The market cheered the July Consumer Price Index (“CPI”) inflation report released yesterday, August 13, 2025, but mostly because it was perceived to be good enough to keep the Federal Reserve (“Fed”) on track for a September rate cut. The market-implied odds for a September cut rose from 86% to 94% according to the CME Groups FedWatch tool. There is some important data yet to come before the next Fed meeting on September 16–17, but the Fed generally does not like to surprise markets and it’s rare for the Fed not to cut when the market-implied odds are greater than 90% heading into the meeting.

At least for the day, the markets seemed eager to embrace the more potentially rate-friendly environment. The Russell 2000 Index of small cap stocks jumped 3.0% compared to a still solid gain of 1.1% for the S&P 500. But things weren’t so happy in fixed income, likely on concerns by bond market participants that there was still some worrisome inflationary pressure underneath the surface and lower rates might increase inflation risk. The Bloomberg US Aggregate Bond Index was flat at 0.0% and the Bloomberg U.S. Government: Long Index fell 0.5%.

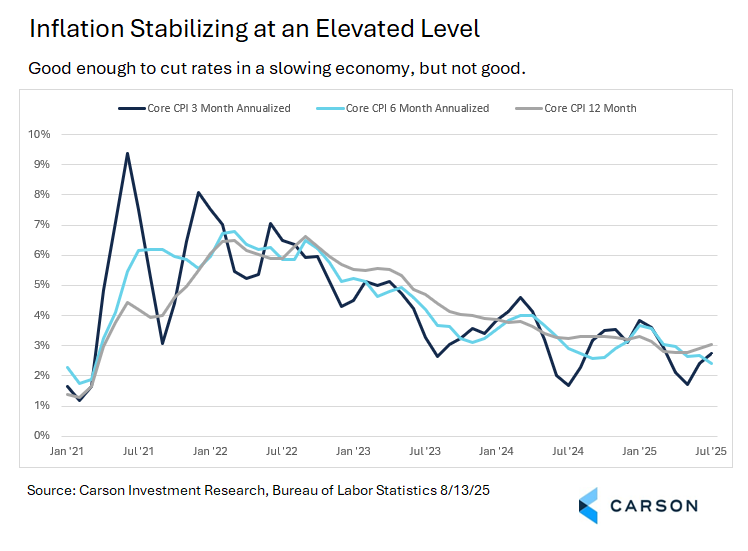

Despite the market response, the overall inflation numbers were not so much good as not as bad as feared. Headline inflation climbed 0.2% in July to take the one-year number to 2.7%, while core inflation (ex-food and energy) climbed 0.3% to take the one-year number to 3.1%, a five-month high. Core inflation at 3.1% is still a long way off from the Fed’s target of 2.0% (but keep in mind that Personal Consumption Expenditure (“PCE”) Index inflation, the Fed’s preferred measure, typically runs 0.2–0.4% cooler than CPI).

Overall, call the inflation data somewhat market friendly overall, but with quite a bit of potential risk (and therefore uncertainty) lurking beneath the surface.

Uncharted Waters

We subtitled our Midyear Outlook 2025 “Uncharted Waters” and a look at the July CPI numbers gives a sense of why. The inflation data cut across the prevailing narrative. Core goods excluding autos, which has been used as a proxy for tariff-sensitive inflation, slowed to 0.22% in July from 0.55% in June. On the other hand, there was concerning acceleration in “supercore” inflation (services inflation excluding energy and shelter), which climbed to 3.3% year over year, a five-month high. This signaled that we may be seeing inflation broadening out rather than remaining isolated to those areas of the economy most immediately impacted by tariffs. Despite the positive market reaction to the report, if inflation in fact is broadening it could make the Fed’s task more difficult.

The slowdown in core goods ex-autos does suggest that consumers are not yet bearing the full brunt of tariff-induced price increases. The most likely reason for the softer-than-expected reading is that pre-tariff inventory is still making its way through the supply chain, a factor that’s on the clock, especially with the return of reciprocal tariffs in August. Other factors may include weakening demand as the economy slows and some absorption into company margins. It’s also possible that companies are finding some loopholes to blunt the impact of tariffs. If these factors stay in play, it could be that economists misjudged the impact that tariffs would have on inflation, which could be part of the picture, but we think it’s more likely they misjudged the timing of the impact

None of these factors guarantee that goods inflation will stay tame—it’s likely we’ll see continued pressure—but for now the pass-through looks manageable. But two major seasonal sources of demand for goods purchases—back to school and holiday shopping—are around the corner and the risk remains that as seasonal goods demand rises, inventories turn over, and newly implemented reciprocal tariffs starts to bite, the impact of tariffs on goods inflation will become more prominent.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

