The Majority of S&P 500 Returns This Year Driven by Positive Fundamentals

The S&P 500 price index has a year-to-date return of 12.0% (through September 12, 2025), and a total return (including dividends) of 13.0%. As many investors have witnessed, this has come on the back of a 25% total return in 2024, and 26.3% return in 2023. Significantly, over half the S&P 500’s return this year has come from profit growth.

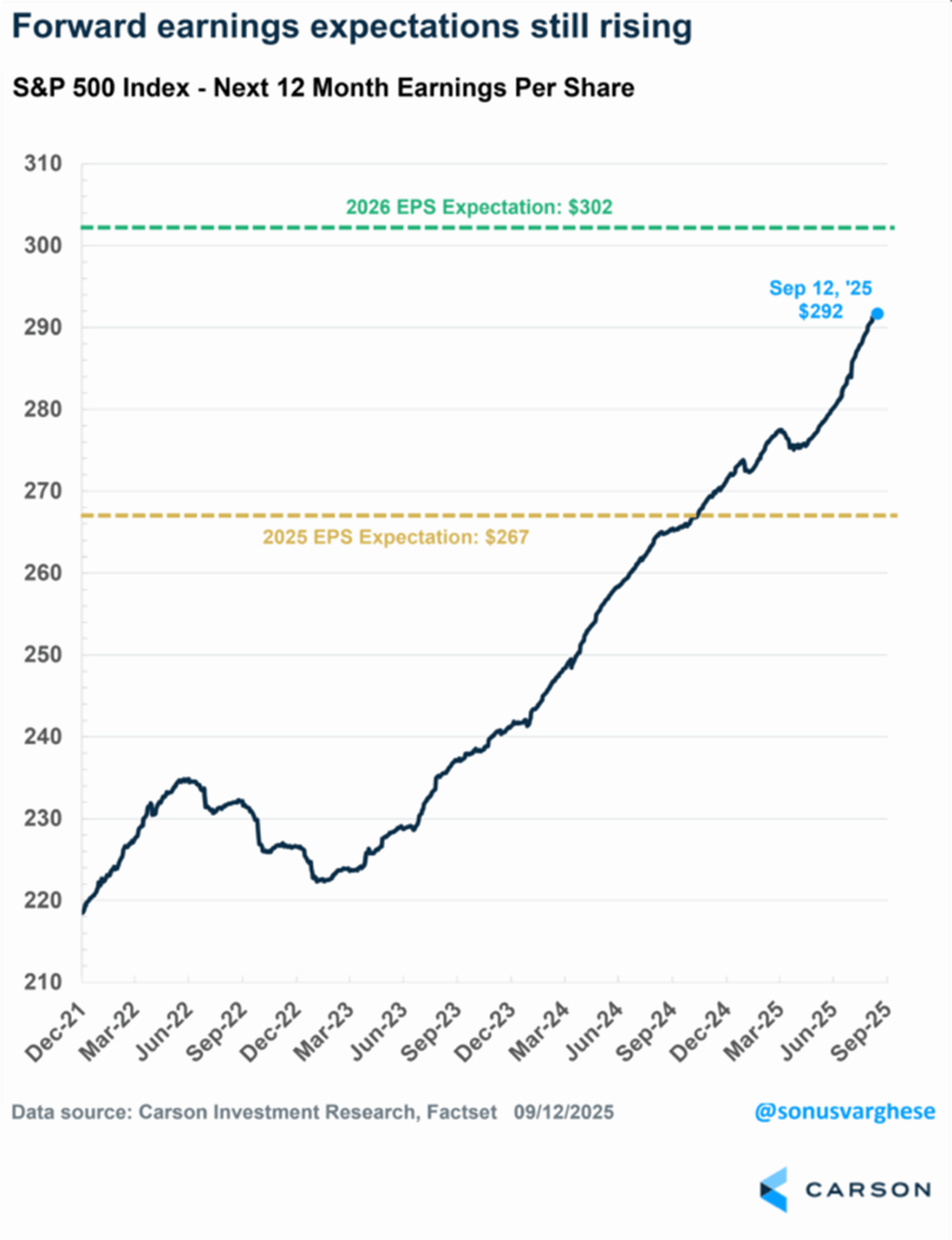

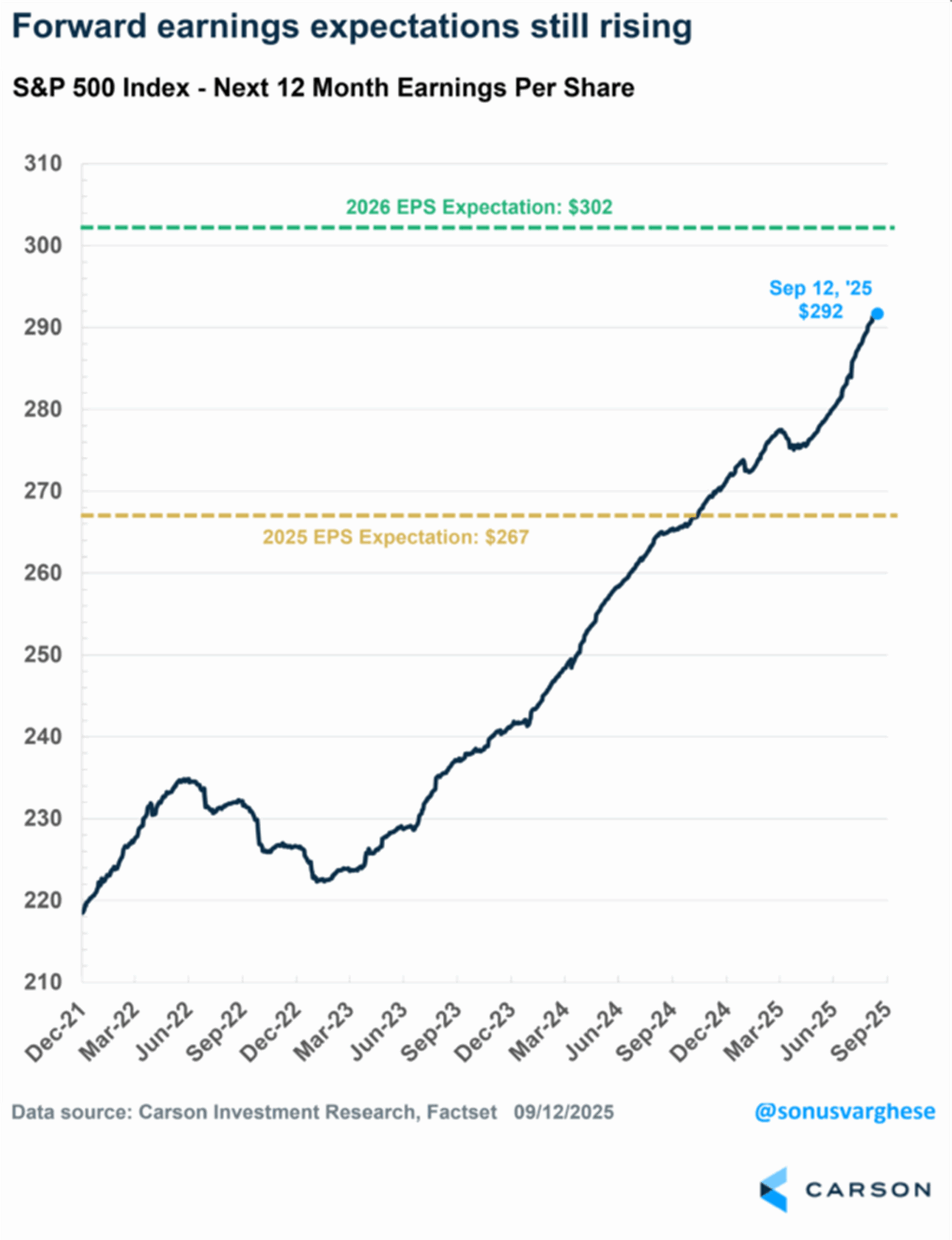

The S&P 500’s forward 12-month earnings per share (EPS) is currently at $292, up 7.4% year to date. Keep in mind that the next 12-month (NTM) EPS is now about 1/3 expected EPS for 2025 ($265) and 2/3 expected EPS for 2026 ($302). As we move forward, the NTM EPS estimate will increasingly be weighted toward the 2026 estimate. If the 2026 estimate remains above the 2025 estimate, we should see the NTM EPS estimate for the S&P 500 continue to rise. At the end of the year, the NTM estimate will match the 2026 estimate exactly.

Interestingly, both the 2025 and 2026 EPS estimates have eased by about 1.8%. But this also means the 2026 expected EPS growth rate hasn’t really changed, with earnings expected to grow 13.6% next year.

Profits Drove Most of the Returns

We can break down the S&P 500’s 13.0% YTD return into gains from profit growth, multiple growth (valuation changes) and dividends. Here’s what that looks like:

- Earnings growth contribution: +7.6% points

- Multiple growth contribution: +4.4% points

- Dividends: +1.0% points

In short, 8.6% points of the index’s YTD return has come from profits, both retained and distributed (dividends), or about 66% of the overall return.

