The Chinese word for ‘crisis’ has two symbols. One is ‘danger,’ and the other is ‘opportunity.’

On Saturday, the US and Israel struck Iran in a large-scale attack that included the death of Iran’s Supreme Leader Ayatollah Ali Khamenei and other top leadership. There are more questions than answers right now, but in the near term, higher oil prices, higher gold prices, and some movement into bonds (and other defensive assets) seem likely. Our base case is that these effects will be relatively short-lived and likely largely a market memory in six months. There remains some risk that the conflict may expand and become more damaging, but below we discuss why we don’t think that’s the most likely outcome. Special thanks to Sonu Varghese, Chief Macro Strategist, and Barry Gilbert, VP, Asset Allocation Strategist, for doing most of the heavy lifting in this blog.

- Historically, what in the near term seems like a geopolitical crisis tends to be largely resolved from a market perspective over the ensuing six months, and where it’s not, it’s often because of an economic downturn that the geopolitical crisis didn’t cause.

- We believe the market has already been pricing in the possibility of a conflict for a month, which may limit the size of a further move and may cause a quicker rebound when the market sees a likely path to resolution.

- The initial market reaction to the actual conflict, based on overnight futures, has been measured, although oil markets made a substantial move higher.

- Despite purported goals, we don’t think the actions of the US or Iran signal that either believes the actual goal is regime change, even though the US has created conditions that make regime change more likely, though the odds remain low.

- If the US shows greater commitment to regime change, or if Iran believes the US is more serious, economic risks increase.

- Energy prices would likely be the main transmission mechanism for market risk, as they can have a meaningful impact on inflation and, through inflation, on interest rates.

- The US is much less vulnerable to temporary energy price spikes than in the 1970s because it is now a net oil exporter, and technology has made it easier to raise domestic production relatively quickly.

- Higher inflation uncertainty (which doesn’t necessarily mean higher inflation) has been a base case for us, and while we didn’t view geopolitical risk as the primary source of uncertainty, our thesis accounts for it. That’s part of why we have been underweight bonds, overweight in commodity exposure, and internationally diversified.

- The conflict does not change our base case of an S&P 500 Total Return of 12-15% in 2026, although we are still in a seasonally challenging period.

- Very big picture, the attack is likely to help stabilize the region, but two successful military actions (Venezuela and Iran) may lead President Trump to test the reach of US military power further.

Here’s a deeper dive on each point.

Historically, what in the near term seems like a geopolitical crisis tends to be largely resolved from a market perspective over the ensuing six months, and where it’s not, it’s often because of an economic downturn the geopolitical event didn’t cause.

