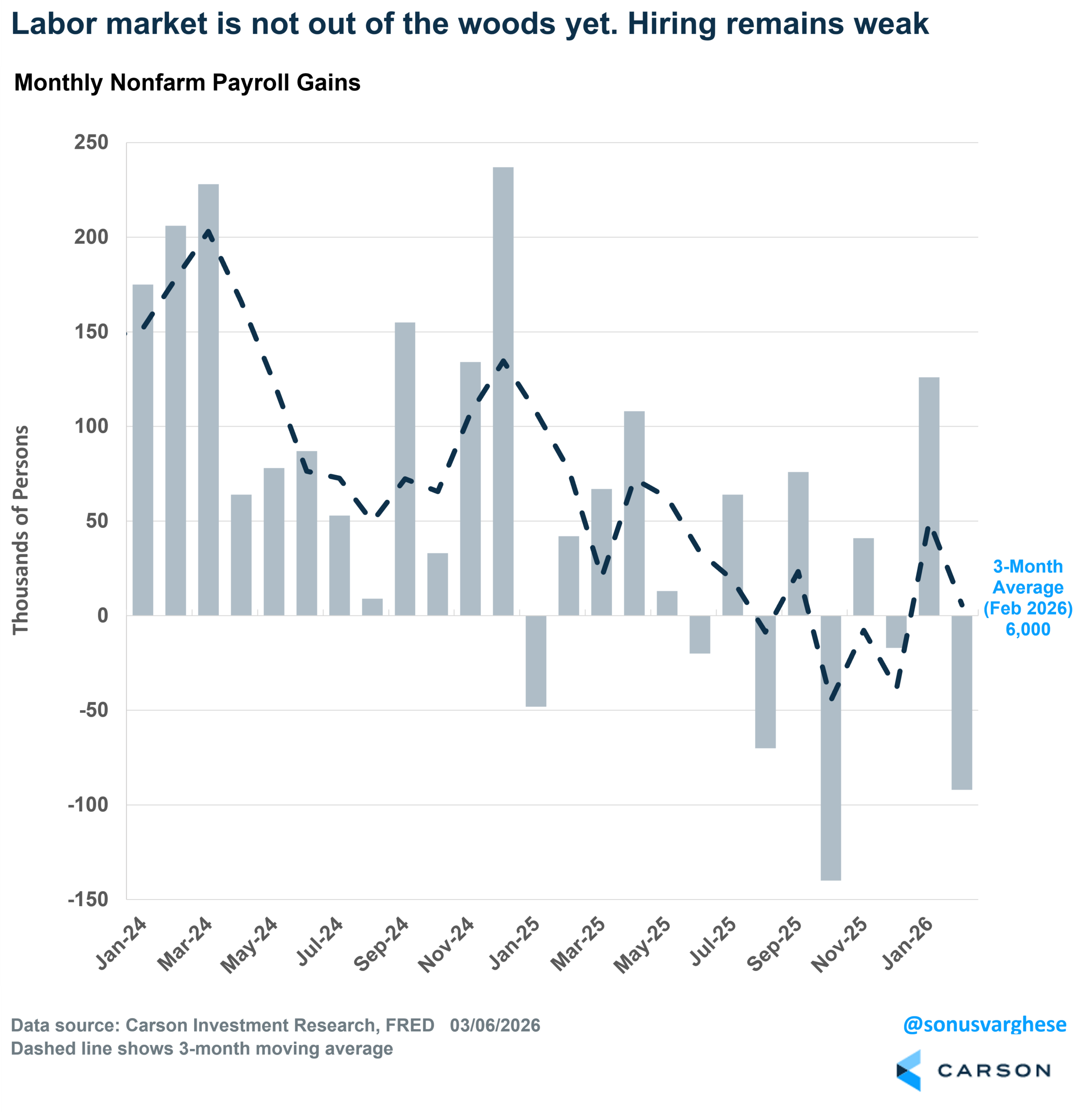

The February payroll report was an ugly one, and a bit of a mess. The economy lost 92,000 jobs in February, whereas forecasters projected a gain of 55,000. We saw significant revisions for the last two months as well:

- December payrolls were revised down by 65,000, from +48,000 to -17,000.

