How this works (a quick one-time intro): Each week during earnings season we will begin to publish a short read on how S&P 500 companies are doing. It’s built from FactSet’s Earnings Insight report (John Butters), with index and market-cap data from YCharts, aggregated in-house. Every figure ties back to FactSet’s published numbers; we simply add our take. We only publish during earnings season. You’re reading the first edition, but there’s a twist: we’re also at the finish line of this earnings season. Q1 is essentially in the books, so think of this as the season’s final scorecard rather than a mid-stream update.

Where things landed

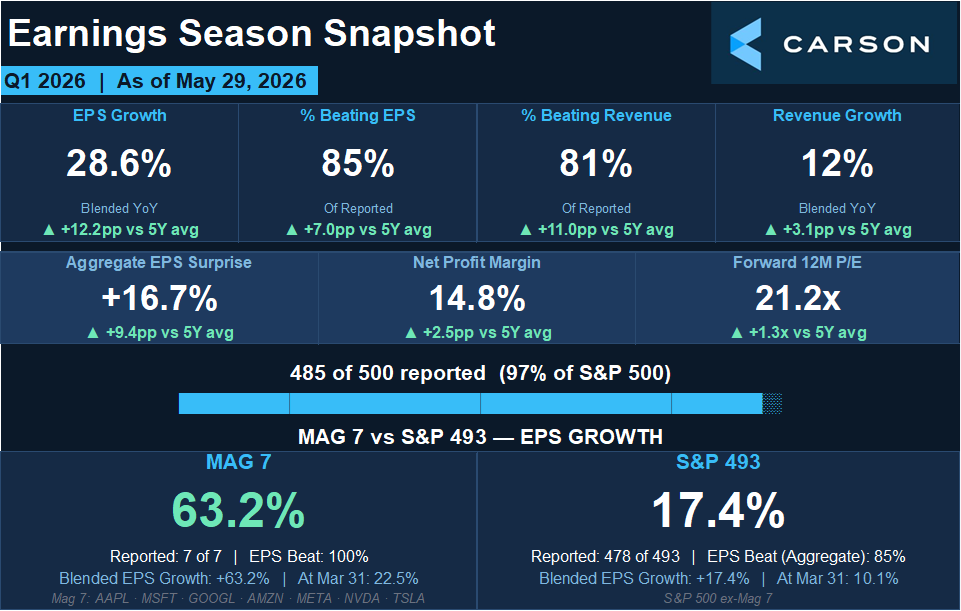

With 97% of the S&P 500 now reported, Q1 2026 earnings grew 28.6% from a year ago, which was the strongest quarter since late 2021 and the sixth straight quarter of double-digit growth. The number is impressive, but the climb is the real story: back on March 31, analysts expected just 13.1% growth, to which companies responded by more than doubling it.

Source: Carson Investment Research, Earnings Insight, FactSet May 29, 2026

85% of companies beat earnings estimates and 81% beat sales, both comfortably above their five-year norms. Profit margins hit 14.8%, the highest in FactSet’s data going back to 2009. Companies didn’t just grow; they kept more of every dollar than ever before.

So, What’s the Catch?

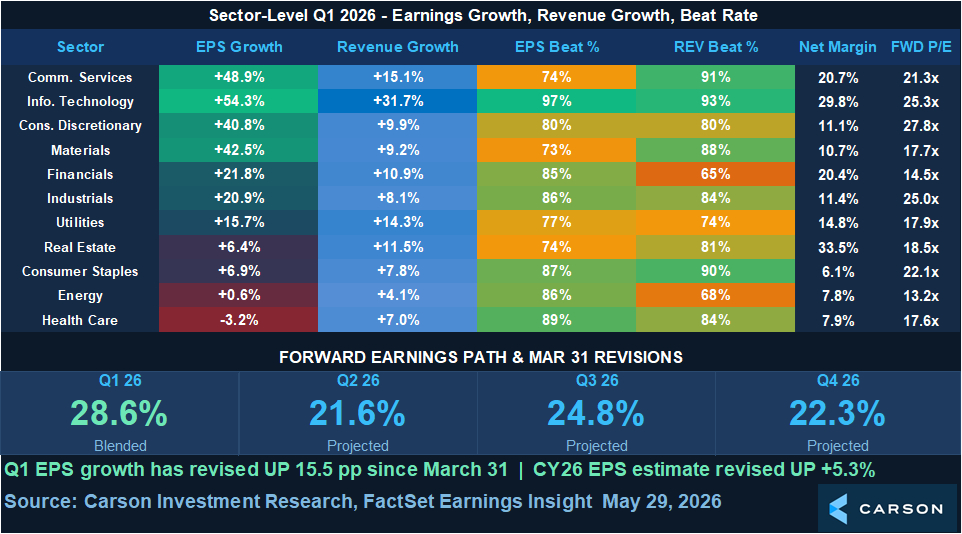

The megacaps drove an outsized share of the growth. Information Technology grew 54% but strip out NVIDIA and Micron and that falls to 30%. Communication Services’ ~49% turns into a decline without Alphabet and Meta. Consumer Discretionary’s 41% drops to 17% without Amazon. The quarter was genuinely strong, but it was also narrow, and that’s the thing we’d keep an eye on.