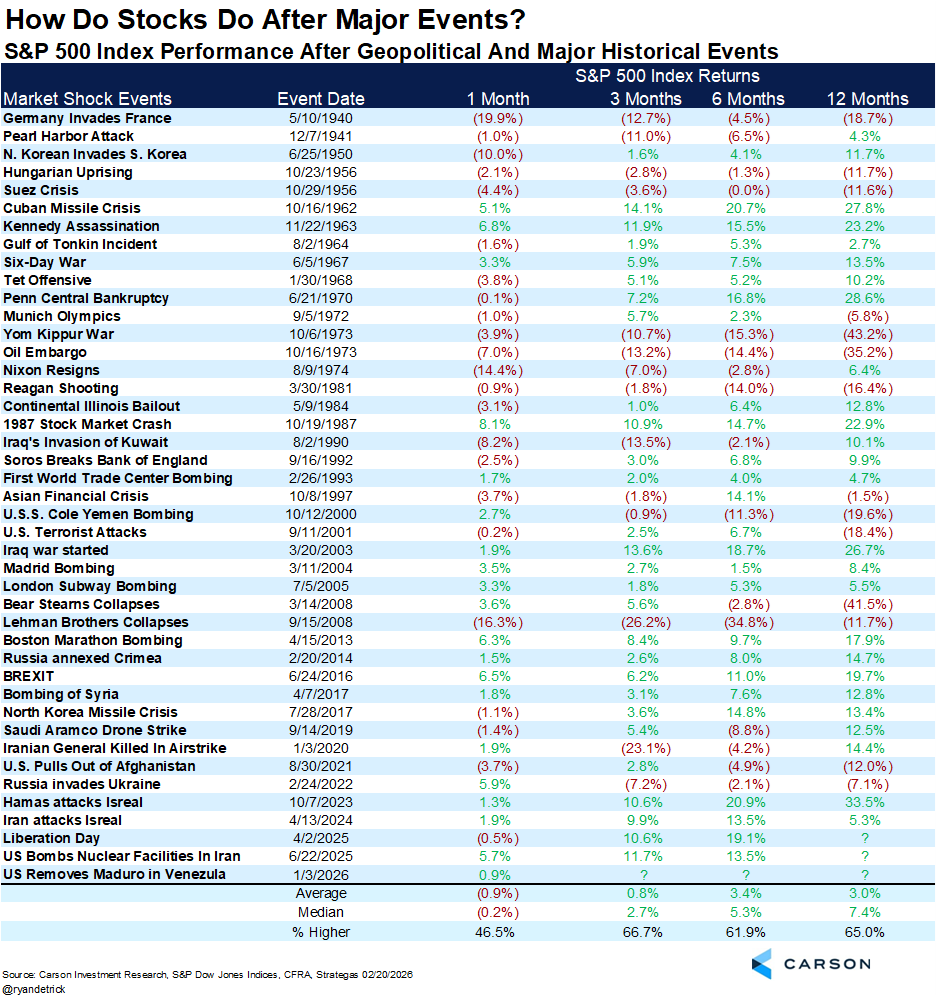

As we’ve shared many times, here’s a list of some of the largest geopolitical events in market history and how stocks did afterwards. Yes, near-term volatility and potential weakness are common, but as you go out, the returns are more positive—in fact, the S&P500 is up a median of more than 5% six months after the events below.

The average six months out runs a little lower, and while the median rises a year out, the average drops a little. But it’s important to understand why. Some of these events coincide with macroeconomic downturns, and the geopolitical events may not even contribute. And where the events do contribute, they’re often not strictly geopolitical (for example, Lehman Brothers collapsing). 1973 is an important exception, but it occurred in a context where US oil dependency on OPEC was far greater than it is today, and even then, economic weakness was already well established, increasing sensitivity to a geopolitical crisis.

