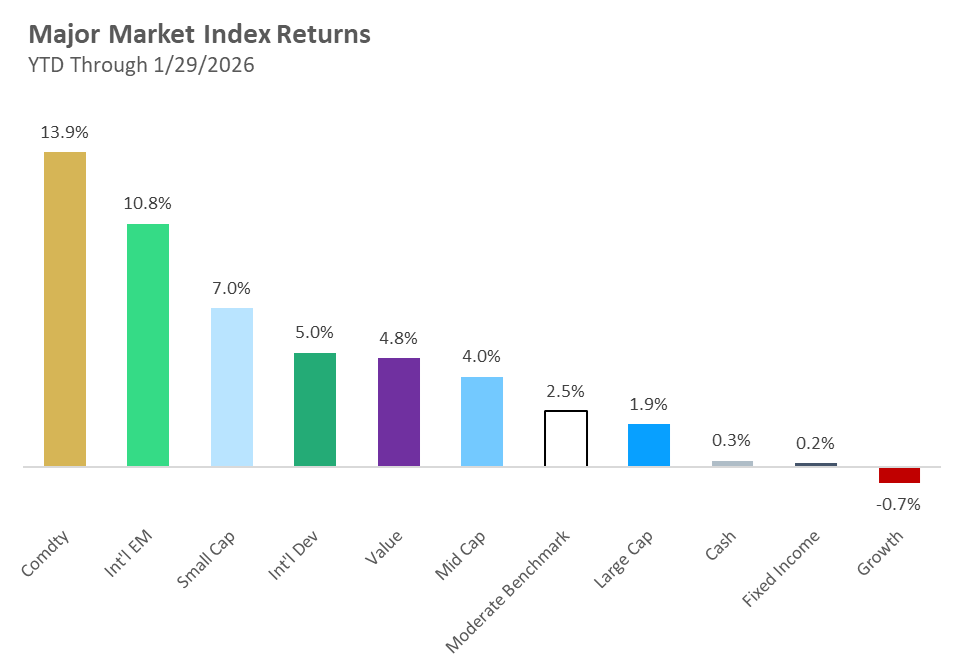

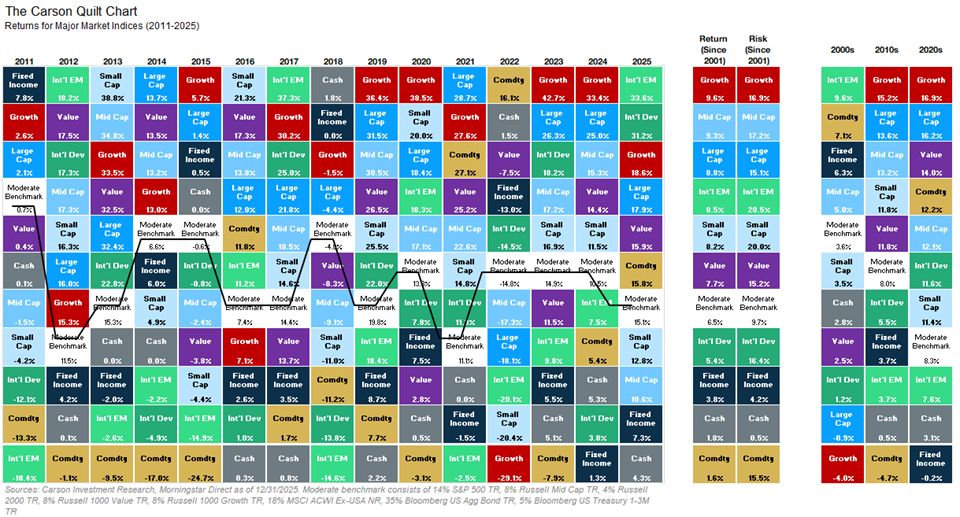

2026 is off and running, with an action-packed January and a further reminder that the oldest trick in the investing book still applies. That “trick” is, of course, diversification, which proved resilient in 2025 as we reminded investors in our 2026 Market Outlook. Now is an ideal time to consider the makeup and risk profile of portfolios. With what appears to be an exciting final day of the month still to go, returns in January bucked a lot of the trends from 2025, with other new trends emerging. Commodities – previously powered by precious metals – have expanded to include industrial metals, oil, natural gas, and now even grains have joined the party. Emerging markets, where many countries are closely tied to the price of commodities, have continued their run from last year as well. We are skeptical of Chinese market returns as part of EM, and we have already seen Chinese stocks turn into a laggard within the very diverse emerging market asset class. Small caps are the other standout so far this year. An asset class that has historically shown a “January Effect” is proving it again this year.

It has only been one month, but market action so far has important implications and considerations for portfolios. Commodities, emerging markets, and small-cap stocks are traditionally small pieces of most portfolios today – if they are present at all! We include commodities in many portfolios, but they are not explicitly in our multi-asset benchmarks (or many others out there).

The run for large-cap US stocks, particularly growth, has likely led portfolios to be overweight in the largest names in the market. Many of these large growth names are fantastic companies that have reshaped the world in many ways, but with those returns and valuations come higher expectations going forward. Just this week, we saw a prime example with Microsoft, currently the third-largest company in the world by market cap, which beat estimates for earnings and revenues but missed on certain spending metrics, sending shares plunging more than 10%, the equivalent market value of Netflix!

Fixed income, which we defined as the broad aggregate bond market, and cash (short-term Treasury bills) have had a slow start to the year, but that is part of the experience for these assets. We expect the yield for fixed income to be the largest driver of returns going forward, not capital appreciation potential, as we saw for a decade following the Great Financial Crisis. So far in January, we only had 1/12 of the expected yield of a fixed-income portfolio for the year. High-quality fixed income continues to be an important part of a diversified portfolio, but as we have mentioned in the past, considering other diversifiers such as alternatives and real assets can help with portfolio construction.

We will write more about what January returns mean for the broader market and the rest of the year. Uncertainty is always part of investing, and the year ahead will undoubtedly present more challenges for investors, as every year does. It is important to remember the mantra – When in doubt, diversify it out.

For more content by Grant Engelbart, VP, Investment Strategist click here.

8747012.1. – 30JAN26A