The recent market pullback has offered a useful reminder: in certain environments, traditional safe havens don’t behave the way you’d expect. Since the Middle East conflict escalated on February 27, both bonds and gold have failed to provide much cushion, and understanding why matters more than the headline.

Bonds: The Inflation Problem

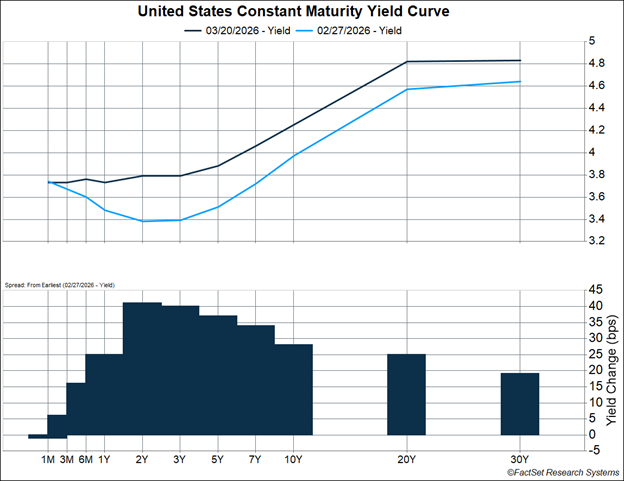

Treasury yields have moved sharply higher since February 27, with the 10-year climbing 45 basis points to 4.39% and the 30-year rising 33 bps to 4.96%. That’s the opposite of what typically happens during a risk-off episode, when investors would normally flock to bonds and push yields lower.

The culprit is inflation. The Middle East conflict is widely expected to push energy and broader prices higher, prompting markets to dramatically reprice Fed rate-cut expectations. Before February 27, markets anticipated two to three cuts in 2026. Now they’re pricing in roughly none, and futures markets are showing rates rising again from 2028 onward, reflecting the view that inflation may remain a persistent headache well beyond this year.

Just before the conflict began, yields were near multi-year lows: the 2-year had hit 3.37% (its lowest since September 2022), and the 10-year was at 3.94% (its lowest since October 2024). Since then, yields have surged further. The chart below shows the most current picture through March 20.

That duration risk matters for bondholders. The iShares 7-10 Year Treasury ETF (IEF) carries an effective duration of about 7.0 years, meaning a 1% move in rates translates to roughly a 7% swing in price. Not exactly the “risk-free” stability investors might be counting on.