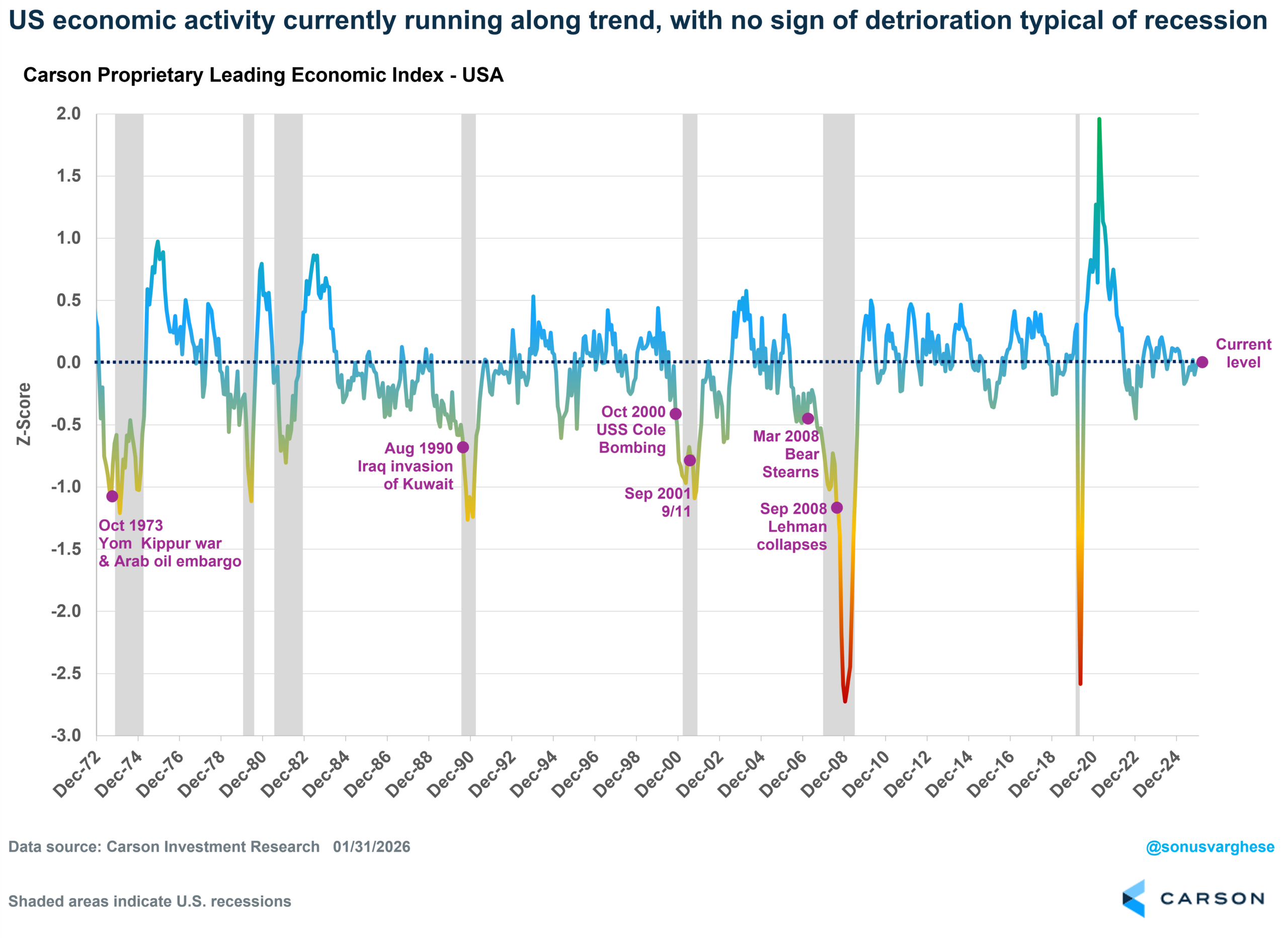

Here’s a look at some of these downturns mapped onto our own proprietary Leading Economic Index for the US going back to 1973. This index uses more timely data than GDP, including consumption, production, housing, and consumer and business sentiment data. We’ve marked several of the above events that saw a larger market downturn on the chart, and as you can see, economic activity was already running well below trend when they occurred. (A reading of zero signals growth near the long-term trend).

Right now, based on this index, we are experiencing near-trend growth, which mitigates some of the risk that we are set up for a protracted market downturn.

We believe the market has already been pricing in the possibility of a conflict for a month, which may limit the size of a further move and may cause a quicker rebound when the market sees a likely path to resolution.

The US began a noticeable force buildup in the Middle East in late January, with the arrival of the USS Abraham Lincoln carrier strike group. By mid-February, reports surfaced of a second carrier group being sent, which turned out to be the USS Gerald R. Ford strike group. That means markets have had time to begin pricing a possible conflict. But do the numbers back that up? We think they do.

