On the face of it, headline fourth quarter (Q4) GDP growth disappointed. The economy grew at an annualized pace of 1.4%, after adjusting for inflation (“real” GDP growth), whereas economists were expecting double that number. A big driver of the underwhelming number was a big pullback in federal government spending, which pulled real GDP growth down by 1.2%-points (or 120 basis points, bps). Nondefense spending collapsed at an annualized pace of 24% while defense spending fell almost 11% (these are “real”, i.e., inflation-adjusted). This was entirely due to the October-November shutdown.

Typically, the most volatile parts of GDP are inventories and net exports – these are what resulted in big swings in GDP growth in 2025. This is why I like to focus on “final demand”, i.e., the combo of:

- Household spending

- Business investment (nonresidential and residential)

- Government spending (federal and state/local)

The problem is that in Q4, real final demand collapsed to just 1.1%. But as I pointed out above, that was largely because real federal spending collapsed amid the shutdown. That should reverse in Q1 2026. Though be wary of reading too much into that, as it’ll just be a rebound from Q4.

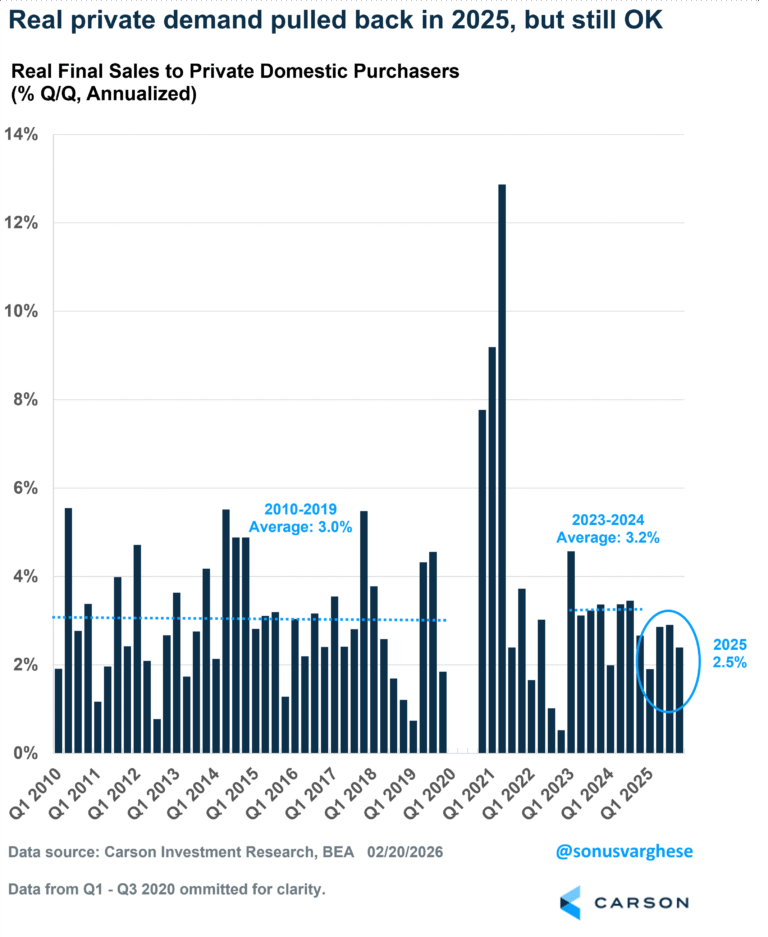

Private final demand, i.e., household consumption and business investment, was much better, rising at a 2.4% annualized pace.

Over the full year, real GDP growth rose 2.2%, while final private demand grew at a faster pace of 2.5%. That’s slower than what we saw across 2023-2024 (+3.2%), and even the 2010-2019 trend (+3.0%), but not by much. All said and done, private demand clocking in at 2.5% growth in 2025 is pretty good considering all the economic uncertainty raised by tariffs post-Liberation Day.