- January payrolls were revised down by 4,000, from +130,000 to +126,000.

The revisions obviously tell you that we should take monthly numbers, and even the previous month’s data, with heaps of salt. The three-month average is more useful here, and that’s clocking in at just under 6,000. That’s not good and not enough to keep up with population growth. As you can see in the chart below, we’ve now alternated between job creation and job losses each month for the last ten months. The payroll data is a mess right now, and likely not giving us a good picture of what’s happening, one way or the other (good or bad).

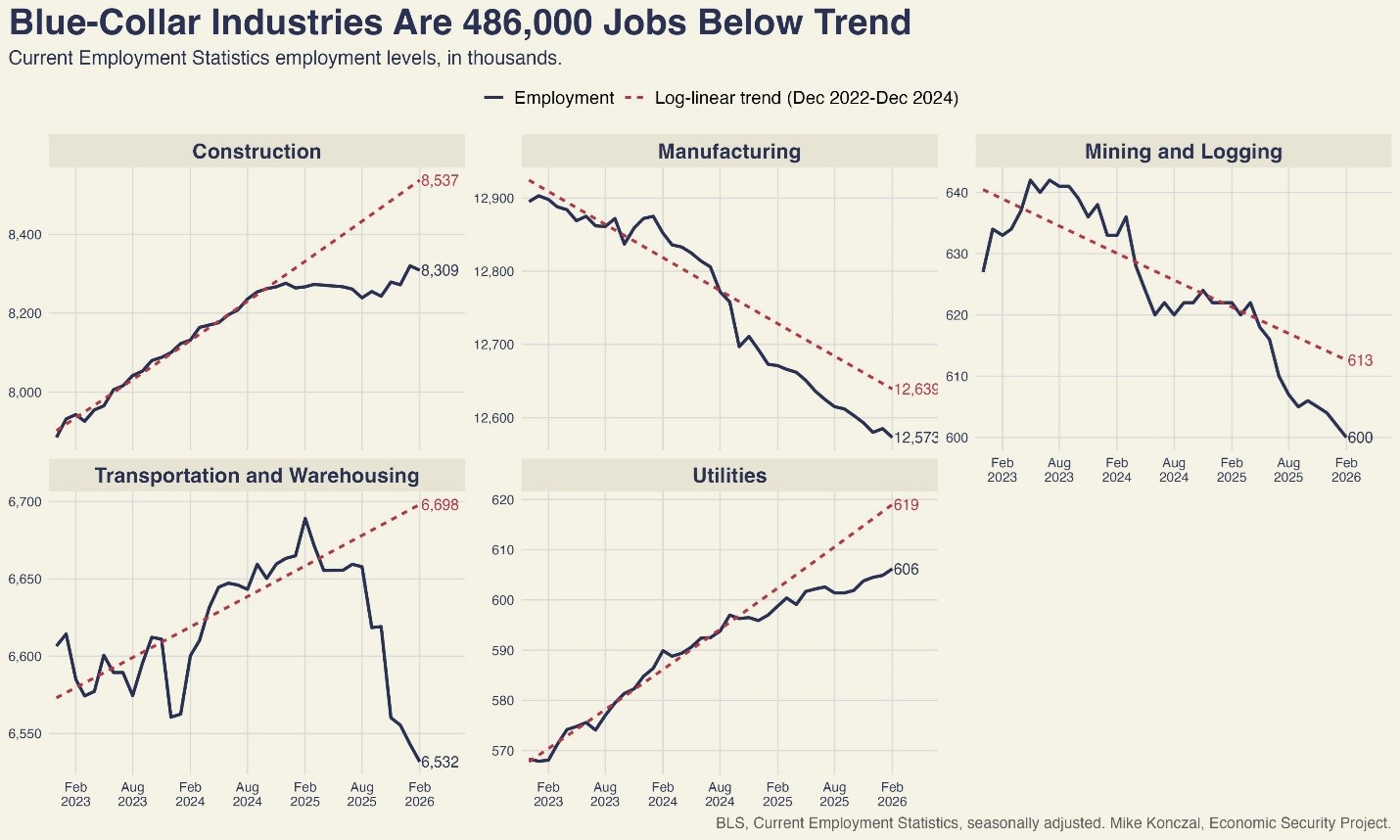

Interestingly, the job market slowdown is not really about AI-related layoffs. The healthcare sector was the main engine of job growth last year, but the industry lost 19,000 jobs last month after averaging 73,000 jobs per month over the prior