Netflix – Netflix delivered a jaw-dropping update with the addition of 13.12 million new subscribers in the fourth quarter. The company previously suggested subscriber additions would be similar to the third quarter where it added nearly 9 million new households. The company has been on a global campaign to crackdown on password sharing which clearly seems to be working. The initiative was initially delayed in the United States due to concerns it would lead to higher cancellations, but that hasn’t been the case. This latest update brings global paying subscribers to 260 million, 30% of which reside in the US and Canada. Unlike cable, which reached its peak in the US with 105 million about a decade ago, streaming is a global business. It is estimated that 700-800 million households pay for TV globally; implying not only does Netflix have room to keep growing in the US, but it is also in the early innings internationally.

The new management team, co-CEOs Ted and Greg, see plenty of opportunities to continue growing the business and delighting customers. They’re investing in series and film content, to the tune of roughly $20 billion annually, but believe there is an opportunity to add in live and sports-adjacent programming. In fact, the company just announced a 10-year partnership with WWE that will make it the exclusive home for all WWE shows and specials. Importantly, these WWE live performances will not be available on traditional cable TV beginning in 2025, an omen of what’s to come for the rest of live sports. The company continues to invest in mobile gaming which is an endeavor they believe will ultimately pay off, particularly as they move more heavily into ad-based products.

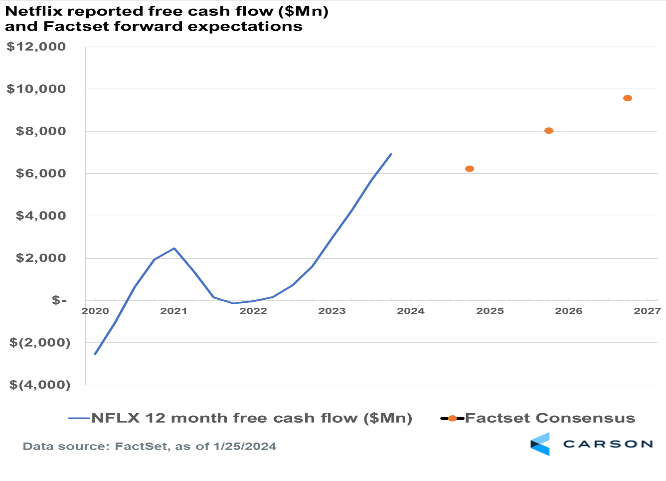

For investors, the improving profitability is arguably as important as the new subscribers. Netflix generated just shy of $7 billion in free cash flow during 2023. An impressive feat, particularly given its competition is losing billions of dollars trying to catch up. Its profitability continues to improve as the business scales, management is guiding to a 24% operating margin in 2024, up from the nearly 20% margin it delivered in 2023. Netflix towers over other streaming competitors because of its scale and, given it can still grow subscribers at a rapid pace, we expect its scale and profitability will continue to increase.

Tesla – Tesla’s Q4 earnings did nothing to improve investor sentiment. It wasn’t so much the earnings, which actually had some positive updates, it was the outlook where “growth may be notably lower” in 2024. In typical Elon fashion, we heard updates about his Cybertruck pet project, the Optimus humanoid robot, and it wouldn’t be an earnings call without mentioning Artificial Intelligence. Wall Street hates uncertainty and an unspecific announcement about slower growth causes analysts to fear the worst.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

That said, there were some encouraging aspects of the fourth quarter earnings, namely a sequential improvement in gross margin and a decline in inventory. First and foremost, these metrics imply that demand is healthy despite the widely reported slowing of EV sales in the US. Furthermore, the improvement in gross margin suggests that pricing is stabilizing.

Recall, Tesla began slashing EV prices in early 2023 as demand faltered. Competitors like Ford and GM followed suit, dubbing this the EV Pricing Wars. It was a rough year. Despite delivering nearly 40% more vehicles, sales from cars in 2023 grew only 1% and earnings for the company fell a staggering 23%! However, Tesla still generated more than $4 billion in free cash flow, and we believe it is winning the war. 2023 was far worse for the competition. Ford lost over $1 billion on its EV operation and has scaled back future plans. Again, scale and scalability are important; Ford produced just over 100,000 EVs in 2023 while Tesla sold 1.8 million. What makes Tesla so valuable is its scalability that other car companies lack. GM sells roughly 6 million gas powered vehicles worldwide each year, but it’s manufacturing model never led to scaled profitability. Tesla earned roughly the same amount of income as GM, in a year with profitability down due to price cuts and at 1/3rd the scale.

Speaking of car prices, the reason for slower growth in 2024 is to focus the company on a mass market vehicle, or a car priced at $25,000-$30,000. There are several reasons consumers are hesitant to buy an EV, but the biggest issue is EVs cost more than gas-powered vehicles. As we saw, when Tesla lowered prices it spurred demand. If the company can ultimately deliver a car that is cheaper to buy than a gas guzzler, it could potentially unlock mass market appeal to the tune of ten million cars or more and lead to enormous scale. Elon has been known to make bold predictions about timelines, but they expect to start producing the mass market vehicle in late 2025. It seems 2024 is going to be tough, but for long-term shareholders Tesla’s obsession with making EVs affordable seems like the right decision.

02087135-0125-A