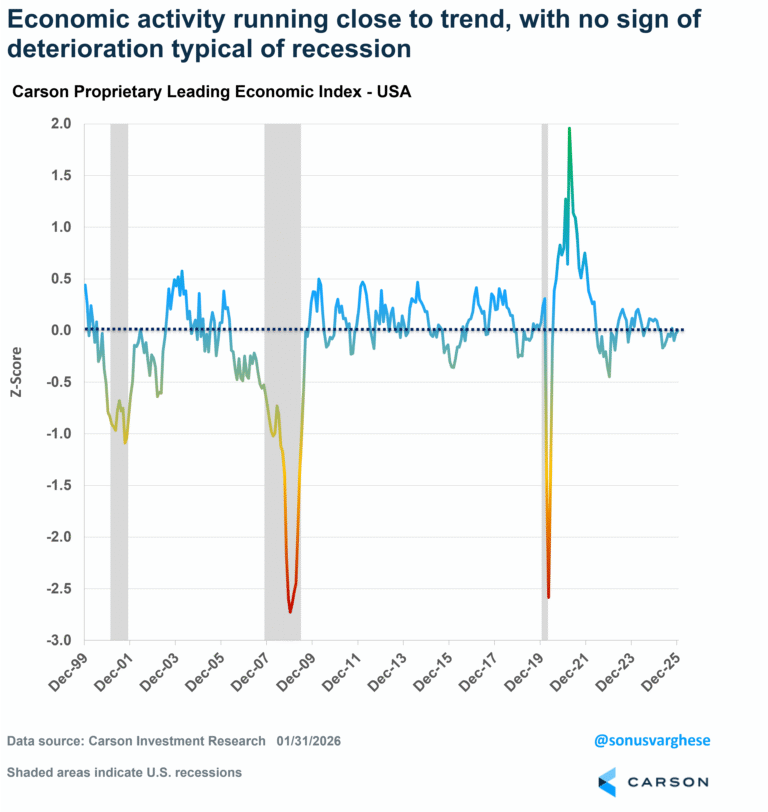

Note that our own proprietary leading economic index (LEI) for the US consistently told us that the economy was fine in 2025. Growth was running only slightly below trend across most of the year and has recently caught up to trend after a relatively weaker summer (in the aftermath of Liberation Day). Though even the summer weakness wasn’t significant. All this to say, the GDP numbers aren’t really a surprise to us.

It’s interesting to look at what drove private demand, and as it turns out, a lot of it was AI.

AI: A Big Wave

AI continues to have a big impact on the GDP data, which is something we discussed in our 2026 Outlook. When I say “impact, I’m referring to investment spending related to AI, rather than the adoption and integration of AI through the economy and boosting productivity (we’re yet to see that really, and probably won’t get details on that until several years from now).