Rate Cuts: Fully Priced Out

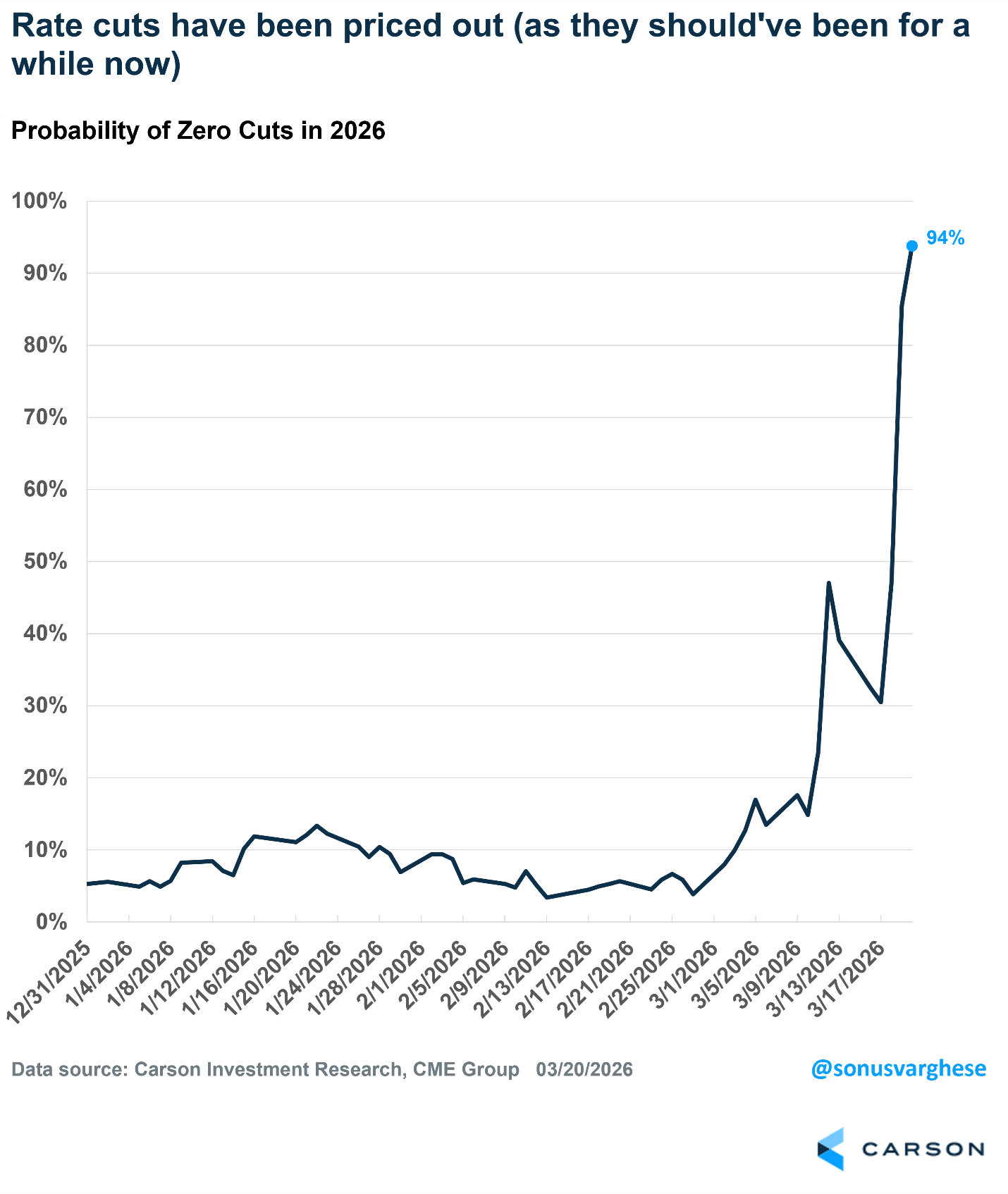

The shift in rate expectations has been dramatic. The probability of zero Fed rate cuts in all of 2026 has gone from around 5% before the crisis (on February 27) to 94% as of March 20 — a complete repricing of the rate outlook in three weeks.

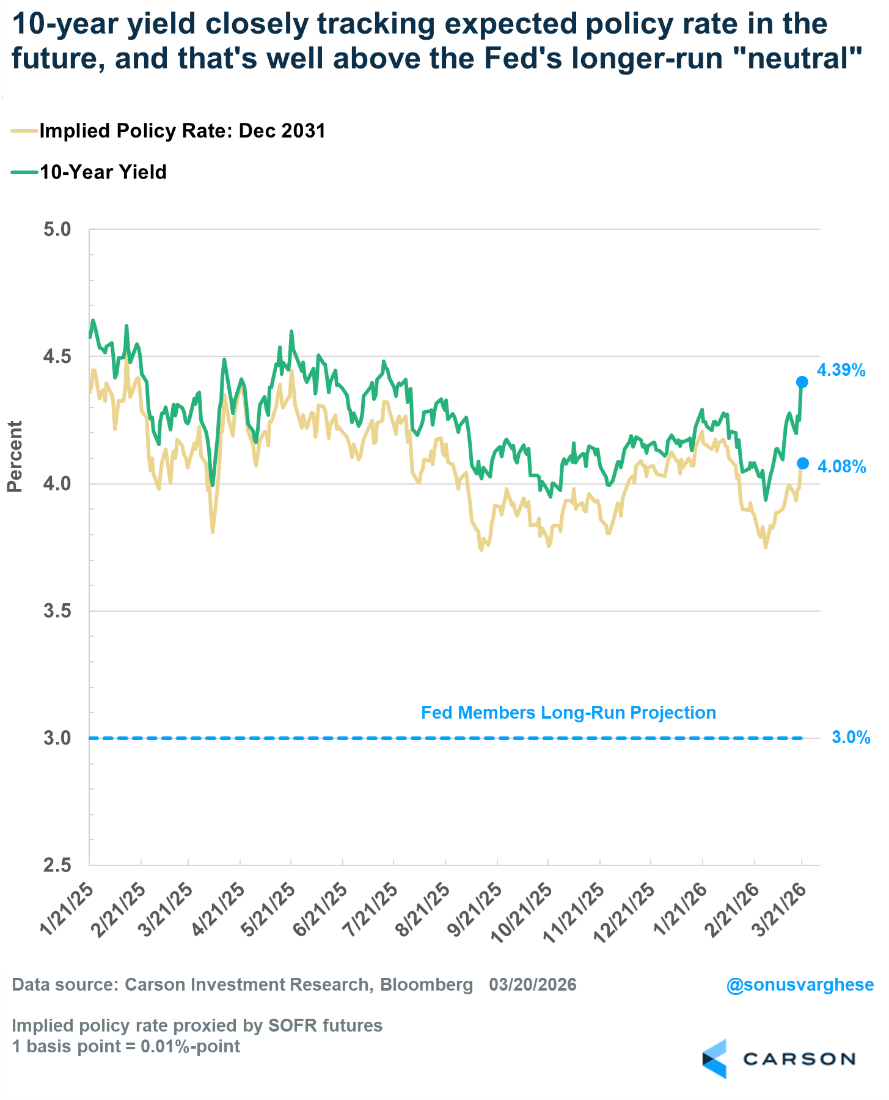

Long-run rate expectations have also shifted, which is what is driving long-term yields (like the 10-year) higher. The implied policy rate for 2031 has risen to 3.94% — well above the Fed’s own long-run neutral target of 3.0%. Markets expect inflation to remain a problem and rates to stay higher for longer.