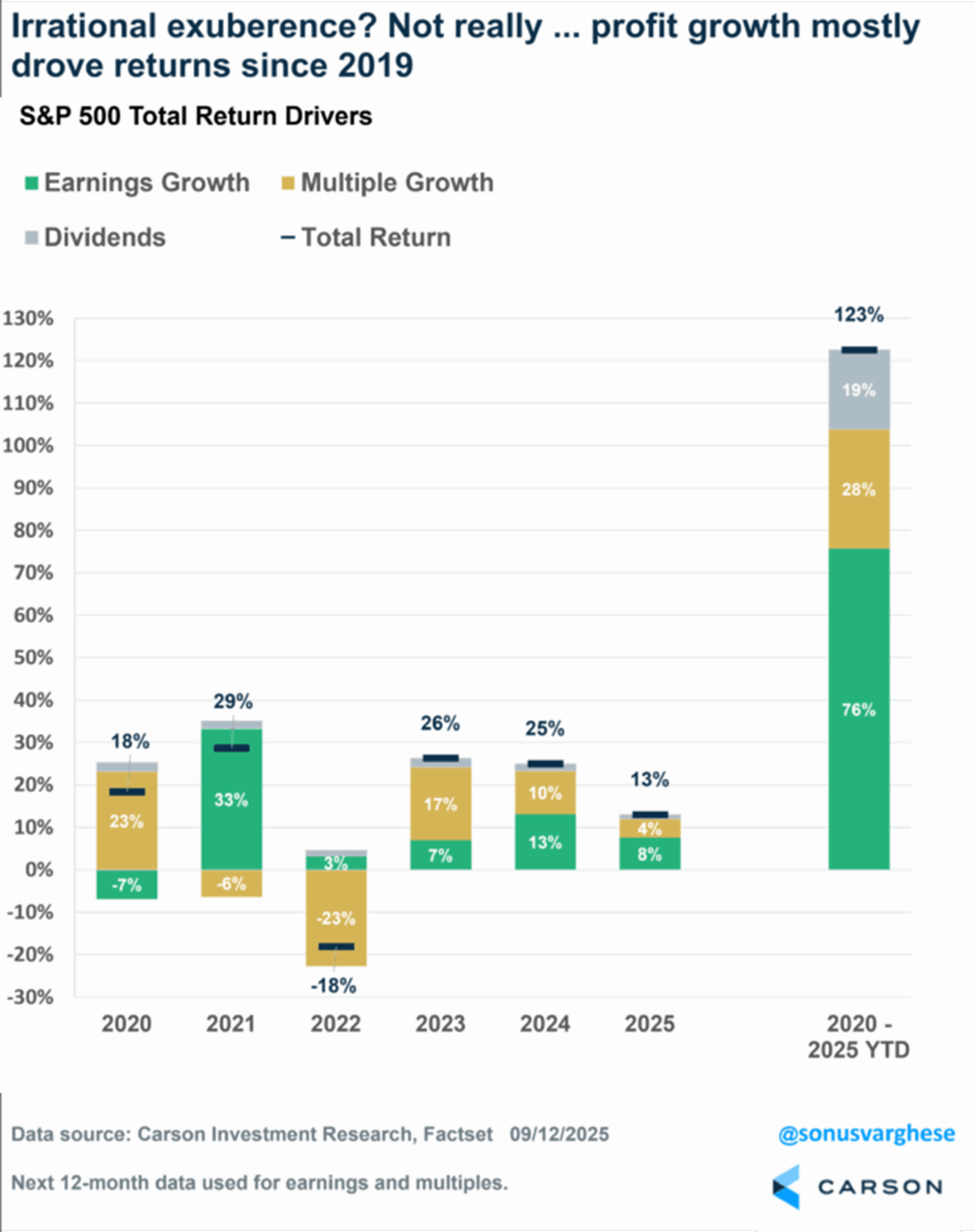

Zooming back over the past 5.5+ years (2020-2025 YTD), the S&P 500 has gained 123%. That return can be broken down into returns from:

- Earnings growth: +76% points

- Multiple growth: +28% points

- Dividends: +19% points

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

In other words, less than a quarter of the return over the last five and a half years (since 2019) has come from multiple growth, just 28% points out of 123%. Over three quarters of the return came from “fundamentals,” i.e. profit growth (including profits that were returned to shareholders via dividends). This doesn’t scream “bubble” or “irrational exuberance.” Rather, we believe it tells investors that American companies have figured out how to grow sales and profits across recessions, inflation surges, low-interest rate regimes and high-interest rate regimes.