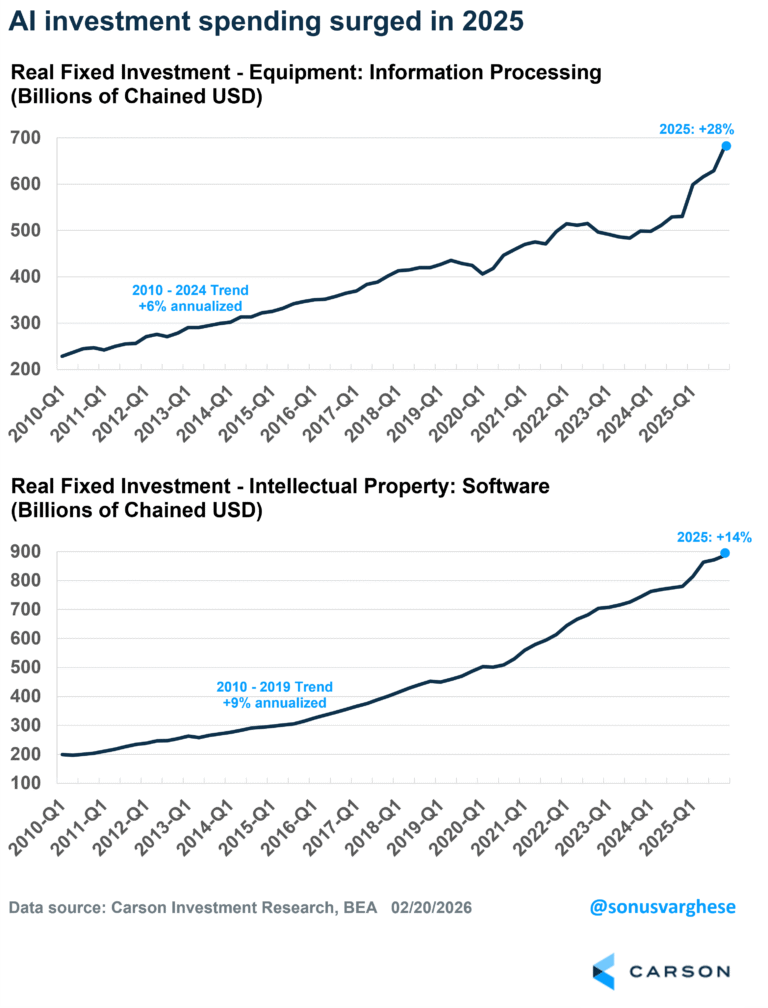

Investment spending on AI absolutely surged in 2025, on both the hardware and software sides. In fact, momentum picked up in Q4.