What’s notable is that market expectations for future rates are well above the Fed’s own long-run projection of 3.0% — the neutral rate that’s neither stimulative nor restrictive. The 10-year yield closely tracks expected long-run policy rates, and both are pricing in a future in which inflation remains elevated.

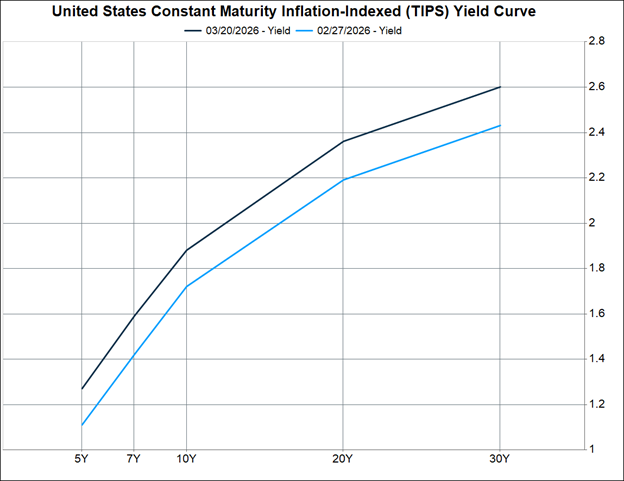

Meanwhile, real yields on Treasury Inflation-Protected Securities (TIPS) have also moved higher: the 5-year real yield is up 16 bps to 1.27%, the 10-year up 16 bps to 1.88%, and the 30-year up 17 bps to 2.60%. If investors were genuinely worried about a sharp growth slowdown, we’d expect real yields to fall. Instead, they’ve risen consistently with the view that the Fed may keep rates elevated to manage inflation rather than cutting to cushion growth.

Source: FactSet Research Systems

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Gold Doesn’t Like a Hawkish Fed

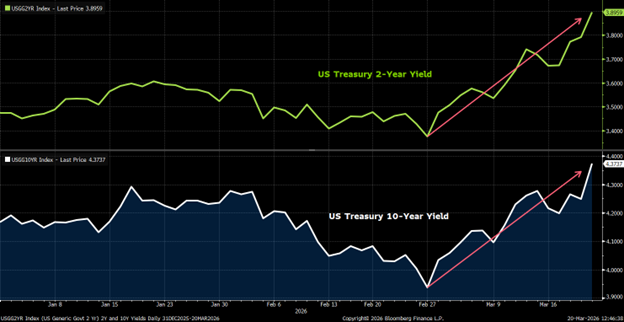

Gold has also disappointed during this stretch, and by a wider margin than many investors realize. The chart below compares the S&P 500 and gold since late February through March 20.

Since February 27, gold has fallen roughly 13.5%, nearly three times the S&P 500’s 4.8% decline over the same stretch. The metal still carried an impressive year-to-date gain heading into this period, but the recent drawdown is a useful reminder that gold is not a reliable short-term safe haven in all environments.

The key is gold’s relationship with real interest rates. Gold is expensive to store and generates no income. When real rates are low and falling, the opportunity cost of holding gold is minimal. But when real rates are rising — because the Fed is expected to keep policy tight to fight inflation — that cost rises, and gold loses its shine.

We’ve seen this dynamic before. In 2022, Jerome Powell’s hawkish pivot in mid-April sent gold down roughly 18% between April and September as near-term policy rate expectations surged from 1.8% to over 4.0% in just five months. Going further back, Paul Volcker’s aggressive tightening from July 1980 to June 1981 crushed gold by 35% as 1-year Treasury yields soared from ~8% to over 13%.

Two Paths for Gold From Here

Hawkish Fed: If the Fed surprises markets with aggressive rate hikes, as it did in 1980–82, gold faces further downside. Rising real yields significantly increase the opportunity cost of holding the metal.

Tolerant Fed: If the Fed opts to live with elevated inflation rather than hike aggressively, as in the 1970s, gold could be a major beneficiary. From 1971 to 1979, gold gained 1,268% as the Fed fell behind the inflation curve. The strategic case for gold remains intact; the near-term path depends entirely on Fed resolve.

The Bigger Picture

None of this means bonds and gold have lost their long-term strategic value. But in an inflationary, geopolitically charged environment, the typical playbook gets rewritten. As long as the Fed avoids the kind of aggressive tightening that would tip the economy into recession, nominal GDP should continue growing in the 5–6% range, an environment that, historically, has been reasonably supportive for equities even if uncomfortable in the short term.

Even in 2022, when stocks fell sharply, revenue growth held up because nominal GDP grew 7.9%. The pain came from valuation compression as the Fed hiked from 0.25% to 5.5%. The difference today is that the Fed is starting from a much higher rate (3.63%), and the magnitude of any potential hikes is likely to be far more modest.

Markets are navigating a genuinely unusual setup. Staying grounded in the data, rather than assumptions about how diversifiers “should” behave, is the right approach right now.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8835049.1. – 20MAR26A