By Michael Barczak, VP, Investment Due Diligence

Recent guidance from the U.S. Department of Labor has once again brought alternative investments to the forefront of the defined contribution conversation. Headlines suggest a meaningful shift—greater access to private equity, private credit, real assets, and even crypto within 401(k) plans.

Our team wrote about this topic a handful of times in 2025 to address President Trump’s executive order on alternative investments in 401(k)s and to discuss the lineup construction methodology questions that alternative asset classes pose to advisors and plan sponsors.

But as with prior developments in this space, the more important question is not whether these investments can be added. It is whether they should be.

This distinction is critical.

While alternatives have never been explicitly prohibited under the Employee Retirement Income Security Act of 1974, ambiguity around fiduciary expectations—combined with real litigation risk—has historically kept plan sponsors on the sidelines. The latest guidance does not change the fiduciary standard. It simply clarifies the process for evaluating these investments.

In that sense, this is not a green light. It is a continuation of the same conversation—now with a more defined framework.

Why This Conversation Is Reemerging

The renewed push toward alternatives reflects broader shifts in capital markets. Private companies now represent a larger share of the investment opportunity set, and firms are staying private longer, meaning a greater portion of growth occurs outside of public markets.

At the same time, the defined contribution system—now measured in the trillions—represents a significant opportunity for asset managers seeking new distribution channels. Product development has accelerated accordingly, with structures designed to bring private assets into vehicles compatible with retirement plans.

This has naturally led to increased interest from plan sponsors and advisors. However, interest alone does not resolve the fundamental challenges associated with incorporating these asset classes into a plan lineup.

The Six Fiduciary Factors: A Framework, Not a Justification

Recent guidance highlights several key areas fiduciaries must evaluate when considering alternatives. These factors should not be viewed as a checklist for supporting inclusion, but rather as a framework for determining whether inclusion is appropriate at all.

- Liquidity and Redemption Alignment

Defined contribution plans are built around daily liquidity. Many alternative investments are not.

Private market strategies often involve lockups, redemption limits, or delayed liquidity. While newer structures attempt to bridge this gap, the underlying assets remain inherently less liquid. This creates a structural tension that must be addressed before any allocation is considered.

- Valuation and Transparency

Public market investments benefit from continuous pricing and robust disclosure requirements. Alternatives do not.

Valuations may be periodic, model-driven, or subject to estimation. Data is often less transparent, less frequent, and harder to benchmark. This creates challenges not only for monitoring, but also for aligning these investments with a plan’s Investment Policy Statement.

- Fees and Cost Structure

Cost remains one of the most tangible hurdles.

Alternative investments often incorporate layered fee structures, including management fees, performance incentives, and other embedded costs. Even in newer “evergreen” structures, total expenses are typically higher than those of traditional public market options.

Under ERISA, fees must be reasonable relative to the benefit provided. That burden of proof is materially higher than for low-cost index-based exposures.

- Diversification Benefits

The case for alternatives is often framed around diversification and access to new sources of return.

While that may be true in theory, the practical benefit is less clear. Public and private equity markets remain highly correlated over time, and the incremental diversification benefit must be weighed against added complexity, costs, and oversight challenges.

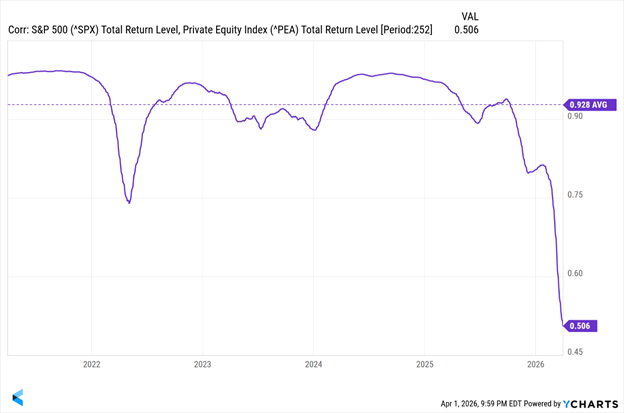

While correlations between public and private equities fluctuate over time, they have historically been highly correlated, with an average trailing 3-year correlation between the S&P 500 and the Private Equity Index over the past 5 years of 0.928.

In many cases, the diversification argument alone is not sufficient to justify inclusion.

- Risk, Complexity, and Oversight

Alternative investments introduce additional layers of complexity—leverage, capital call structures, and less transparent risk exposures.

From a fiduciary perspective, complexity increases the burden of oversight. Standard monitoring tools and peer group comparisons are often less effective, making it more difficult to evaluate performance and risk within a traditional framework.

If an investment cannot be monitored with the same rigor as existing options, its inclusion becomes more difficult to defend.

- Participant Suitability and Use Case

Finally, there is the question of participant appropriateness.

Defined contribution plans serve a broad population, many of whom rely on default investment options and may not fully understand more complex strategies. This raises important considerations around communication, education, and behavioral outcomes.

For this reason, any future implementation is far more likely to occur within diversified vehicles—such as target-date funds or an Advisor Managed Account (AMA) solution —rather than as standalone options within a core lineup.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Lineup Construction Still Matters

Beyond individual investment considerations, alternatives must be evaluated within the broader context of lineup construction.

Every plan must balance diversification with simplicity. Too many options can create confusion among participants and increase fiduciary risk. As a result, the bar for adding any new asset class—particularly one with higher costs and complexity—should be high.

Our approach has consistently emphasized efficiency: covering major asset classes while limiting peripheral exposures unless they serve a clear and measurable purpose. That philosophy does not change with the introduction of alternatives.

In fact, it becomes even more important.

Alternatives should not be viewed as a replacement for core exposures, nor as a default addition to improve outcomes. They must demonstrate a clear role within the lineup—one that justifies their inclusion relative to simpler, more transparent alternatives.

What Hasn’t Changed: Fiduciary Responsibility

Despite evolving guidance, the core fiduciary principles under ERISA remain unchanged.

Plan sponsors must act prudently, ensure fees are reasonable, and select investments that are appropriate for participants. If anything, the inclusion of alternatives raises the standard for documentation, due diligence, and ongoing monitoring.

As we’ve noted in prior discussions, the industry has a well-understood dynamic: the first to introduce a new structure is often the first to be tested in litigation. That reality continues to shape adoption.

A Practical Path Forward

While interest in alternatives is likely to grow, widespread adoption is unlikely to happen quickly.

Early implementations will likely:

- Be limited in size.

- Be embedded within diversified structures.

- Focus on operational feasibility and liquidity management.

For advisors, the role remains consistent: guide plan sponsors through a disciplined evaluation process, grounded in fiduciary best practices rather than product-driven narratives.

This includes helping clients:

- Distinguish between access and appropriateness.

- Evaluate whether alternatives solve a real portfolio need.

- Understand the trade-offs between diversification, cost, and complexity.

Conclusion: The Burden of Proof Remains High

The conversation around alternatives in 401(k) plans is evolving, but the underlying principles are not.

Regulatory clarity may make it easier to consider these investments. It does not make them easier to justify.

Ultimately, the decision comes back to the same question we have emphasized throughout:

Not “Can we add alternatives?”—but “Should we?”

And more importantly:

Can we defend that decision within the context of a disciplined, participant-focused investment process?

By Michael Barczak, VP, Investment Due Diligence

8862093.1. – 7APR26A