three months (November-January). This is partly because of a strike of 31,000 physicians. But job creation has been weak even in blue-collar industries: construction, manufacturing, transportation, mining and logging, and utilities lost 35,000 jobs in February. Job creation in these sectors has been running well below trend over the past year (about 500,000 jobs below where you’d expect based on the 2023-2024 trend).

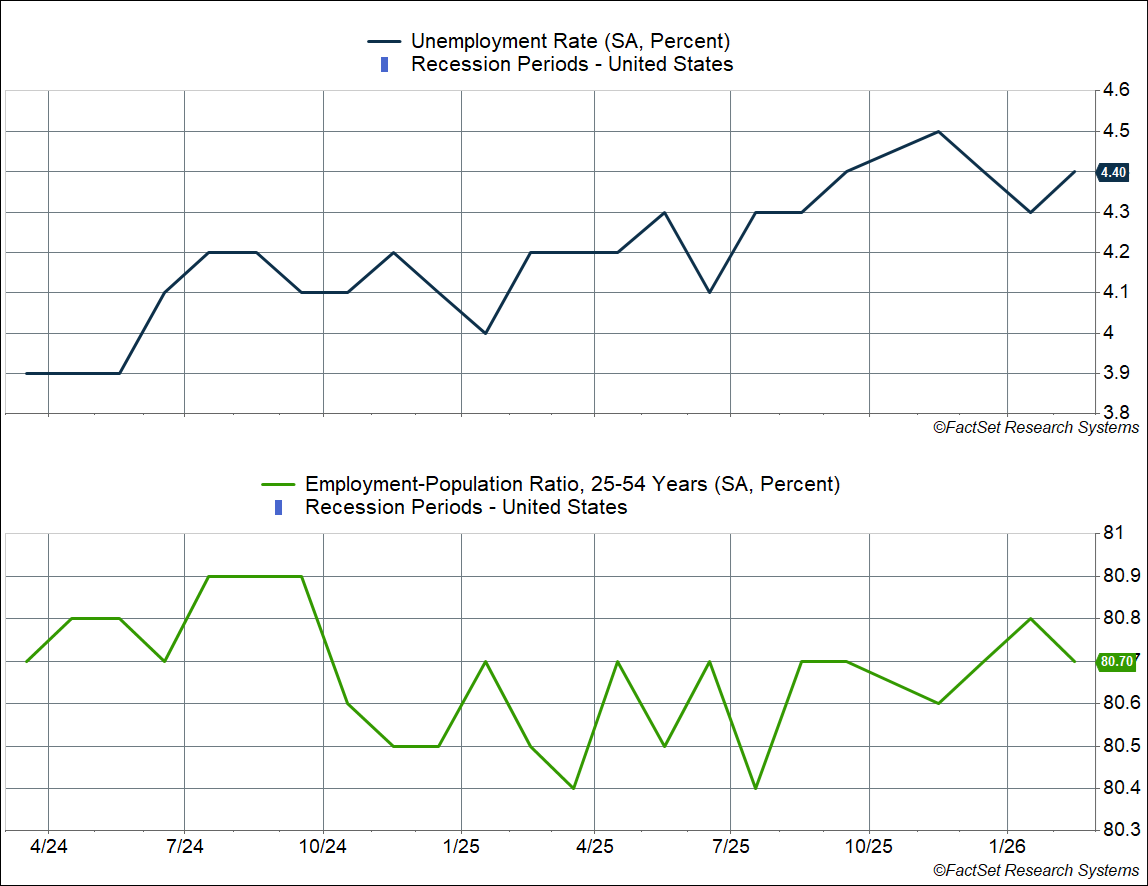

The unemployment rate did tick up from 4.3% to 4.4%, but that is still low relative to history. One month doesn’t make a trend, but there’d be some real worry if it continues to rise. But it wouldn’t be all bad if the unemployment rate stabilizes around here. For perspective, the unemployment rate was 4.1% a year ago. The labor market has clearly cooled since then, especially after Liberation Day, but things may have stabilized for now.

