As we get ready to release our 2026 Outlook, I thought now would be a good time to revisit our 2025 Outlook. I recognize this is rare in our world, as it’s not often you see strategists revisit and reevaluate their calls. We don’t really think of ourselves as forecasters in the strict sense of the term, in that we’re not trying to predict economic variables or even market moves. But we manage several multi-asset class portfolios, and we’re always making choices within those portfolios, i.e., “predictions” as to the opportunity cost of overweighting or underweighting one asset class versus another. That’s another difference between a lot of the outlooks you see and ours — usually, the people writing these are not managing portfolios.

If you’ve followed us over the last three years, you know that we’ve had some strong views during that time, often in sharp contrast to the consensus. But our views are always translated to our portfolios, and it’s within that context that we evaluate what we got right and wrong. That’s how we try to keep ourselves honest in the process. (Of course, it’s reflected in portfolio performance too.)

With that, here’s the verdict on 11 calls we made in 2025.

One: Stocks would have an above-average year

Verdict: Correct

Our official prediction a year ago was for stocks (by which we mean the S&P 500) to gain 12–15% in 2025. These “predictions” are always a dicey proposition, but our view reflected our recommendation to be overweight stocks with the expectation that returns “exceed the typical return for the index (average of about 9% per year)”. Notably, we didn’t shift this expectation, or our “overweight stocks” call in our Midyear Outlook, despite all the volatility in April–May. The S&P 500 gained 17.9% in 2025, including dividends, which is as close as you can get in this business.

Two: Expect more volatility (relative to 2024) and a double-digit drawdown

Verdict: Correct

It seems clichéd to say “expect volatility in the stock market,” since the average year sees a drawdown of about 14% and volatility is the “toll” you pay to invest. We didn’t see a large drawdown in 2024, and we wrote a year ago that 2025 could be different, with a double-digit drawdown earlier in the year. This played out, although we certainly didn’t expect Liberation Day and the near-bear market that resulted. The S&P 500 fell 19% from February 19th, 2025, through April 8th. But it also highlighted the policy whipsaw around tariffs, which we discussed in our 2025 Outlook.

Three: Tariffs are a threat that could upend optimism

Verdict: Correct

Boy did this play out. A year ago, we wrote that excessive tariffs were a looming threat that could upend early-year optimism around the new administration. We pointed out that while Trump discussed implementing huge tariffs (especially on Chinese goods), the market reaction would likely be quite negative. This is straight from our 2025 Outlook:

“For better or worse, President Trump likely sees the stock market as a report card on his performance, and so a negative market reaction may prompt him to temper some of his proposals. Expect to see market volatility around tariff announcements (or rumors).”

As it turns out, the administration proposed massive tariffs on Liberation Day, but quickly pulled those back amid market pushback, both from the stock and bond markets.

Still, it’s one thing to predict drawdowns and market volatility, and threats from tariffs, but what I’m proud of is how we positioned portfolios with this in mind. As I mentioned above, we didn’t change our full-year outlook despite the tariff chaos, remaining overweight stocks. (Our chief market strategist, Ryan Detrick, was in fact on TV on April 9th, saying the lows could be in.)

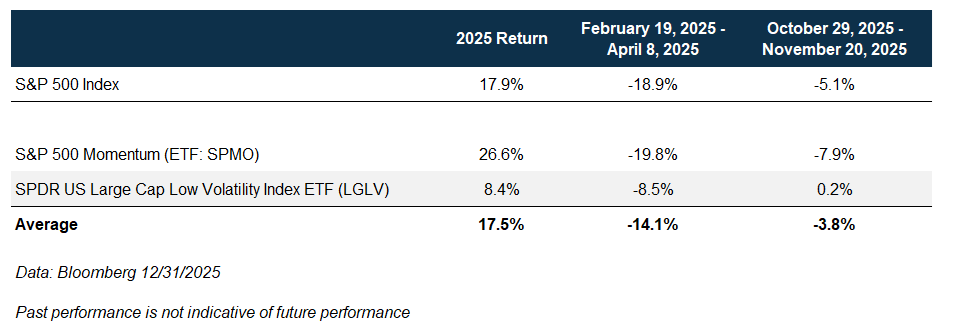

However, we also wrote about implementing a momentum + low volatility factor barbell to help play offense and defense at the same time. As you can see in the table below, the combination (which has historically outperformed the broad market) almost matched the S&P 500 return in 2025 while falling less during the February – April period, and even in November when the S&P 500 fell 5%. A side note here is that ETF/methodology selection matters too—you have to be careful about the specific flavor of momentum and low volatility to use, which is something else we believe our team is really good at.