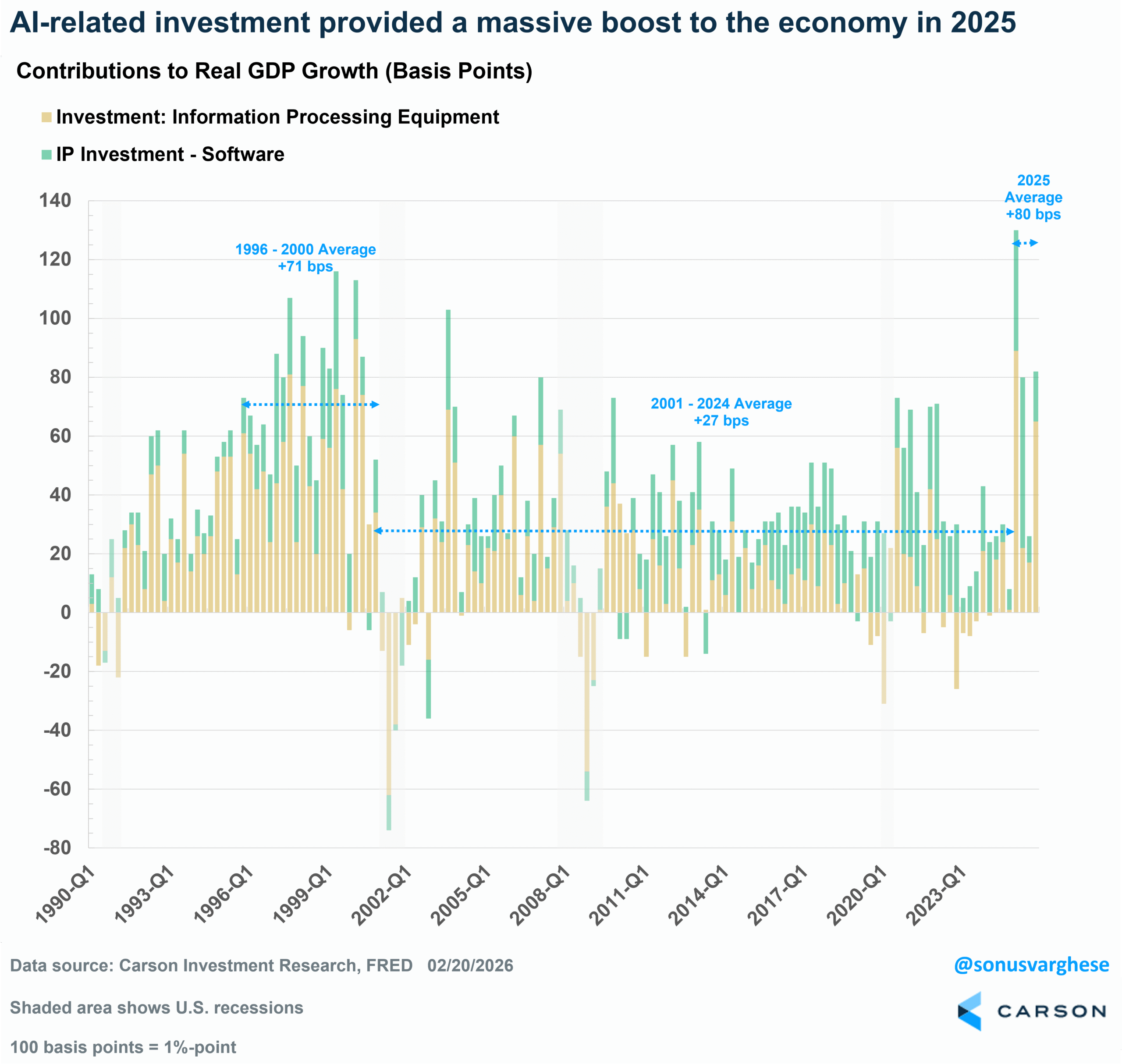

On the hardware side, investment spending on IT equipment jumped by 28% in 2025 – for comparison, the 2010-2024 annual pace was just 6%. Within IT, spending on computers and peripherals grew by a whopping 72% last year.

On the software side, investment spending clocked in at 14% year-over-year in 2025. The 2010-2024 annual pace was 9%.

These numbers are simply massive, and keep in mind that these are all adjusted for inflation. AI-related investment made a huge contribution to GDP growth in 2025. Across the four quarters, real GDP growth averaged 2.2%, of which

- AI-related hardware (IT equipment) and software spending contributed 80 bps per quarter, i.e., about 36% of real GDP growth.

- For perspective, consumption contributed an average of 151 bps per quarter in 2025. Keep in mind that consumption makes up 68% of the economy, while AI-related investment makes up just over 4% of GDP (it grew from 4.1% in 2024 to 4.5% in 2025)

- From 2001-2024, IT equipment and software spending contributed on average 27 bps per quarter

- Even during the internet boom (1996-2000), it contributed an average of 71 bps per quarter to real GDP growth

One thing I do want to note here is that a lot of this equipment is imported (these are all exempted from the post-Liberation Day tariffs), and so it doesn’t directly “contribute” to GDP in a strict sense – only goods produced domestically contribute to GDP. Still, it gives you a sense of the massive demand for AI-related equipment.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

This Is Good For Profit Growth

As we discussed in our Outlook, private-sector investment is a driver of corporate profit growth. Since profits are the main driver for stock prices, the key question is whether this level of investment spending will continue. The short answer seems to be yes, and it looks like early innings on that front.