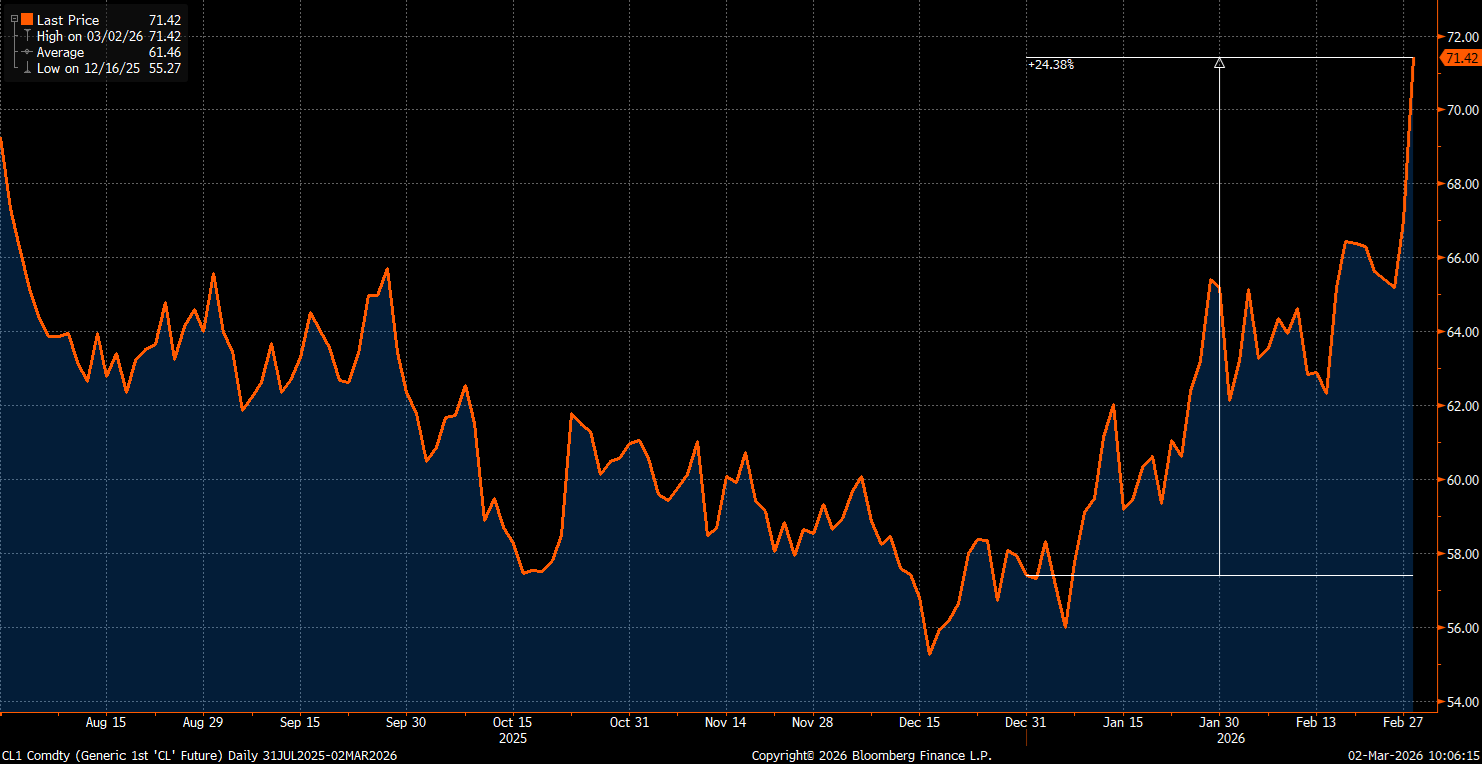

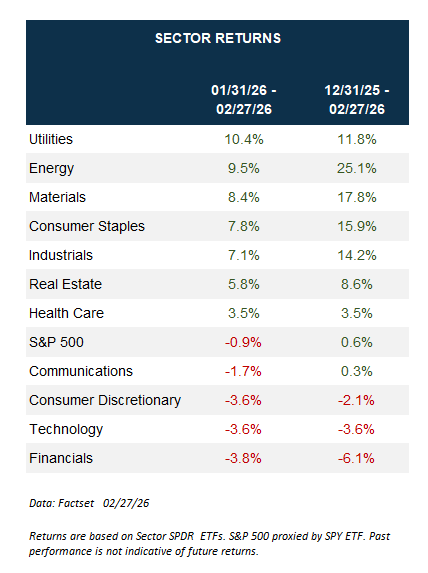

The top-performing sectors in the market year to date have been energy (+25.1%) and materials (+17.8%). Just in February, energy was up 9.5%, and materials were up 8.4%. Oil prices have already been rising since the start of the year: WTI crude prices are up 24% year to date, to $71/barrel, the highest since last August. While these trends partially predate the force buildup, anticipation of geopolitical events likely supported the existing trend.

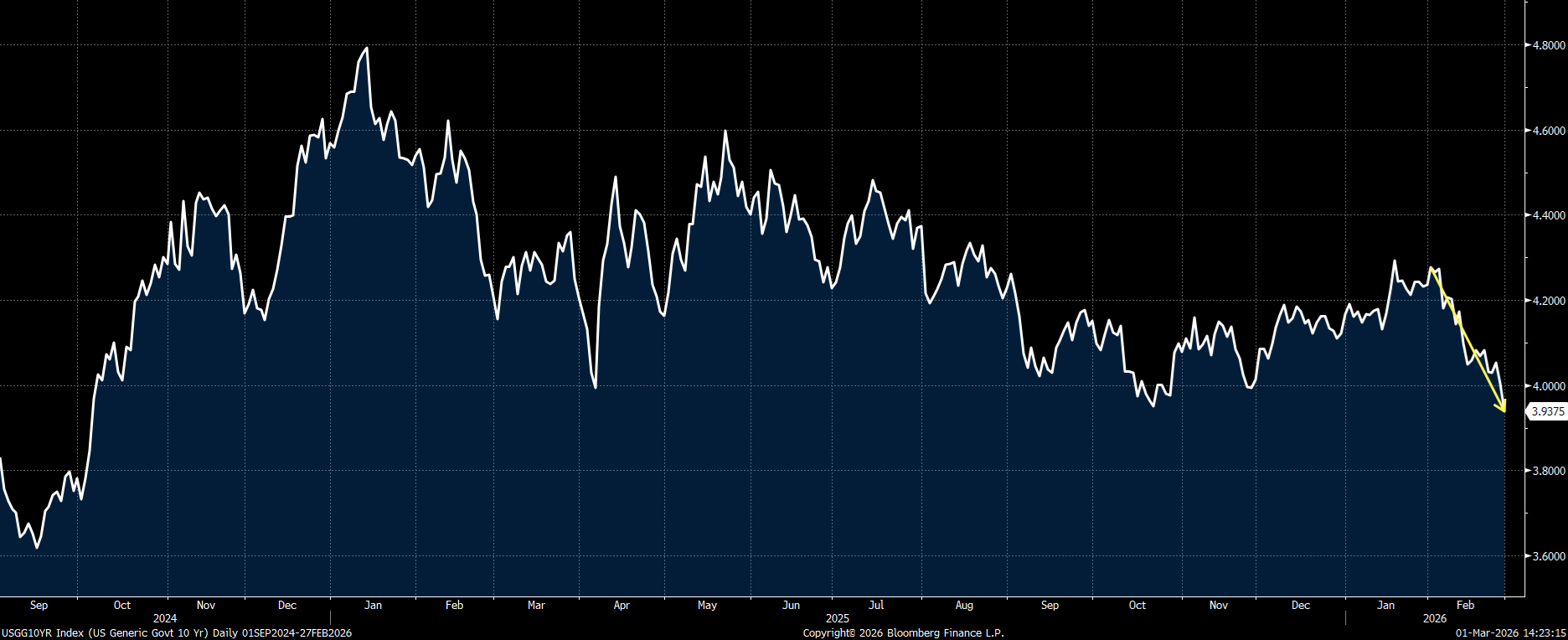

At the same time, bond yields have fallen, with the 10-year yield breaking below 4% on Friday for the first time since late October. The 10-year yield plunged 0.3%-points in February, a large move, ending the month at 3.94%. Lower yields signal investors expect slower growth and, sometimes, lower inflation, but that doesn’t make sense when the energy and materials sectors are also receiving support.

