is repricing higher, staying short on duration is a risk-management decision, not just a yield decision. This is why we are tactically overweight cash equivalents, as we wrote in our 2026 Outlook.

The Bottom Line

The Fed is navigating a genuinely difficult environment. Inflation was already sticky and broadening before the Middle East conflict added a massive supply shock on top. The standard toolkit, which adjusts interest rates to manage demand, is poorly suited to a supply-driven problem. Raising rates enough to slow inflation would risk triggering a debt refinancing crisis and recession. Cutting rates to support growth would risk further de-anchoring inflation expectations. Holding steady and waiting for data means the Fed is always reacting rather than leading.

None of this means a crisis is inevitable. The Strait could reopen if the ceasefire holds. The conflict could de-escalate. The Fed could thread the needle. But the range of outcomes is exceptionally wide right now, and investors should position accordingly. Favoring businesses with pricing power, keeping fixed income duration short, maintaining diversification beyond traditional stock-bond allocations, and staying disciplined rather than reactive.

By Harry McDonald, Analyst, Investment Research

8865015.1. – 8APR26A