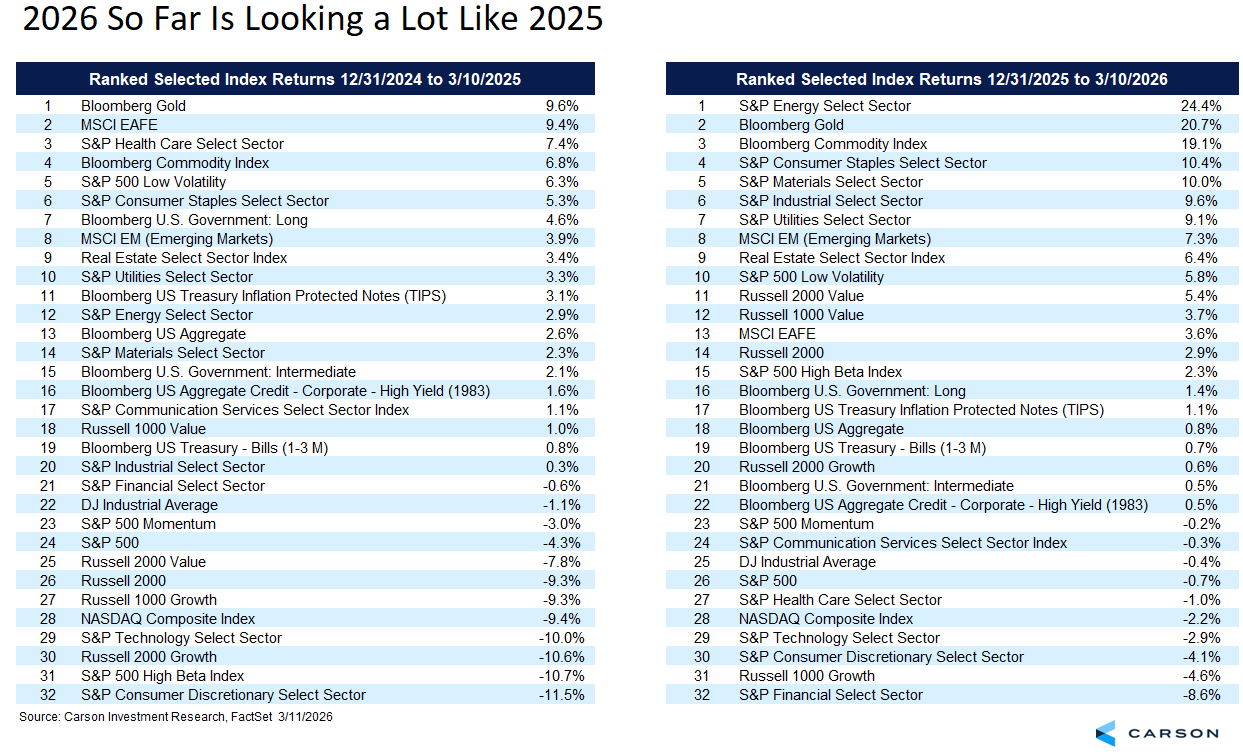

Markets in 2026 are looking an awful lot like they did this time last year. Yes, the drivers are different, but the similarities are eerie. Let’s take a look (numbers as of Tuesday’s close)…

- The S&P 500 is down year to date.

- The Bloomberg Aggregate Bond Index is outperforming the S&P 500.

- Gold is having a banner year with an even stronger start in 2026 (Bloomberg Gold Index up 9.6% at this point in 2025 versus 24.4% in 2026).

- Commodities are off to a strong start.

- Large cap growth stocks (Russell 1000 Growth) are underperforming the S&P 500.

- The technology sector is underperforming the S&P 500.

- Consistent with large growth and technology sector underperformance, a simple average of “Magnificent Seven” stock returns (seven well-known mega-cap technology-oriented stocks) is underperforming the S&P 500 by over five percentage points.

- Also consistent with the above, value stocks are outperforming growth and low volatility stocks (the S&P 500 Low Volatility Index) is having a good year so far.

- International stocks (both emerging and developed markets) are outperforming the S&P 500.

- The energy and materials sectors have done well, as have defensive sectors overall.

But there are some differences too:

- The above bullets, while highlighting a similar market texture, miss some differences in scale.

- Small cap stocks (the Russell 2000) were getting beaten up in 2025, meaningfully underperforming the S&P 500; they are in positive territory this year.

- Similarly, high volatility stocks (the S&P 500 High Beta Index) were underperforming the S&P 500 in 2025, more than doubling its loss; this year they’re outperforming the S&P 500 with a reasonable year-to-date gain.

Here’s an overview of ranked year-to-date performance. It’s a lot of information, so give it a click to see it full size:

While we know the drivers of the two years are different, there is one common factor they share: For both years there was a “decider” who was a catalyst for the market texture (said without judgment) rather than independent macroeconomic drivers, although obviously the decisions have had macroeconomic consequences. Don’t expect the same outcome for the same reason, but in both cases market volatility is a direct and immediate consequence of the president’s policy choices, which means he likewise also owns the off ramp. If 2026 in the end were to look similar to 2025, one reason would likely be because a single decisionmaker has the power to unwind some of the market risk.