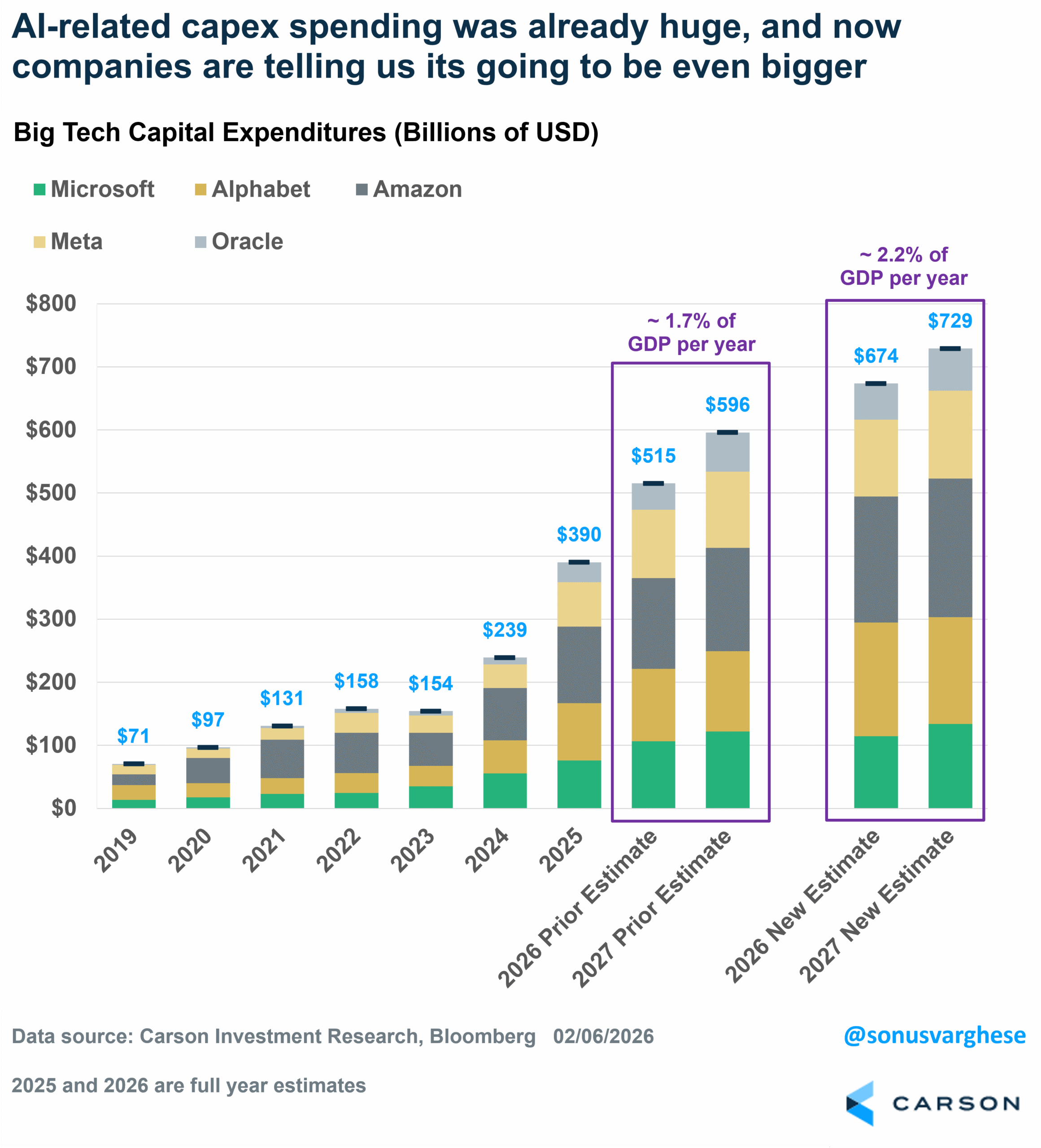

AI-related capital expenditures (“capex”) are being driven by large tech companies, especially those that provide large-scale cloud compute capacity and operate hyperscale-level data centers (Microsoft, Alphabet, Amazon, Meta, Oracle). I wrote about this in a recent blog. When we wrote our 2026 Outlook, we estimated that these firms would spend a total of $515B on capex in 2026, up from almost $400B in 2025. That amounts to about 1.6% of GDP (which’s huge, especially since it’s just in one year). However, the most recent post-earnings updates take the 2026 capex estimate to a whopping $674B, which is about 2.2% of GDP (2027 is expected to be similar) – that is over 4x the level of capex in 2023 (0.5% of GDP) and 7x the size of where it was in 2019 (0.3%).