Four: Stocks would be powered by earnings growth, including margin expansion

Verdict: Correct

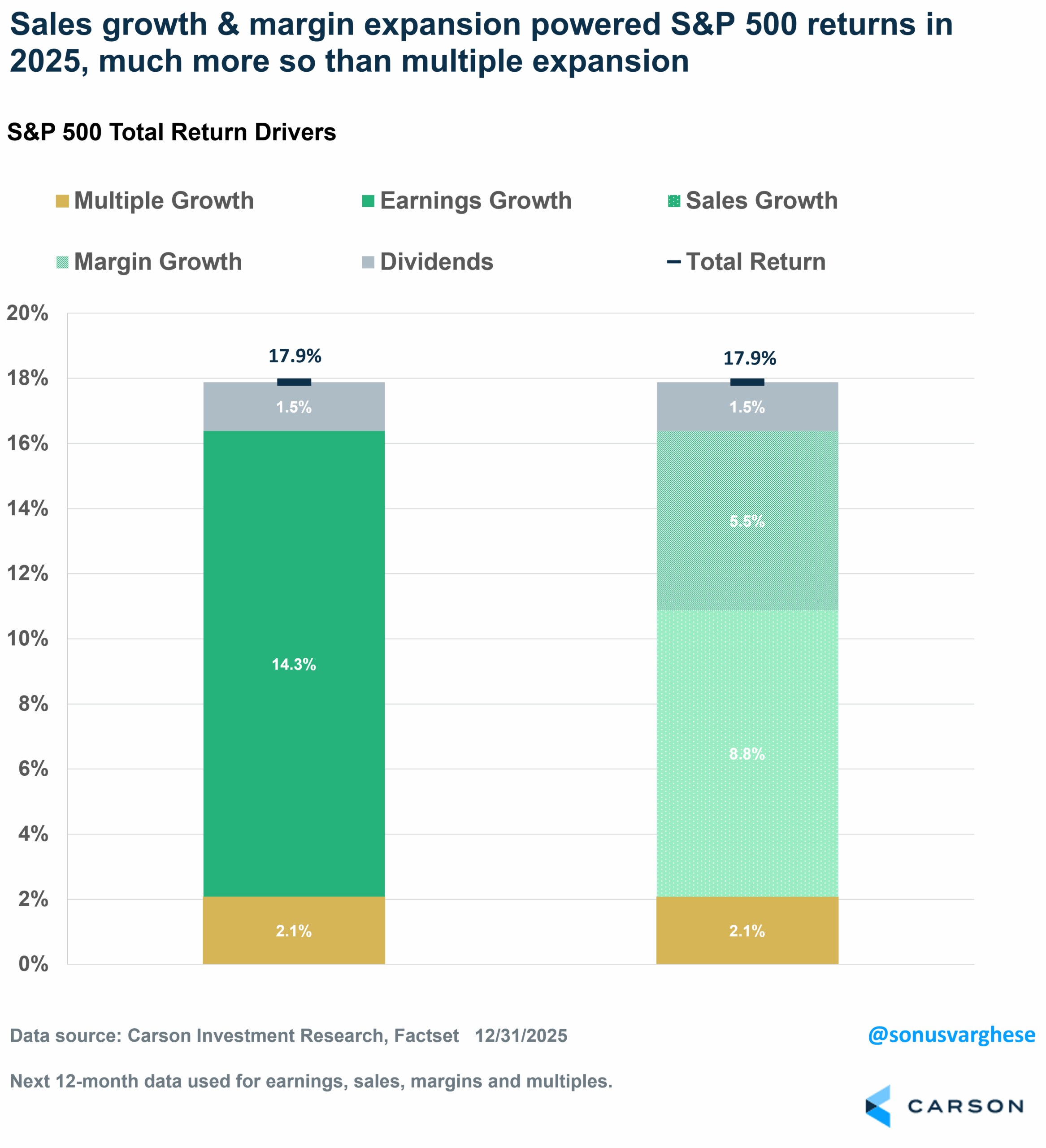

In our 2025 Outlook, we wrote that continued stock market gains would be driven by profit growth, on the back of sales growth and margin expansion. Sales growth is tied to nominal GDP growth, which didn’t skip a beat in 2025, clocking in around 5-6% annualized through Q3 (partly due to elevated inflation). We also pointed out that an underrated story is corporate America’s “operating leverage,” which allows firms to expand margins as sales grow. This played out in 2025, as firms grew sales and expanded margins amid significant policy headwinds and economic uncertainty. The message was don’t underestimate corporate America, and it still is.

You can see how the S&P 500’s 17.9% return in 2025 came mostly from profit growth, powered by sales growth and margin expansion, rather than multiple expansion.