Contributing further to the picture, after energy and materials, the next-best-performing sector year to date is consumer staples (+15.9%). And just looking at February, utilities were the best-performing sector (+10.4%), while consumer staples gained 7.8%, a leadership that tends to happen when investors are in a risk-off mood. This also jives with a plunging 10-year yield, as investors often buy bonds to hedge against stock declines (though this strategy isn’t always effective).

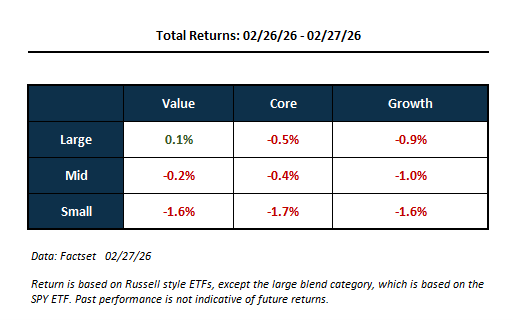

On Friday, small caps also fell 1.7%—another sign this was a risk-off move anticipating geopolitical uncertainty.

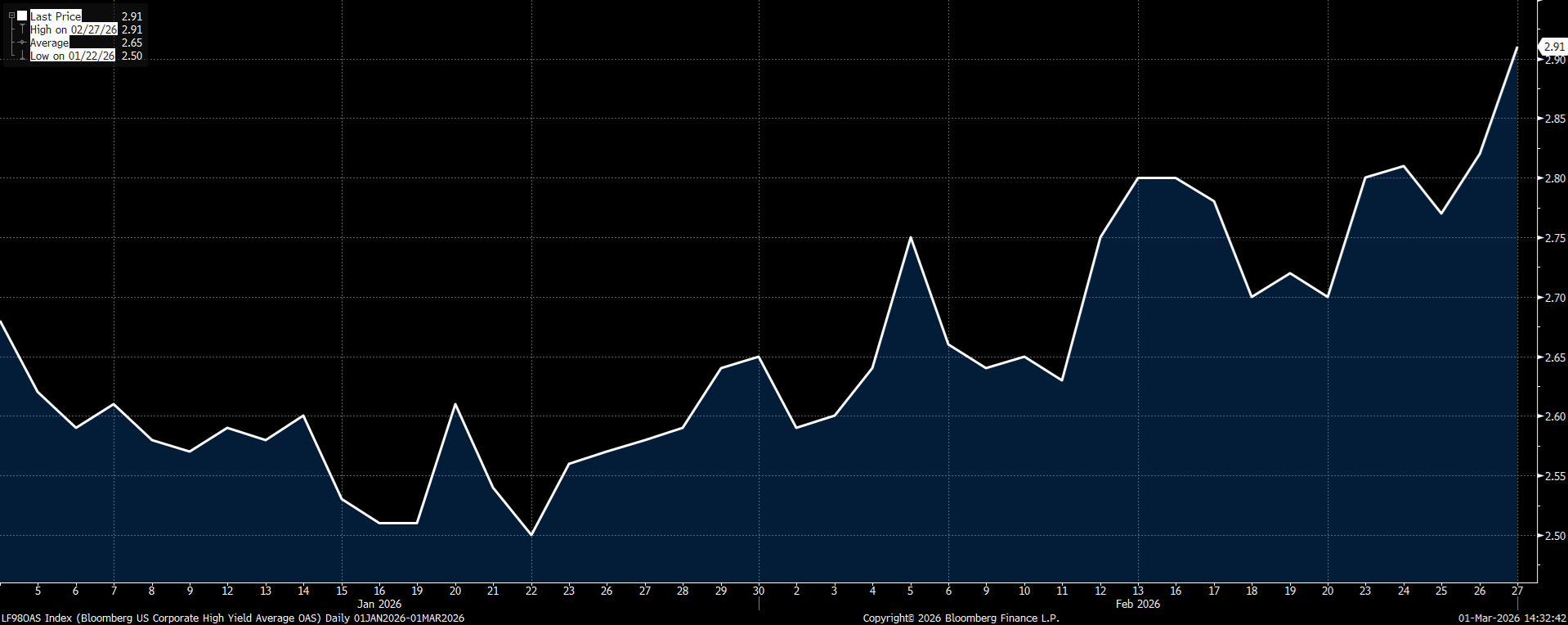

In addition, high-yield corporate bond credit spreads have widened, indicating investors are at least a little more worried about defaults. While spreads are still well below levels that would leave us worried about the economy, it is yet another risk-off move.

