Exchange-traded funds (ETFs) continue to gather significant assets, generally at the expense of traditional open-end mutual funds (albeit not completely). In the first quarter alone, ETFs have taken in some $425 billion in net flows, while traditional open-end mutual funds have seen $92 billion in investors assets leave, according to Morningstar. Beneath the surface of continued strong growth, there are a few important trends with ETFs to monitor.

Private (Equity) Assets in ETFs

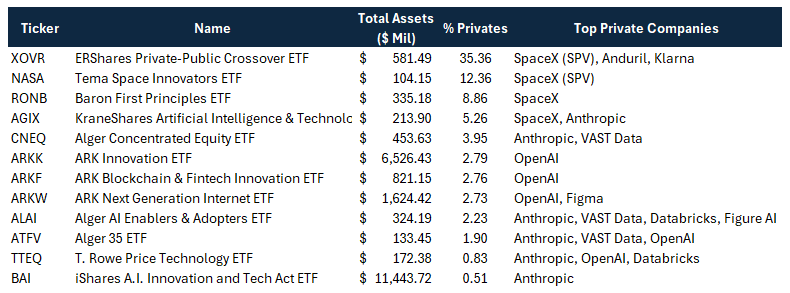

The ability to hold securities deemed illiquid within a traditional 1940 Act fund (open-end mutual fund or ETF) has been possible for a long time, subject to a 15% cap and certain requirements on valuation. In recent years, illiquid or less-liquid assets – like shares in private companies – have become a much more popular or sought-after investment. Traditionally in the mutual fund wrapper, managers could manage around this illiquid exposure because they could choose what to sell to fund redemptions (ok for managing illiquidity, bad for taxes). With the rise of ETFs, the ability to own illiquid assets remains – but intraday trading and in-kind creation-redemptions add more complexity. When there is a will (or just a lot of demand) there is a way, and many ETF providers have found ways to include private securities in ETFs (we are just looking at the equity side here, not credit). Below is a non-exhaustive list and the space continues to evolve. This is a combination of new entrants in the private space and established active managers that have owned private securities in traditional mutual funds or other vehicles and are now using private shares to add value to their active ETFs. It should be noted that the 15% illiquid max refers to the ability to add more shares. If outflows lead to a larger allocation to the illiquid portion the fund may be able to maintain the exposure, but cannot add more.

Sources: Carson Investment Research, Morningstar Direct, ETF Daily holdings files as of 4/14/2026. Private % and companies are subject to change at any point. Larger private exposures absolutely do not imply a more or less attractive investment. Consider all risks and objectives before investing.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

ETF as a Share class

I previously wrote about this concept after progress was made by Dimensional Fund Advisors (DFA) towards launching the first ETF-as-a-share class since Vanguard’s patent expired. As of March 20th, the Dimensional US Micro Cap ETF (DFMC) began trading as a share class of their long-standing micro-cap mutual fund, technically becoming the first “active” mutual fund with an ETF share class. Still a work in progress, but several third-party websites have been able to reference the fund’s full 40+ year track record when looking up the ETF DFMC. It should also be mentioned that in February of this year, F/M Investments did this in reverse – offering a mutual fund share class of their existing TBIL ETF. Many other fund managers, including DFA, have filed for this ability, all likely watching and waiting as Dimensional was happy to be the first mover.

Structured Notes

Grabbing fewer headlines than the cases discussed above, another trend has been certain ETFs including income-producing structured notes (or at least a synthetic version) within the ETF structure, typically in a perpetual way that reduces the need to continually roll notes forward. To us, this is a natural evolution of the defined outcome (often just referred to as “buffer”) ETF trend and could be an efficient and positive development for investors. So far, many autocallable and barrier structures have been replicated in the ETF structure, often with double digit yields. It is important to understand all the nuances of these products, from trading to barrier ranges and periods, as well as the laddering approach many take.

Beyond the structural advantages of ETFs, their ability to provide access and bring liquidity to an ever-evolving list of asset classes further enhances the usefulness of the structure. Not all innovation moves in the same direction, however. With every new actively managed ETF from an established provider, there is usually a corresponding launch or filing for a new levered or inverse product. Prediction and betting markets finding their way into an ETF wrapper is also a hotly debated topic in the space that we continue to watch for any potential approval. Sifting through the ETF universe is becoming an unwieldy task, and we at Carson want to be there for our clients and advisors to make sense of the fray.

For more content by Grant Engelbart, VP, Investment Strategy and Research, click here.

8876930.1. – 15APR26A