Five: Continued economic expansion

Verdict: Correct

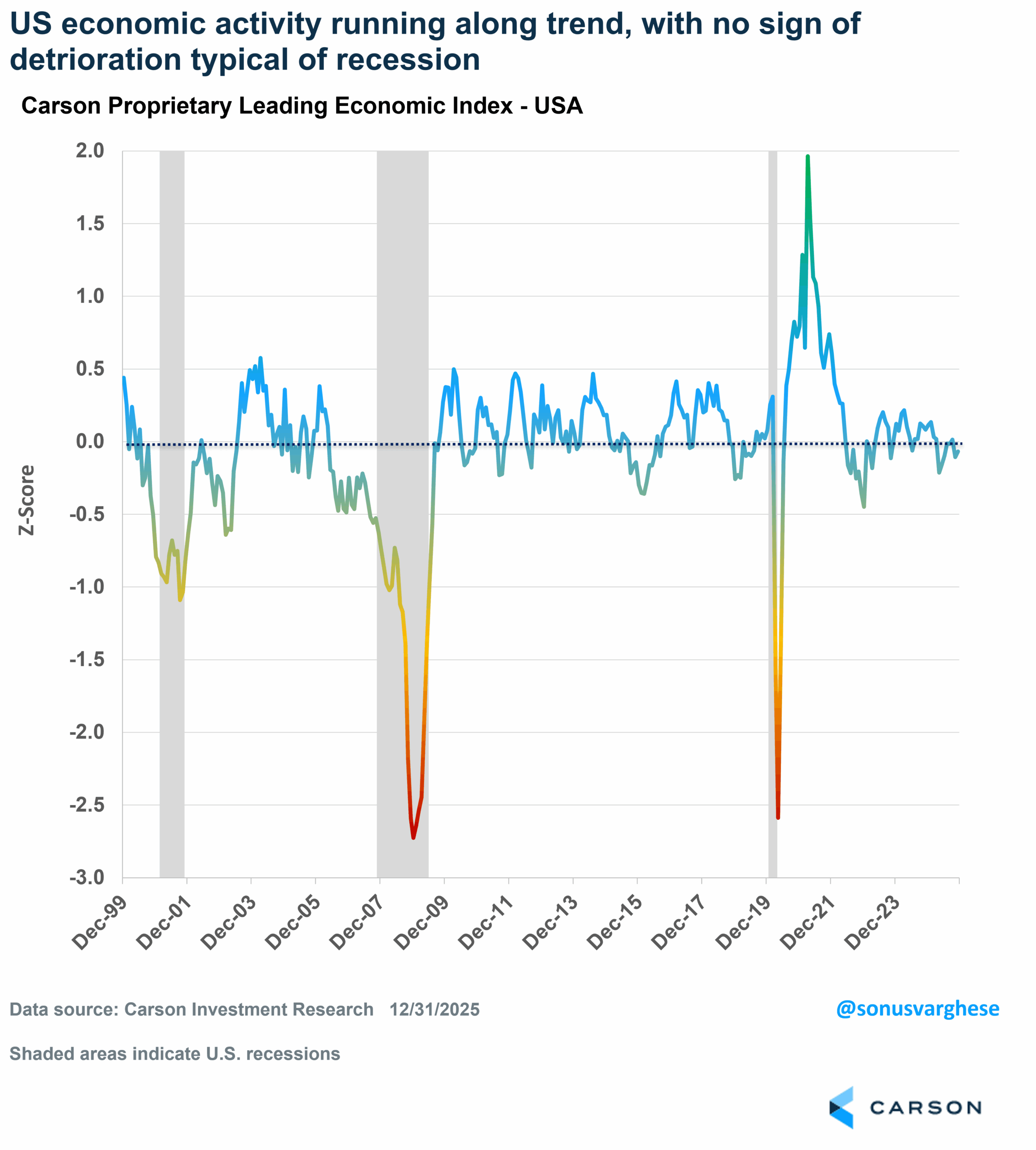

This didn’t seem like a differentiating “call” at the start of last year, since optimism was riding high and we were one of many calling for continued economic growth (unlike in 2023 and 2024, when our call for economic expansion was relatively more contrarian). But it became a contrarian outlook after Liberation Day, when there were many recession calls. One grounding factor for us is our proprietary leading economic index (LEI) for the US (we populate a similar measure for 28 other countries around the world). It had served us well in 2023 and 2024 by suggesting there was no recession imminent, and again in 2025 when we just didn’t see signs of economic deterioration typical of a recession (in contrast to another popular LEI). Our index has both official and private data, which also helped during the data blackout period amid the government shutdown.

Our US LEI remains in a fairly solid place as we move into 2026, suggesting the economy is growing along trend, represented by a score near 0.

Six: A Dovish Fed

Verdict: Correct

We wrote that the benign inflation outlook would allow the Fed to focus more on the employment side of its mandate. Inflation remained elevated in 2025, with no progress due to tariff-affected inflation in core goods and stubborn core services inflation. Still, lower oil prices and shelter disinflation meant we didn’t see a big inflation surge despite the challenges. The tariff issue led to a delay in rate cuts, but a rising unemployment rate meant we saw rate cuts late in the year, as the Fed looked to avoid further cooling in the labor market.

We expected 50 basis points of cuts in 2025, similar to market pricing a year ago, and the Fed ended up cutting 75 basis points, taking the policy rates to the 3.50–3.75% range. I’m still going to rate the call as correct, as we expected a dovish Fed. In the end, that’s what we got (and positioned for as I’ll discuss below).