Source: Carson Investment Research, Earnings Insight, FactSet May 29, 2026

Alphabet, Amazon, Meta, NVIDIA, Microsoft, and Apple all posted sizable beats and carried the quarter. Health Care was the only sector to shrink from a year ago.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Why it matters going forward

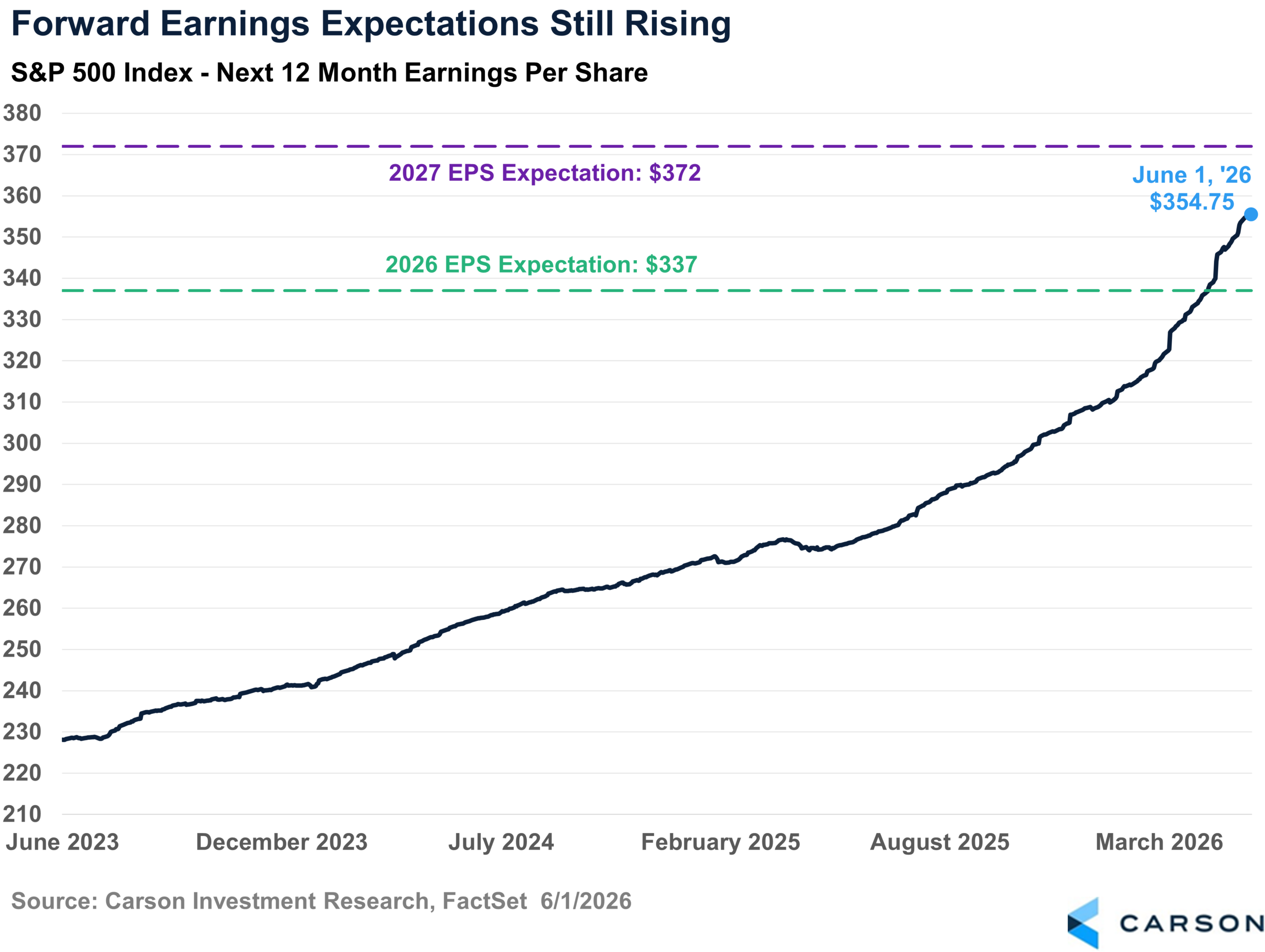

BUT there is good news! Instead of trimming estimates as the quarter played out, analysts continued to raise them. Expected earnings for the next twelve months continue to climb, now near $355 per share and still rising. In our opinion, that tells you the market sees more growth ahead.

The trade-off is valuations. At about 21x forward earnings, the market isn’t cheap. It’s above both its 5- and 10-year averages. Strong results are increasingly priced in, which raises the bar for what still counts as a pleasant surprise.

That 14.8% profit margin is an all-time high in FactSet’s records. S&P 500 companies have never turned this much of their revenue into profit.

Q1 2026 was a strong quarter: record margins, broad beats, and earnings that nearly doubled what analysts expected back in March. The watchouts are concentration and a full-priced market. Earnings season is now wrapping up, so we’ll go quiet until Q2 reporting kicks off this summer. Be back then with the weekly check-in.

By Harry McDonald, Analyst, Investment Research

8957848.1. – 2JUNE26A