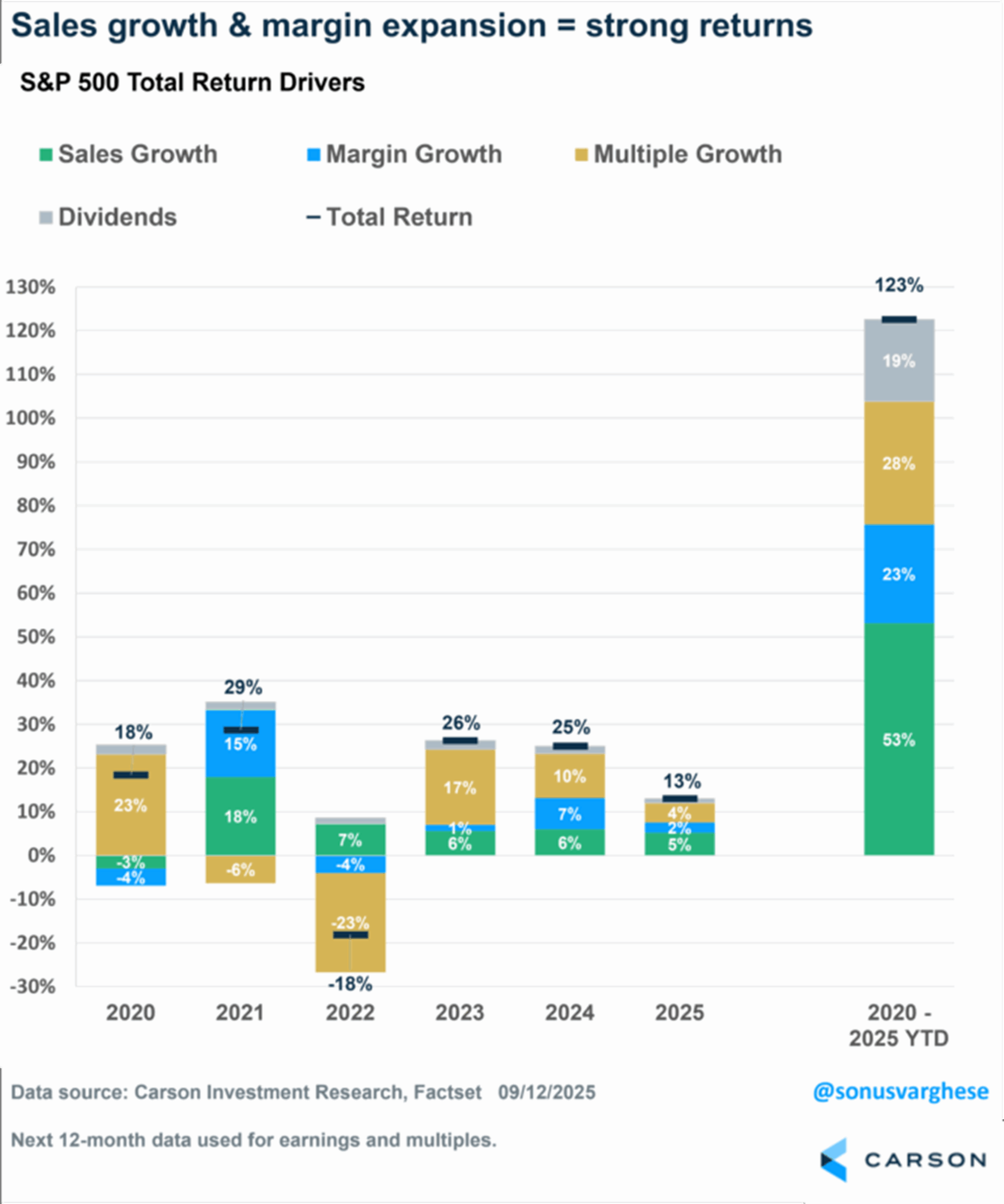

Margin Expansion an Important Driver of Profit Growth

Margin expectations have been a big part of the story over the last few years. Forward profit margins were just under 12% at the end of 2019 but expanded to 13.7% by the end of 2024, the highest on record for this series. Margin expansion stalled a bit earlier this year, but it has recovered recently and has reached a new high of 14.0%. Let’s look at how this has driven the S&P 500’s return.