Seven: Bonds have a good year

Verdict: Correct

We expected a 4–7% return for bonds, thanks to high starting yields and a potential boost from rate cuts. The US aggregate bond index gained 7.3% in 2025, as interest rates fell. From a portfolio perspective, we targeted interest rate sensitivity that was slightly higher than the benchmark US Aggregate Bond Index (and underweight cash)—a call that worked out in 2025.

Eight: A Shift to a large-cap overweight, relative to mid- and small-cap stocks

Verdict: Mixed

We started 2025 with an overweight to mid and small-cap stocks but pivoted to a large-cap overweight early in the year (we discussed this in our Mid-Year Outlook). Small caps did outperform large-cap stocks in the back half of the year, but mid-caps continued to lag large caps, which is why I’m going to rate this call mixed.

Nine: US Overweight Before an Early Year Pivot

Verdict: Wrong

We kicked off 2025 with an underweight to international equities, which by itself would be reason enough to rate this “forecast” as wrong. But the facts on the ground shifted in Q1, with a significant fiscal policy shift in Germany, and we moved to a neutral weight for international stocks early in the year. (I wrote about this at the time—another reason to follow our blogs, in addition to bi-annual outlooks.) It highlights that we’re ready to pivot when ground realities change. While this pivot worked out, we did maintain an overweight to developed markets relative to emerging markets, which was not correct in hindsight. So I’ll stick with the “wrong” verdict.

Ten: Diversifying diversifiers

Verdict: Correct

In addition to being positive on bonds in 2025, we also “diversified diversifiers,” with allocations to gold and managed futures. Gold had an outstanding year, gaining 65%. Managed futures had a very good year—despite the pullback in oil prices, commodities gained in 2025. But the key was implementation within the portfolio, as I’ll discuss below.