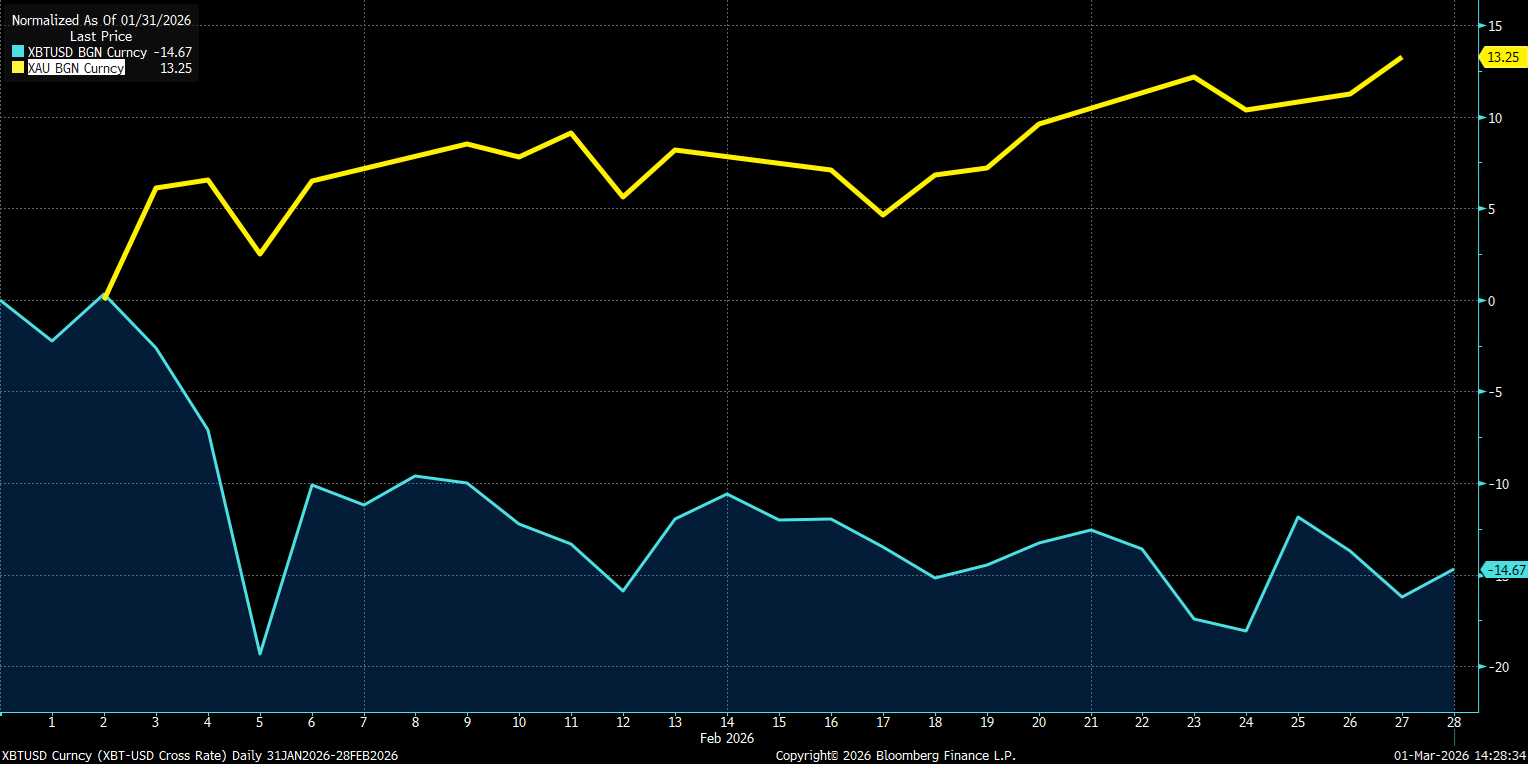

Add in that bitcoin, a risk proxy, fell almost 15% in February (blue line in the chart below), taking its year-to-date loss to -24.4%. Meanwhile, gold, a crisis hedge, rose 13%, taking its year-to-date gain to +21.9%.

Higher energy prices, coupled with general risk-off sentiment points to markets sensing a geopolitical crisis in the Middle East before the events of the weekend. With the conflict already partially priced in, there may be less downside risk from here, and the possibility of a stronger reversal if markets begin to expect a relatively quick resolution.

The initial market reaction to the actual conflict, based on overnight futures and Monday AM, has been measured, although oil markets made a substantial move.

We are writing this in real time, but based on futures markets and today’s opening, market participants are tilting risk off but taking the start of hostilities in stride. As of one hour into trading today, the S&P 500 is down less than half a percent. WTI oil futures were up close to 10% last night, but are up about 6% right now, and that’s where we would expect the initial reaction to be strongest. Gold futures are catching a bid, up more than 1%. The 10-year Treasury yield moved back above 4% as inflation risk, which would push rates higher, offset risk-off demand, which would push rates lower. The move in oil prices is a concern, but WTI futures still sit in the low $70s per barrel, a level that is not a meaningful economic threat yet.

Despite purported goals, we don’t think the actions of the US or Iran signal that either believes the actual goal is regime change, even if the US has created conditions under which regime change is more likely, although odds remain low.

