Cost, quite rightly, is one of the first considerations investors look to when analyzing investment options. How much of an investment’s return is lost to costs? But what costs are they really referring to?

It seems that nine times out of ten, the discussion centers on the management fee of a product. Mutual funds, ETFs, SMAs, interval funds, and more bespoke solutions all carry some form of management fee tied to security selection and portfolio management. Even passive instruments, which have continued their multidecade rise to the mountain top of investor focus, come with management fees, albeit much lower (in most cases) than their active counterparts.

So that is it, right? We pay a management fee and an advisory fee, and that is the full cost of investing.

If only it were that simple.

In reality, several additional and often less visible costs can materially impact investor outcomes. These costs are frequently misunderstood or, in some cases, overlooked entirely. Let’s walk through them.

Tax Costs

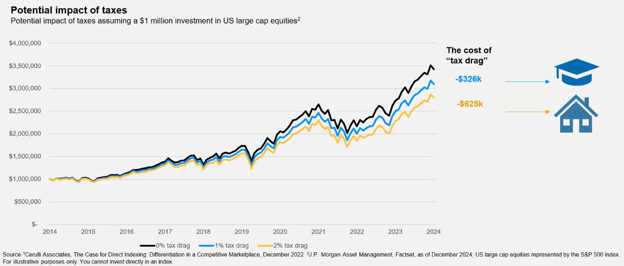

One of the most avoidable, yet least discussed, drags on portfolio performance is the tax cost of different approaches to investing. Put differently, that is the difference between the gross return a portfolio generates and the net return an investor actually keeps after taxes.

Under most circumstances, investors think about taxes only when an asset is sold. However, what often goes unnoticed is the annual income and capital gains generated by investment vehicles, which can trigger tax liabilities even when the investor has not sold anything.

Mutual funds, often viewed as the industry’s proverbial punching bag during this decade-long shift toward ETFs, are a prime culprit here. Because of portfolio turnover as a result of both security selection changes and flows, these funds may be forced to distribute capital gains each year. These distributions are largely independent of an investor’s holding period, their personal gain or loss, or their share of realized gains inside the fund. In years with elevated turnover and strong market performance, these distributions can climb into the mid-teens or higher.

This cost can be especially painful in down markets. Consider 2022, when many investors experienced double-digit losses while simultaneously receiving sizable capital gain distributions. Not only did portfolio values decline, but investors also faced an immediate tax liability. This effectively pulls capital out of the market, eliminating the opportunity for those dollars to remain invested and recover in market pullbacks such as 2022, let alone compound over time.

Inflation

Inflation is a silent, though recently much noisier, cost of investing. It steadily erodes the purchasing power of wealth and represents a persistent headwind for real returns (returns after adjusting for inflation).

In the United States, the Federal Reserve targets an annual inflation rate of 2 percent, a level broadly considered conducive to stable economic growth. In some environments, inflation acts as only a modest drag on returns. For example, in the post-Global Financial Crisis period but before the Covid-19 pandemic, inflation consistently ran below target.

In contrast, the 1970s demonstrated how damaging elevated inflation can be. During that decade, persistently high inflation made it difficult for markets to generate positive real returns.

Regardless of the level, inflation represents a structural cost of investing and a hurdle that portfolios must overcome. While it cannot be avoided, it can be addressed through thoughtful asset allocation, including exposure to investments better positioned to hedge inflationary pressures.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Performance Fees

While not universal, many private market and alternative investments include performance fees in addition to their base management fee. These fees vary by asset class, manager, and structure, but they are critical to understand when evaluating the true net return potential of an investment.

In some cases, performance fees may apply regardless of outcome, though more commonly, funds require a hurdle rate to be exceeded before such fees are charged. A well-known industry structure is the “two and twenty,” where a fund charges a fixed 2 percent management fee and retains 20 percent of profits as a performance fee.

These structures can meaningfully affect investor outcomes and should always be evaluated in the broader context of expected returns and diversification benefits.

Redemption Costs

Redemption costs are not present in every investment, but they can be significant in certain products. These fees typically arise when investors exit a strategy shortly after entering it.

In many cases, redemption costs function as early withdrawal penalties designed to encourage longer holding periods and improve asset stickiness for managers. Investors may be required to pay a percentage of their investment if they redeem within the first year or two following purchase.

While sometimes reasonable given the nature of the strategy, these costs should be clearly understood before allocating capital, particularly when liquidity needs may change.

Bringing It All Together

So the next time someone asks, “What is the cost?” or the next time you find yourself asking the same question, it is worth expanding the conversation beyond the headline fee.

Advisors should not only ask about management costs, but also compare how different vehicles and asset managers perform across tax efficiency, inflation sensitivity, fee structures, and liquidity constraints. Only then can we properly evaluate which investments are optimal, not just on the surface, but for the long-term outcomes our clients are investing to achieve.

By Shane Denton, Sr. Analyst, Investment

8983221.1. – 17JUNE26A