You would be surprised how often I’m asked how many positions there should be in a portfolio or simply hear concerns that there are too many (or too few). A variant on this is concern about position sizes—more often that they’re too small, but occasionally that they’re too big.

The mushy but true answer is “it depends.” A robust portfolio can have many or few positions, but so can a poorly constructed portfolio. The real question is not how many pieces there are, but how intentional each piece’s role is (even if it’s very small) and how the portfolio is managed as a whole.

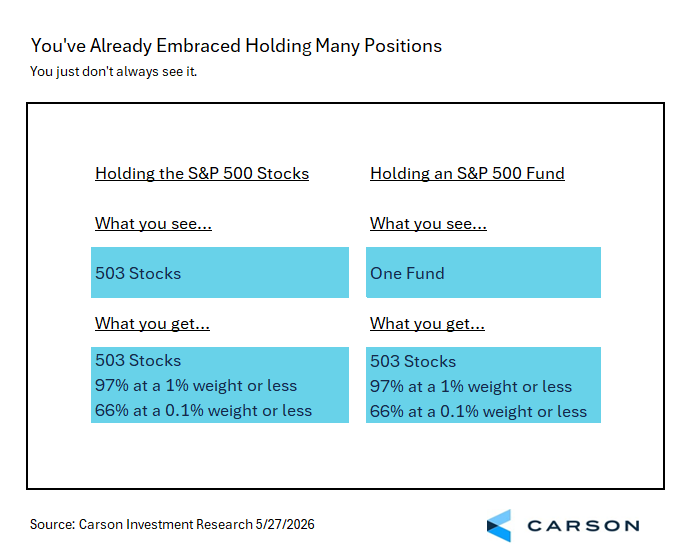

For example, a portfolio could hold all the individual stocks of the S&P 500 (in fact, there are currently 503 of them) at about the same weights they have in the S&P 500. In principle, no one should object to holding “all the stocks in the S&P 500,” whether as a standalone equity holding or as part of a larger portfolio. The S&P 500 is a diversified portfolio of stocks that roughly captures the risk and reward of publicly traded US companies, and it’s considered a reasonable proxy for exposure to the US economy through the lens of corporate America. In fact, the three highest AUM US-listed ETFs track the S&P 500 — they just come from different providers. On top of that, two of the three largest mutual funds also simply aim to track the S&P 500.

So if you wanted to build the S&P 500 on your own from individual stocks, there would be nothing in principle wrong with the allocation. It would be messy, your statements would be long, and you would have to own a lot of fractional shares, but there’s nothing wrong with the allocation itself. Now, if you did do that, 97% of your holds (488 stocks) would have a weight of 1% or less, and 66% of them (333 stocks) would have a weight of 0.1% or less. That’s a lot of very small holdings. But from a portfolio perspective, holding many very small positions is perfectly normal. We already do it all the time. We just don’t see all those holdings when it’s bundled together in a single security (an ETF or mutual fund), and that single security is usually a much more practical way to get the desired exposure.

While the wrapper is different and more convenient, the allocation remains the same. So by holding an S&P 500 ETF, you’re embracing that it’s entirely reasonable to hold lots and lots of individual positions at under 0.1% as part of a well-constructed portfolio. (In fact, there are times the individual positions may be preferable. For example, holding the individual positions can create a lot more opportunities for tax loss harvesting.)

Here’s a quick overview, from my experience as a portfolio manager, of times when more security holdings could be harmful or beneficial.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

10 Ways Complexity Can Harm a Portfolio

- Adding positions without being aware of how the positions or groups of positions impact overall portfolio behavior.

- Having a collection of pet tickers that once looked good but that you can’t let go of.

- Adding positions just to tell a story.

- Creating concentration risk in a portfolio with an unknown payoff (see my prior blog on the perils of stock picking).

- Betting on red and black (two positions that end up completely canceling out, although one or the other will always “work”).

- Accumulating a heap of tickers that end up just replicating a benchmark.

- Holding tickers that add unknown or unintentional risk.

- Mistaking a long holdings list for diversification when the underlying exposures are highly correlated.

- Creating a portfolio that is too complex to monitor, explain, rebalance, or tax-manage effectively.

- Owning overlapping funds, ETFs, or stocks without recognizing that the same economic exposures appear repeatedly.

- And the overriding principle of all of these is adding complexity with little benefit at a higher cost.

6 Ways Complexity Can Benefit a Portfolio

- Efficiently enhancing targeted risk control.

- Efficiently improving diversification while not losing desired idiosyncratic risk or factor exposures.

- Adding targeted idiosyncratic risk when there is potentially a genuine informational advantage.

- Deliberately tuning exposure to sector, industry, size, value, quality, duration, credit, geography, currency, or other measurable risk factors.

- Implementing a systematic quantitative strategy.

- Creating deliberate opportunities for potential tax-loss harvesting.

The bottom line is that a lot can be achieved very simply and at low cost, and I often see portfolios that are needlessly complex for the wrong reasons. Very simple portfolios are often a good place to start and can do a lot of work, as I discussed in a prior blog, The Starting Point for Effective Portfolio Management.

But at the same time, there are many ways in which added complexity can enhance a portfolio, and sometimes it does even require a whole lot of added complexity. But complexity must come with an expected payoff, such as lower expected risk, higher expected return, or other features like better tax management or a portfolio intentionally aligned with a set of values.

But just because more sophisticated portfolio management often comes with more complexity doesn’t mean a more complex portfolio actually creates better opportunities. It may just be extra packaging with a higher price tag.

So my advice is don’t reject complexity or small positions out of hand. It’s perfectly reasonable to be suspicious, but the complexity may be justified. And be especially suspicious of a heap of individual stock holdings that add risk and complexity unless there’s a clear purpose. But there are cases where complexity should be embraced. Or, to paraphrase Einstein, keep things as simple as possible, but no simpler.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.

8947717.1. – 27MAY26A