Why long-term investors shouldn’t pay for flexibility they don’t need.

By Kevin Bruce, CFA®, CFP, Analyst, Alternative Due Diligence

Many advisors share the same core playbook with clients: think long-term, stay invested, diversify, and do not let short-term volatility derail the plan. It is the foundation of wealth creation. We remind clients that cash (the most liquid investment) may not outpace inflation, may not support decades of retirement, and may not participate when markets rise. They understand and they agree. If they did not, they would most likely not be clients in the first place.

So, we help them build a long-term portfolio designed to support their goals and fund cash flows 10, 20, even 30 or more years into the future.

But in this portfolio-building process, we often subtly abandon our own message. Even when money is not needed for many years or even decades, we place almost every investable dollar into fully liquid, constantly priced public securities. Portfolios built for the long haul are given the ability to unwind instantly, as if the entire plan might change at any moment. It is a quiet contradiction. We encourage long-term behavior while designing portfolios around short-term access.

If liquidity is costly in cash due to inflation and opportunity costs, and we all agree it is, why do we assume it suddenly becomes free the moment assets move into investments?

The Liquidity Penalty

For decades, the industry has talked about the “illiquidity premium,” the additional return private assets generate over traded markets. But that language implies the baseline is correct, and illiquidity is some kind of special reward. It turns the truth upside down. Liquidity is the deviation from the norm. Illiquidity is the natural state of long-term capital. The return difference is not an illiquidity premium, it is a “liquidity penalty” embedded in public markets. Liquidity is not free. It can erode return potential, which can create an emotional toll, increasing the likelihood of behavior that further reduces realized returns.

Clarity Around Liquidity

This isn’t about diminishing the importance of public markets. They remain the foundation of most portfolios, providing flexibility, transparency, and broad access to global growth. But when every dollar is invested as if it might be needed tomorrow, the portfolio may be paying a liquidity penalty it doesn’t need to pay. Long-term capital deserves a long-term structure, and private markets can support the portion of a portfolio designed for goals far down the road.

Client Acceptance

In the very parts of their financial lives that create the most wealth—homes, businesses, and retirement accounts—many clients already embrace illiquidity without hesitation.

Homeownership is the clearest example: houses do not receive a daily quote, and the inability to sell instantly is a feature that keeps owners focused on use and long-term equity growth. No one asks for a minute-by-minute Zestimate. A daily appraisal would be both costly and unnecessary.

Business owners understand this even more deeply. They pour capital and energy into their companies with no concern for daily valuation. Their focus is on building, improving, and creating future value, not responding to every passing opinion of worth. Illiquidity allows them to work on their businesses rather than trade them.

Retirement accounts follow the same logic. They physically prevent impulsive access. That restriction protects wealth from short-term fear and preserves it for long-term purpose.

When a long-term focus is clear, illiquidity feels natural, not risky. And daily liquidity only invites investors to worry about things that don’t matter to their goals.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