From the US perspective, the first day went exceedingly well. Bombs were on target, and the Iranian regime was decapitated. But it looks like the US envisioned the conflict, or at least this stage, lasting just about 4-5 days before getting Iran back to the negotiating table.

In my opinion, for real regime change, you would need 1) a new leadership in the wings that will step into any vacuum, 2) US ground forces to provide security for a new government, and ensure they are able to step in immediately. Neither is true today. There’s no government-in-waiting amid a deeply divided opposition, nor is the US likely to send ground troops. There’s no sign of a popular uprising either within Iran, partly because Iran ruthlessly eliminated leaders of the protests that erupted around the New Year.

It seems the biggest goal for the Iranian regime is to stay in power. While nuclear capability may support that in the long run (to the detriment of global stability), in the near term, it’s only a secondary objective. That’s why we didn’t see Iran escalate the conflict when this happened last time. There were a few perfunctory retaliatory attacks, but things calmed down quickly.

However, if the US were serious about regime change, or Iran believed it was, that would change the calculus. That could make the Iranian regime the side that escalates more rapidly than the US (and Israel) and impose as much damage as they could. If they haven’t, the most likely reason is skepticism about the US commitment to follow through on regime change.

The fact that Iran’s former leader, Ayatollah Khameini, was taken out could create an even more volatile situation. But Khameini was 86, and it’s likely there’s been a succession plan in place for years, if not decades. And even if the clerics fall, they’re likely to be replaced by the hardline security forces in the Islamic Revolutionary Guard Corps (IRGC). For some countries, the military is considered a potential moderating force. That’s not a realistic prospect with IRGC leadership as an extension of the regime’s most repressive tendencies.

As for Iran’s response, Iran’s attack on other Gulf countries is a significant escalation, and something they’ve never done in the past. It pretty much halts economic activity in the region, much of which is trade, which can’t take place if airports and some ports are closed.

But so far, Iran hasn’t attacked the Gulf countries’ oil infrastructure, which lies in range of its missiles. That is an option as well, though likely a last resort because of their strategic value. And while the conflict has led to shipping traffic avoiding the Strait of Hormuz, Iran has not yet attacked shipping going through the Strait or created a physical barrier by mining it or other means.

A potential off-ramp for the Trump administration without creating actual regime change is to say that regime change has been achieved because Ayatollah Khamenei is dead. This would be similar to what happened in Venezuela, when the US took out Maduro but left the rest of his regime in power.

If the US shows greater commitment to regime change, or Iran believes the US is more serious, the likelihood of economic risks become greater.

Ultimately, this has more to do with Iran’s assessment of the US commitment to regime change and its ability to hang on than with US intentions. If regime change were a real threat, Iran has two ways to escalate: take more serious action to close the Strait of Hormuz or systematically use missiles and drones to attack oil infrastructure in the region.

The Straits of Hormuz sees about 19 million barrels flowing through it every day, about 20% of global supply. Any real disruption, or even a halt to shipping across the straits, will have a huge impact. (Note that this has a significant impact on Iran’s economy as well, which is part of why it’s a last resort.) There have already been reports that Iran is shutting down the Straits of Hormuz, but this has been more a consequence of a conflict that may be short-lived than a structural barrier (such as mines) or explicit military efforts. Even if Iran were to attempt the latter, the world’s most powerful navy has a strong presence in that same corridor to keep the Strait open.

As for targeting regional oil infrastructure, this is what happened when the Iraqis retreated from Kuwait in 1991—they set the oil fields on fire, and it took 8-9 months to put them all out. This is the scenario in which we’re likely to see oil surge above $100/barrel. But as with closing the Strait, such a move does potential damage to Iran as well and is likely a last resort.

It’s also not just about oil. Qatar is the world’s largest liquefied natural gas (LNG) supplier. Any attack may benefit US energy firms, but as the US exports more natural gas, US prices become more tied to global prices, and we could see utility bills surge in the US (on top of already elevated pressure from data centers).

For now, it’s significant that Iran has not taken these measures. Note that some of the effects on shipping don’t require direct intervention by Iran, but these mechanisms would likely only last as long as the conflict does. In fact, the most effective thing disrupting shipping in the area so far may be insurance companies in London saying they’re no longer willing to insure ships (and their contents) transporting goods to/from the Persian Gulf, which includes canceling policies and raising coverage prices. Insurance prices for ships travelling through the Gulf were about 0.25 per cent of the replacement cost of a vessel. They could now jump by as much as half. So for a $100 million vessel, that would increase insurance coverage for a voyage from $250,000 to $375,000.

Energy prices would likely be the main transmission mechanism for market risk, as they can have a meaningful impact on inflation and, through inflation, on interest rates.

Oil and energy prices are likely to rise in the immediate term, although they’ve already been rising in anticipation of the conflict. The first question is whether oil takes out the June 2025 high of $75/barrel, and if so, by how much. Oil at $90 becomes a big inflation problem, especially if it stays there for a while. Oil surging to $120-130 becomes a big problem for the global economy.