More positive is the prime-age (25-54) employment population ratio. It did fall from 80.8% to 80.7%, but that’s still close to this cycle’s high of 80.9% and higher than at any point between May 2001 and June 2024. It tells you that more people in their prime-age working years have a job now than at any time during the 2000s and 2010s economic expansions (as a percent of the population).

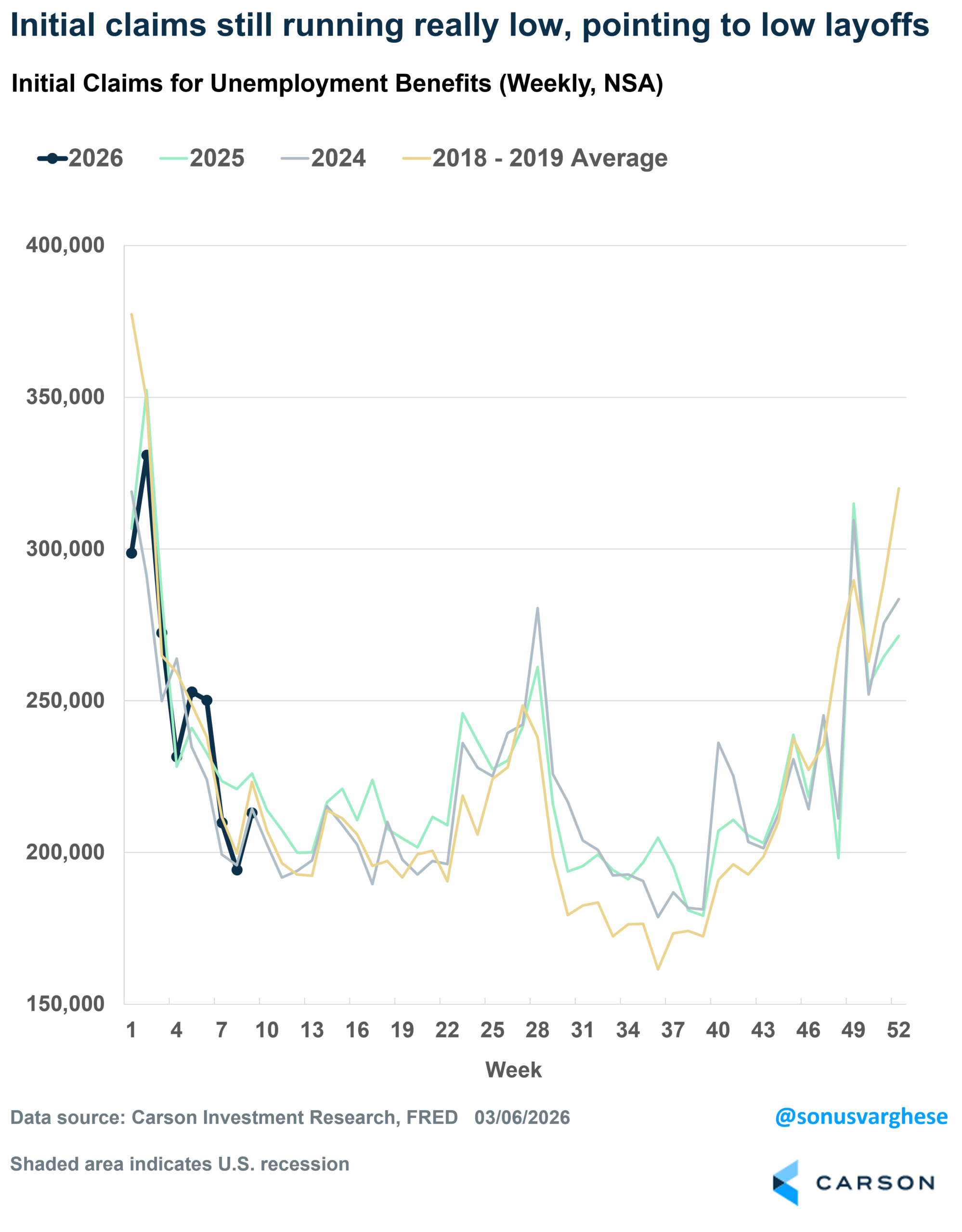

Another positive is that initial claims for unemployment benefits, which offer a real-time view of the labor market, remain really low. As of last week, initial claims were running below where claims were a year ago, or even in the same week in 2018-2019.

The big picture here is pretty much the same as it has been over the last two years. We’re in a low-hiring, low-firing economy. Companies have really clamped down on hiring recently, especially after Liberation Day last April, amid increased economic uncertainty. But that also leaves the economy vulnerable to a shock, especially if that leads to a pick-up in layoffs.