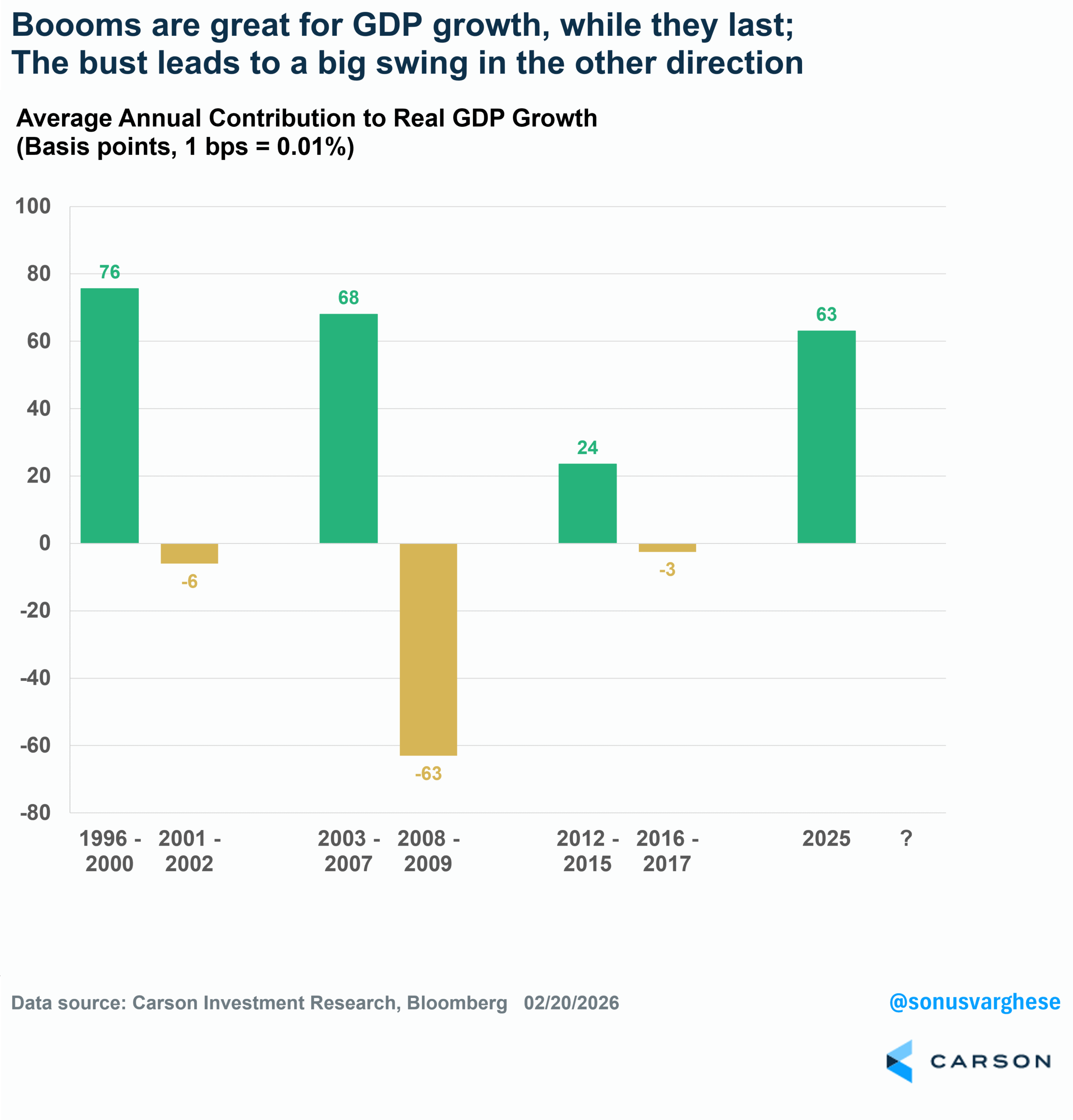

The current boom has led investors to draw parallels with other historical periods in which private firms made massive capital outlays to build the infrastructure for transformative technologies—railroads in the 1870s and the internet in the late 1990s. Relative to GDP, the current AI capex boom is already larger than the peak of the internet boom, but it’s still below the peak of the railroad buildout.

You don’t have to be a student of history to know what happened with the railroad and internet booms. Railroad stocks rose about 50% before collapsing. Telecom stocks rose 400% in the late 1990s before crashing. The internet boom is not the only economic boom we’ve seen over the last few decades. In fact, just after the internet boom/crash, we got the housing boom from 2003-07 (which was also a financial sector boom, including areas like real estate and insurance). Then we also got a mini-energy boom amid the shale revolution from 2012-15.

The dynamics are similar across these booms. Historically speaking, the promise of new technology pushes firms to make massive investments. Investors like that, and stock prices soar, which in turn facilitates even more investment. But ultimately, demand fails to keep up, and there’s excess supply, although that ultimately benefited society, whether it was railroads, high-speed internet that allowed us to connect as never before (and stream cat videos), new housing to meet the demand of the next generation, or cheap oil. Overcapacity leads to lower stock prices and lower valuations, and investment spending reverses.

Economic growth then takes a hit as the boom leads to a bust. It’s not like any of these areas—tech in the late 1990s, housing/finance in the mid-2000s, energy in the 2010s—were large parts of GDP. But when they were booming, GDP growth benefited. But the flipside was a sharp swing in the other direction when the booms ended.

Bigger picture, we are seemingly in a capex cycle with some strong parallels to those in the past, but we believe the length of the cycle (only a few years old), technology acceleration, and low current debt levels suggest we’re not in the latter part of the cycle. As we wrote in our Outlook, we don’t think the negative part of the cycle is a 2026 story, or even necessarily a 2027 one. For now, we believe we can ride the AI boom, but don’t believe it’s time to chase the AI theme with concentrated positioning—better to tilt in that direction for participation within a broadly diversified portfolio.

For more content by Sonu Varghese, Chief Macro Strategist click here.

8788776.1. – 24FEB26A