We will take a closer look at higher energy prices and the impact on tomorrow’s blog.

The US is much less vulnerable to temporary energy price spikes than in the 1970s because the US is now a net oil exporter, and technology has made it easier to raise production relatively quickly.

Oil prices will be interesting to watch, partly to gauge the “message of the market.” If oil stays below $75, the “message of the market” will be that 1) this is not a protracted conflict, 2) the Iranian regime stays in place.

We think it’s unlikely that oil prices (WTI) rise above $100 a barrel. Even if it hits that level, which is likely in the event of a complete shutdown of the Strait of Hormuz, it’s unlikely that prices are sustained above that level. For one thing, US shale production will ramp up once oil hits above $80/barrel (and stays there). This is a big difference between a Middle East crisis today and one in the 1970s. We could also see increased production in Canada and Latin America.

Also, several OPEC+ countries announced on March 1 that they will increase production to the tune of about 206,000 barrels per day (bpd). Note that these countries were already increasing production by about 137,000 bpd from Q4.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Market Takeaways

Our last three points (along with the first) are our primary market takeaways.

Higher inflation uncertainty (which doesn’t necessarily mean higher inflation) has been a base case for us, and while we didn’t view geopolitical risk as the primary source of uncertainty, our thesis accounts for it. That’s part of why we have been underweight bonds, overweight commodity exposure, and internationally diversified.

As discussed in our 2026 Outlook: Riding the Wave, inflationary growth is our base case for 2026. Inflation is typically the price of growth and a price worth paying if inflation is kept reasonably in check. The balance right now is delicate, as several economic forces (AI energy and chip demand) and Trump Administration policies (immigration, tariffs, and greater geopolitical uncertainty) can contribute to the risk. Even so, we think the positive impact of the growth outlook still outweighs the risks from inflation. A protracted conflict in the Middle East, however, accompanied by a genuine threat of regime change in Iran, could tip the balance. As a policy matter, that might still be the best outcome, but our job is to gauge the impact on markets, and that outcome would likely come with additional market and economic pain, not to mention military risk. But it may turn out that a significant increase in Iranian containment, with nuclear ambitions meaningfully undermined and any real negotiating power quashed, may be a reasonable second best.

The conflict does not change our base case of an S&P 500 Total Return of 12-15% in 2026, although we are still in a seasonally challenging period.

While the conflict increases the risk to our outlook, it’s not a large shift, and we still believe our base case is solidly in place. It may, however, require some patience. We are still in a seasonally challenging period, and the first month after the start of a geopolitical conflict often sees some additional market impact. But trying to time the turnaround is likely to do more harm than good.

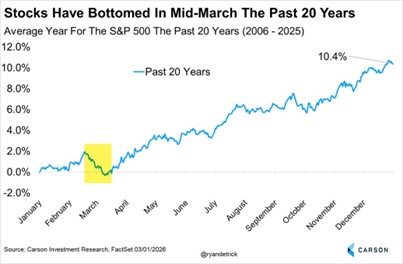

We noted many times that February is known for being one of the weakest months of the year (along with September), and looking at what the S&P 500 has done the past 20 years, more weakness into mid-March would be perfectly normal. No, history isn’t destiny, but it can be a guide.

At the same time, we are seeing many signs of extremely negative sentiment, which could be bullish from a contrarian point of view, especially if we get a quick resolution in Iran. Various sentiment polls are quite dour, flows out of technology have been extreme, and put/call ratios are showing the most worry since last April’s market crash. Add to that some of the market risks around the conflict already being priced in over the last month, which may help set up a stronger rebound.

Very big picture, we believe the attack is likely to help stabilize the region, but two successful military actions (Venezuela, Iran) may lead President Trump to test the reach of US military power further.

We’ll end with our thoughts—while our focus is on near-term market risk, Iran has been a constant source of potential long-term market risk as an ongoing threat to regional and global stability since the 1979 Islamic revolution. Some near-term market costs may actually yield longer-term benefits. And that’s not even to raise the issue of Iran being a brutally repressive dictatorship. The US should not be the world’s police force, but the attack on Iran is likely a place where national self-interest and global stability intersect. Even if a near-term market risk, the action could marginally improve the long-term outlook, and once you’re talking long term, even a marginal improvement is significant. If there’s a downside from a market perspective, it may be that the Trump administration becomes emboldened to further experiment with US military might as a policy tool. And while there is certainly scope for actions that further serve US self-interest, history provides countless examples of military overreach leading to consequential policy mistakes.

Thank you for taking the time to read our team’s perspective on this major geopolitical event. You have many places to get your macro and investment information, and we are honored that you chose to read what our team has to say. We won’t always be right, but we will always be honest, actionable, easy to understand, and always there for you.

For more content by Ryan Detrick, Chief Market Strategist click here.

8799359.1. – 3MAR26A