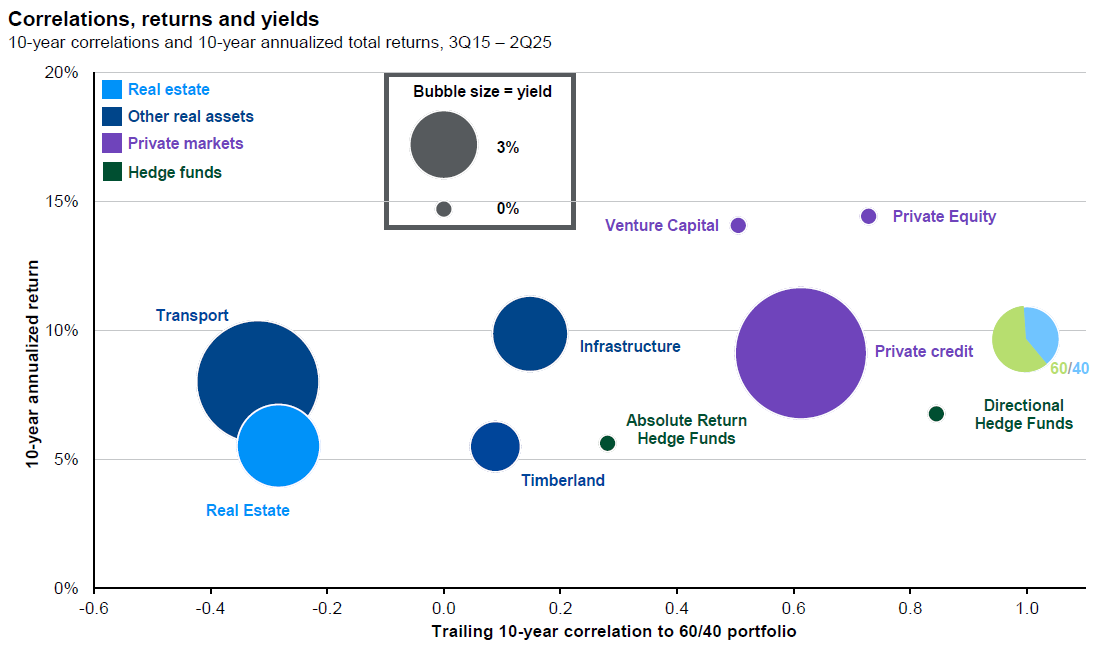

Modern Portfolio Theory

Harry Markowitz demonstrated more than half a century ago that portfolios become more efficient when they include assets whose returns don’t move together.1 That foundational idea has only strengthened over time. Decades of research from firms such as Cambridge Associates,2 MSCI,3 and others has shown that less liquid alternative investments, including private equity, private real estate, and private credit, offer return streams with meaningfully low correlations to traditional stock and bond markets, while also delivering strong long-term performance. When these distinct drivers are added to a portfolio, the efficient frontier expands, and the likelihood of achieving long-term goals improves. Excluding them isn’t a sign of prudence; it’s a structural decision to accept less than what a diversified, long-term portfolio could deliver.