The War With Iran Is Creating an Inflation Shock

As I wrote in my prior blog, inflation was already elevated. The January core Personal Consumption Expenditures (PCE) Price Index is going to be hot based on already released data, likely sending the year-over-year pace to 3.2%, the fastest pace since November 2023. That’s before any impact of what’s happening in the Middle East.

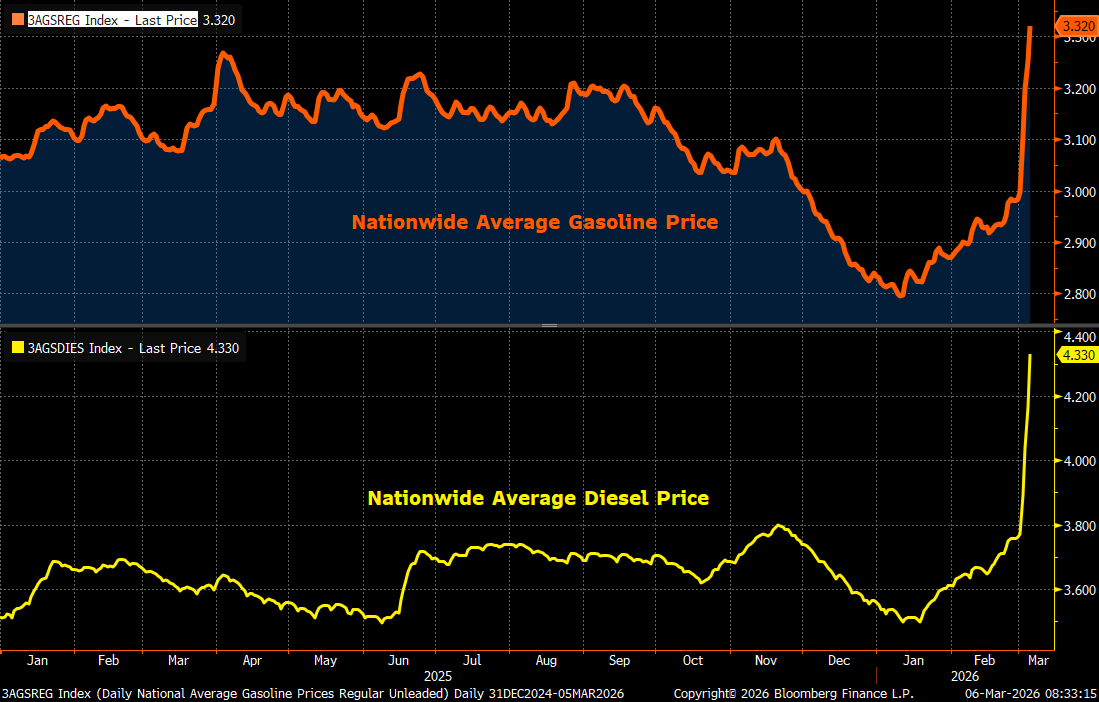

Gas prices have now surged to the highest level in almost two years, with nationwide average gas prices rising over $3.3/gallon. It was close to $2.80/gallon a couple of months ago, which means gas prices have surged close to 20%. Diesel prices have surged even more, hitting $4.12/gallon, the highest since November 2023. Diesel prices were close to $3.50/gallon a couple of months ago. The bad news is that prices are probably heading higher for now.