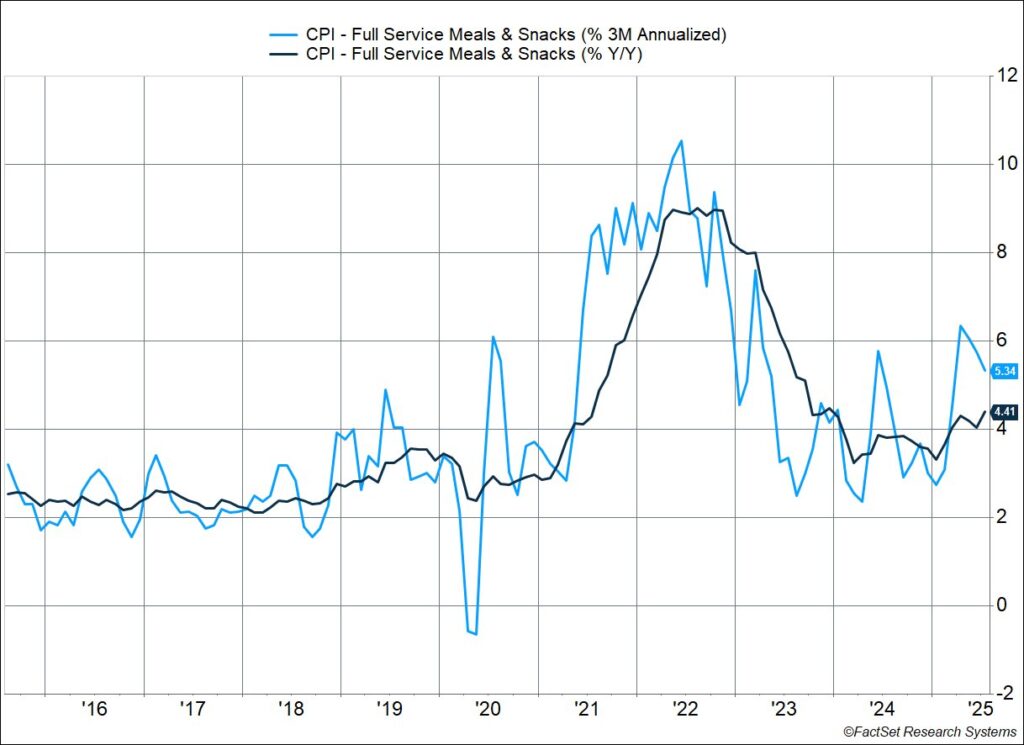

Watch Food Services

We like to keep an eye on CPI for “full services meals and snacks,” primarily seated restaurants, to gauge underlying inflationary pressure. That’s because it combines several drivers of inflation including:

- Worker wages

- Food inflation, and even energy prices (including transportation)

- Rent of restaurant premises

Inflation for restaurant meals is running at a 5.3% annualized pace over the past three months, a slowdown from the previous month but still quite elevated, and 4.4% over the last year. That’s well above pre-pandemic levels and inf fact higher than at any point in the 2000s and 2010s, a levels inconsistent with “normal” 2% inflation.

Normally, we would say this is a symptom of underlying inflationary pressures driven by strong labor income. But we know worker wages are easing, and it’s unlikely higher rents are a problem, which means the source of inflation is underlying food prices, and probably energy and transportation costs.

Should the Fed Cut?

Should the Fed return to even a modestly aggressive cutting cycle, the primary risk is that the overall economy is not as weak as the post-jobs report narrative has made it out to be, and even if it is there may be more resilience built into the economy than meets the eye. We’ve talked about some of these factors in various contexts including:

- A surge in AI-related capital expenditures

- Strong consumer balance sheets

- No warning signs of a slowdown at this point from the stock market or credit markets

But even if the economy were more resilient, we’ve made the argument since the beginning of the year that rates don’t need to be as high as they’ve been sitting, a level the Fed still views as restrictive, with cyclical areas of the economy (housing, small businesses) bearing the brunt of higher rates even as the rest of the economy muddles through just fine.

We should also not lose sight of the segment of the economy that is most negatively impacted by lower rates, that is savers, including most retirees. Savers have been thrilled to be getting a more than 4% return on “cash” compared to the near zero interest rates of much of the 2010s. In fact, if rates are pulled down too quickly and inflation remains elevated, savers and retirees get hit twice, once on the lower return of short-term Treasuries and again on inflation eating up more of the return that’s left.

The Fed has put itself in a difficult position by not raising rates earlier this year as it gets pulled in two different directions by its dual mandate. Stubbornly elevated inflation (even more so now with tariffs, although not nearly at the levels seen in 2022) says don’t cut rates; a slowing economy says cut. The jobs report shifted the balance toward emphasizing a slowing economy and cutting, and that appears to be the path we’re currently on. Overall, that’s good for markets (and the economy), especially if we get a Goldilocks scenario:

- Just enough economic slowing to support several cuts

- Not so much economic slowing that the economy is at genuine risk of going into recession

- Just enough forces containing inflation that the rate cuts don’t eventually force the Fed back to a hiking cycle

Right now, we appear to be in the Goldilocks zone. The stock market seems to think so, despite being in a volatile seasonal period. If we stay there, that would mean higher stock prices by the end of the year are likely, but it would also be an environment where continuing to diversify potential downside risk beyond bonds makes sense in case inflation comes back into play.

8281006.1.08.13.25A

For more content by Barry Gilbert, VP, Asset Allocation Strategist click here