Source: JPMorgan – Guide to Alternatives, 4Q 2025

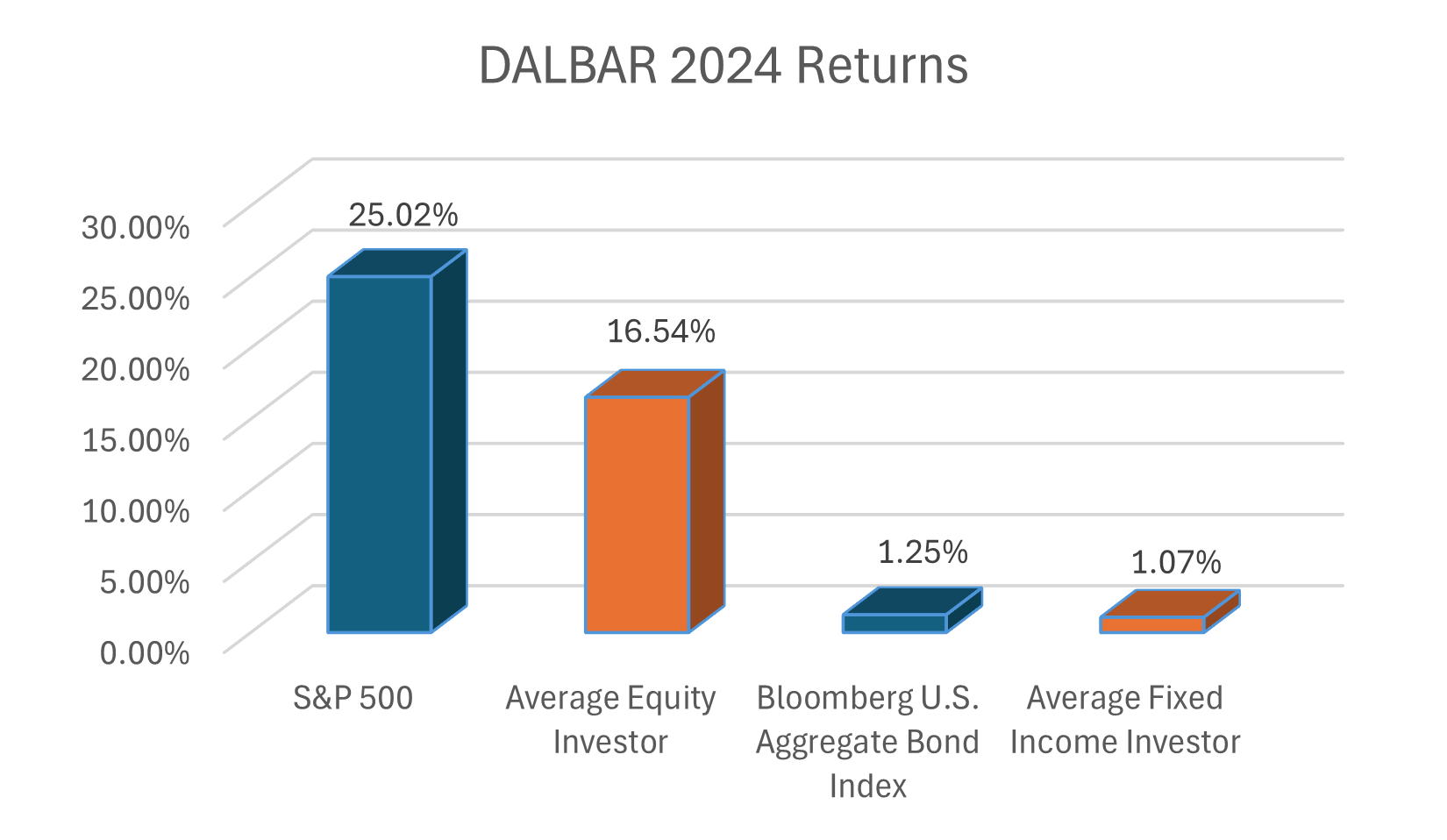

Behavioral Finance

There are also behavioral reasons liquidity may be penalized. Kahneman⁴ and Thaler⁵ showed that losses are felt more intensely than gains. The more frequently investors observe losses, and the easier it is to trade, the more likely they are to lock those losses in. Decades of DALBAR⁶ and Morningstar⁷ studies have documented the resulting gap between market returns and investor returns, with liquidity playing a starring role. Liquidity can feel like an escape hatch, but like an ejection seat on a submarine, it offers the illusion of safety while being fundamentally misaligned with the environment. Less liquid structures, by contrast, introduce constructive friction that enforces discipline and helps investors stay aligned with long-term plans.

Source: DALBAR Quantitative Analysis of Investor Behavior Report 2024

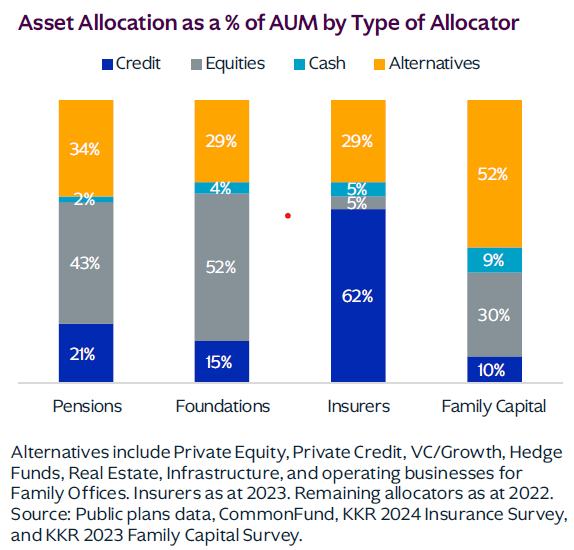

Institutional Adoption

The most sophisticated investors in the world, endowments, sovereign wealth funds, large pensions, and multigenerational family offices, have already embraced substantial exposure to private markets. Not due to fads or marketing campaigns, but because when capital is genuinely long-term, paying for daily liquidity makes no sense. They reduce the liquidity penalty intentionally, not to increase risk, but to improve outcomes.

Source: KKR: Global Macro Trends 2024

The Smoothing Critique

A fair critique of some illiquid assets is that private markets “smooth” volatility rather than eliminate it, but the opposite is also true. Public markets don’t merely reflect volatility; they amplify it. They turn short-term uncertainty into constant repricing and emotional noise. That amplification isn’t a clearer truth, it’s a distortion created by liquidity and leveraged short-term incentives. Neither system perfectly measures value in the moment. The better question is: which system more accurately reflects the purpose of the capital it holds?

Conclusion

Liquidity is neither inherently beneficial nor detrimental; its value is contingent on the purpose of the capital it serves. When portfolios designed to fund long-term objectives are structured to allow for continuous liquidity, investors may incur a persistent and compounding liquidity penalty in the form of reduced expected returns and increased behavioral risk. Evidence from institutional allocation practices, modern portfolio theory, and behavioral finance suggests that long-horizon capital is most efficiently deployed when its structure reflects its time horizon. We often say volatility is the toll we pay to invest. By thoughtfully allocating a slice of long-horizon assets to less liquid private markets, investors can potentially pay a smaller toll.

¹ Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77–91.

(Seminal paper establishing diversification and the efficient frontier.)

² Cambridge Associates. (Ongoing, various annual publications). Private Investments Benchmarks Reports.

(Empirical evidence showing long-term outperformance and diversification benefits of private equity and private real assets.)

³ MSCI Research. (2020). Private Asset Valuation and the Role of Illiquidity in Portfolio Diversification.

(Analysis of correlation differences between private and public markets and portfolio construction benefits.)

4 Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263–291.

(Original research establishing loss aversion — losses hurt more than gains feel good.)

5 Thaler, R. H. (1985). Mental Accounting and Consumer Choice. Marketing Science, 4(3), 199–214.

(Reinforces how investors perceive gains/losses and make suboptimal choices.)

6 DALBAR, Inc. (Annual). Quantitative Analysis of Investor Behavior (QAIB).

(Long-standing data proving investors significantly underperform the investments they own — largely due to timing mistakes.)

7 Morningstar. (Various annual Mind the Gap studies — e.g., 2022, 2023). Investor Returns vs. Total Returns.

(Demonstrates the persistent gap between market returns and investor returns; liquidity-enabled behavior is a key driver.)

8675576.1. – 19DEC25A