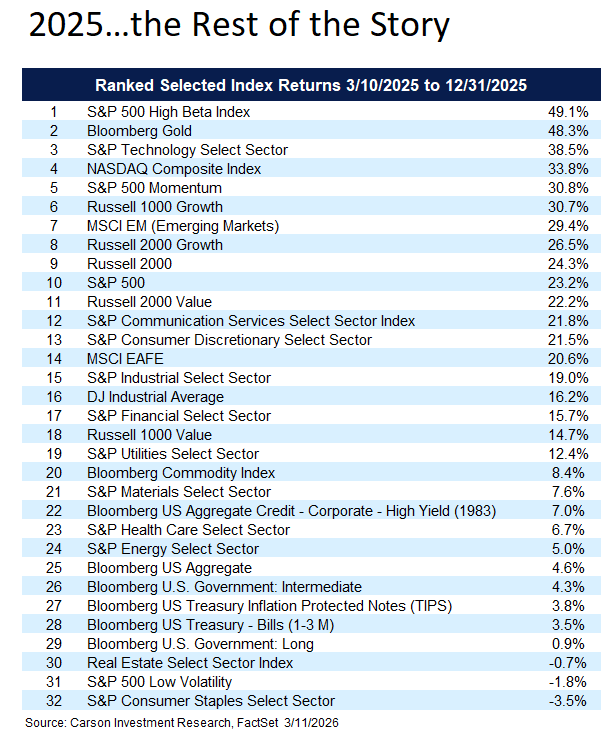

We know how the rest of 2025 shaped up (below), and this isn’t even off the market bottom, which didn’t take place until April 8 on a close basis. But we can see markets bouncing back strongly with a decided “dash for trash” element (high beta stocks), but also support from technology, momentum, and growth stocks. But international still basically kept pace with the S&P 500 over the rest of the year. And despite the risk-on environment, gold continued to draw a lot of attention, contributing to its best year since 1979 (and it’s not even close). And finally bonds, while trailing gold and stocks by a very wide margin, still had a decent year, supported by rate cuts in the fourth quarter (although long maturity Treasuries lagged other parts of the market, including Treasury bills).

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

While 2026 won’t follow the same path as 2025, it is a useful exercise in reminding us how declines feel. Maintaining perspective when you’re in the moment is always difficult, and paradoxically (as history has repeatedly shown) the impulse to sell usually grows as we get closer to the bottom.

From a market perspective, the key person dependency of this conflict keeps in place significant potential for rest-of-the year gains in our view. We believe this is plausible for several reasons:

- The conflict has achieved several objectives and major progress toward the next set of major objectives comes at significantly higher risk and cost (and some of these objectives can be pursued by other means). There will likely come a point, probably over the next several weeks, where the risk/reward tradeoff, even from the perspective of the national interest, becomes decidedly unattractive.

- The global macroeconomic drag from the conflict via higher energy prices (which flows through to broad prices, rates, central bank policy, and market volatility) have been immediate but also become stickier the longer the conflict lasts. As we’ve already seen, when markets have even sniffed out an end to the conflict energy prices have moved but there is still an impact on broader prices and that future drag becomes more meaningful over time.

- The economy already had some heightened inflation sensitivity prior to the conflict, which increases the risk of sticky prices if the conflict becomes prolonged.

- This is a mid-term election year and “affordability” has already been an issue. Unlike the price spikes when the Ukraine conflict started this conflict was chosen by the president. The circumstances are different and whether or not higher prices are worth the strategic objectives achieved is a political question, but the president owns the connection between the conflict and prices in a way that wasn’t true in 2022.

- There are several buffers against a recession still in place, including a market-friendly but extraordinary level of debt-financed stimulus. But the conflict has degraded the Fed’s ability to act as an addition buffer. Also, the low hire / low fire job market we’ve seen is stable but weaker and more vulnerable to disruption than in 2022.

- The economy has been weakened by tariff policy, but “weakened” here just means going from above-trend growth to near-trend growth, helped by a fortunately timed boost from AI spending, which we don’t expect to slow in the near term.

Put it all together, and we think markets still have solid potential to achieve something like what we saw in 2025 over the rest of the year. If that feels unlikely right now, remember it felt even less likely last year and by the lows definitively unlikely. That’s where it’s worth remembering that, like tariffs, the president has extraordinary control over how this conflict proceeds and is keenly aware of the political consequences. That doesn’t mean electoral politics will dominate his decisions, but at the very least it will be top of mind, which keeps the possibility of a 2025-like turnaround in play.

For more content by Barry Gilbert, VP, Asset Allocation Strategist click here.

8819821.1. – 12MAR26A