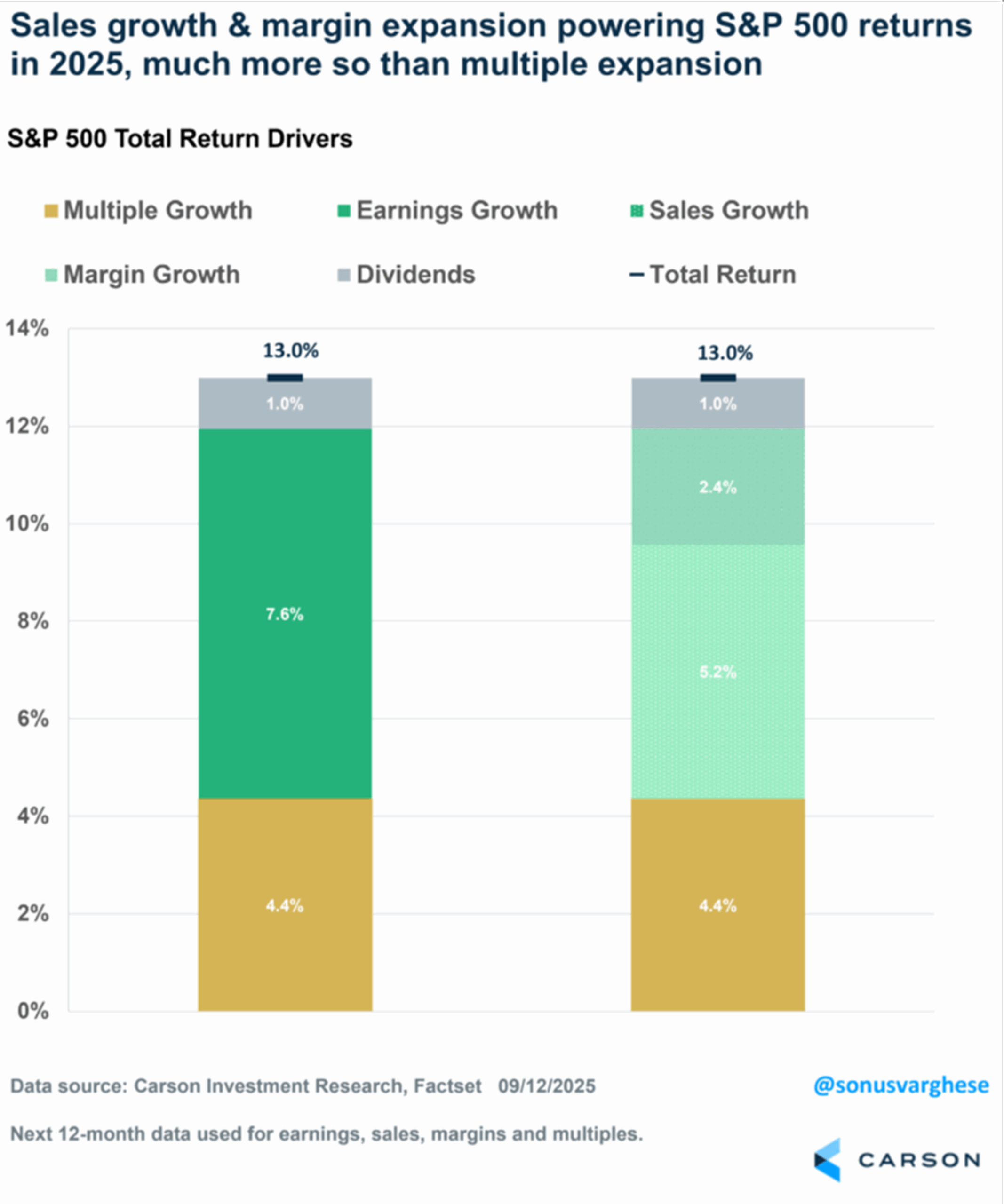

We can separate EPS growth into sales and margins. As I noted above, the S&P 500 is up 13.0% year to date, with contributions breaking down this way:

- Sales growth: +5.2% points

- Margin expansion: +2.4% points

- Multiple growth: +4.4%-points

- Dividends: +1.0% points

Returns were powered by a resilient corporate sector and an economy that has, so far, avoided recession. Sales rose thanks to nominal GDP growth. But margins are also expanding thanks to operating leverage.

Broadening the horizon to the last 5.5+ years (since 2019), and breaking down the S&P 500’s 112% return from 2020-2025 (YTD), here are the contributors:

- Sales growth: +53% points

- Margin expansion: +23% points

- Multiple expansion: +28% points

- Dividends: +19% points

We continue to believe that corporate fundamentals are constructive given the recent better-than-expected sales and earnings quarterly reports. Current valuations could be seen as being on the higher side historically; however, we believe that much of this is justified given margin expansion. In addition, dovish Federal Reserve policy as well as fiscal policy support should continue to support the present business environment, which, in turn, should fuel top and bottom line quarterly growth.

8406354.1.-09SEPT2025A

For more content by Sonu Varghese, VP, Global Macro Strategist click here.