Eleven: Capital efficiency in portfolios

Verdict: Correct

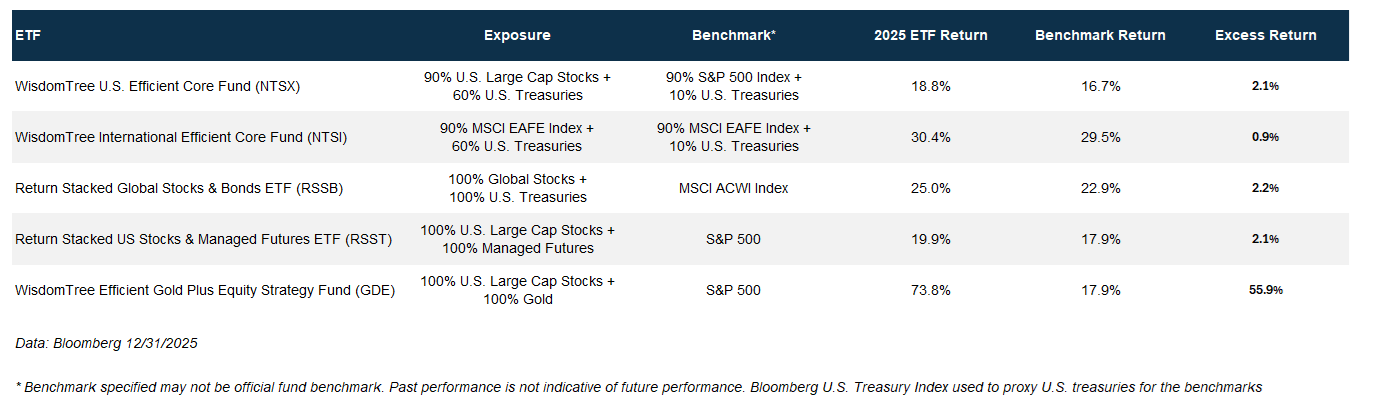

With our overweight in stocks, it can be difficult to find “space” in the portfolio for all our “diversifiers” (including bonds, gold, and managed futures). This is where we’ve been ahead of the curve (in terms of managing model portfolios in our industry) by creating capital efficiency in portfolios by using leverage specifically for diversification. I wrote about this in an Outlook-related blog a year ago. Leverage is usually a dirty word in our business, mostly because it’s often used to double down on the same or similar bets (for example, investing $1 in a stock, and borrowing $1 more to invest in the same stock), and that can turn ugly when there’s volatility. In contrast, for capital efficiency, the extra dollar that is borrowed is invested in a typically low correlation asset (like bonds, gold, or managed futures). We use exchange-traded products (ETFs) like WisdomTree’s Efficient Core portfolios or Newfound/Resolve’s return stacked portfolios (full disclosure: we have been using these funds for years now), which helped us find “space” in our portfolios to diversify diversifiers, and even add alpha in 2025, since all the diversifiers did better than cash (and fees) as shown in the table below. Note that the benchmarks we use to evaluate these funds may not be the official fund benchmarks. Rather, we look at what we use to “fund” these positions in our portfolios to create capital efficiency.

Pulling it all together

Here’s the final count:

- 9 Correct

- 1 Mixed

- 1 Wrong

Once again, I want to stress that it’s not about the calls, but how they translate to the portfolios we manage. From that perspective, the verdict is even better than what I summarized above and resulted in the best year since inception for our tactical models. We obviously did get a few calls wrong, but that’s also where portfolio construction matters, along with risk management. An important point here is that we do have broadly diversified, risk-based benchmarks for all our portfolios. As my colleague Barry Gilbert wrote, selecting a benchmark is not a trivial affair. It serves as our effective starting point for portfolio construction, but it’s also the neutral point we’re comfortable sitting at when uncertainty is high, and we don’t see opportunities to add differentiated value.

But that’s 2025. Keep an eye out for our 2026 Outlook, which will be released soon!

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

8690743.1. – 6JAN26A