Higher diesel prices are going to increase transportation costs, which may put upward pressure on food prices as well. Fertilizer costs are also surging as the war disrupts supply and shipping. Natural gas, which is a key ingredient for fertilizer production, has seen prices surge with Qatar (the world’s second largest producer) shutting production.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The Fed Has a Problem, and So Do Households

This is the picture we’d be looking at even if the Middle East hostilities didn’t happen:

- Elevated inflation (3%+) as 2026 gets underway

- Potential AI-related bottlenecks, including items like memory chips that are required for goods like computers, electronics, and even cars

By itself, the above two points would imply the Fed would have a hard time justifying cuts this year. Yes, labor market risks persist, as February payrolls highlight. But as I noted above, the labor market clearly weakened in the middle of 2025 but has stabilized in recent months (though that doesn’t mean it’s in great shape. Keep in mind that the Fed already cut rates by 0.75%-points in Q4 to protect the labor market.

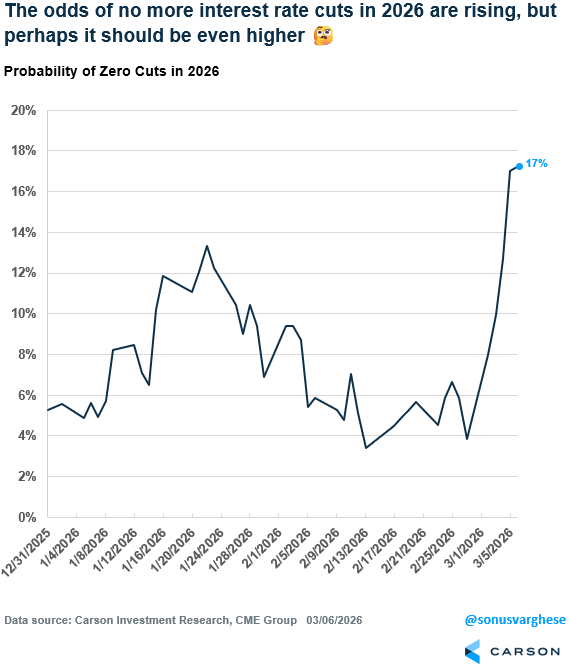

Now you have an energy shock as well. Even if you treat that as “transitory,” the case for cutting rates this year isn’t clear-cut. Right now, the market (using fed funds futures) is pricing in 100% probability of one more 0.25%-point cut in 2026, and a 71% probability of a second one. The probability of a second cut was 100% last Friday before the war started (February 28th), and markets were even pricing in 44% probability of a third cut.

Perhaps a better way to look at this is the probability of no more interest rate cuts in 2026. That’s risen from below 5% last week to over 17% right now. That’s a big shift, but perhaps it’s not big enough given the data. I’d say the probability of no more cuts in 2026 should at least be 50%, even if you discount events in the Middle East and assume things get back to normal quickly. If they don’t, and arguably it’s hard to predict what happens on that front, the probability should be closer to 100%. Even if the labor market falls off a cliff, which is not our base case now, it’s likely the Fed may focus on fighting inflation if prices really surge. Recall that the Fed was ready to send the economy into a recession (and even predicted it) when inflation surged to 40+ year highs in 2022.

Of course, higher inflation and higher interest rates are a problem for households as well, especially when the labor market is looking a bit shaky, and it isn’t easy to find a job if you lose your current one. That’s a recipe for lower consumer sentiment. For now, that is unlikely to translate to lower consumption (since it hasn’t over the last several years) – workers are still seeing fairly solid wage growth, and over the past year, households have been saving less, though that’s partly because household wealth has increased amid a strong stock market and rising home prices. But that could change if inflation picks up and layoffs pick up. We’re definitely keeping an eye on it all.

Ryan and I talked about all this in our latest Facts vs Feelings podcast. Take a listen below.

For more content by Sonu Varghese, Chief Macro Strategist click here.

8809693.1. – 6MAR26A