The 10-year Treasury yield has been climbing since bottoming at 3.95% on October 22 last year. While it’s not currently at its peak since then, it’s not far off with a close of 4.22% as of yesterday. We said in our Outlook 2026: Riding the Wave that we don’t think that lower short-term rates will have the same gravitational pull as they have historically. While it’s early, that’s held true so far.

In fact, a lot of the upward pressure on rates we expected when this was first penned, teased in my November 7 blog, has already come to pass. In that blog, I argued that the 10-year yield could finish 2026 near 4.25%. (The 10-year yield was at 4.09% at the time.) Point forecasts are always taken too literally, but I think that’s still a reasonable end-of-year forecast. If the 10-year yield presses higher and the spread between the 10-year yield and short-term yields widens (which we would expect if the Fed continues to cut rates this year), we believe intermediate core bonds would become increasingly attractive relative to short-maturity bonds. In our Outlook, we had recommended a roughly 2-1 ratio of bonds to short-maturity bonds, but we have already shifted that modestly more in favor of intermediate bonds this year.

This yield shift is not going in the direction the Trump administration wants, with higher rates acting as a brake on the economy and negatively affecting affordability. The president has undertaken explicit campaigns to lower rates, but these have not been enough to offset other favored policies with an upward rate bias, even if that’s not their goal. Among the policies enacted, suggested, or encouraged to lower rates:

- Pressuring the Fed into dropping interest rates, even if it means threatening criminal indictments (Powell, Cook).

- Reducing mortgage spreads by proposing to buy $200b in mortgage-backed securities (MBS).

- Capping credit card rates to 10%

Of course, the problem is that tariff policy is driving rates the other way, especially 10-year yields, which many other benchmarks (like mortgage rates) key off of.

The 10-year yield broke above 4.20% recently for the first time since last August, rising as high as 4.29% in the immediate aftermath of the Greenland-related tariff threat, but pulled back to 4.21% after the tariff threat was removed. But that still leaves it slightly above the 4.17% level it reached at the end of last year. What’s interesting is that the 10-year yield has trended higher over the last four months despite the Fed cutting policy rates by 0.75% over that period.

It’s instructive to look at how we’ve gotten here over the last year. On January 21 last year, the 10-year yield was 4.58%, meaningfully above its current level. Of course, economic growth expectations were flying high at the time, running at about 3% real GDP growth, although that fell after Liberation Day (2025 real GDP growth is likely to clock in around trend at roughly 2.5%, significantly better than some of the post-Liberation Day doom scenarios).

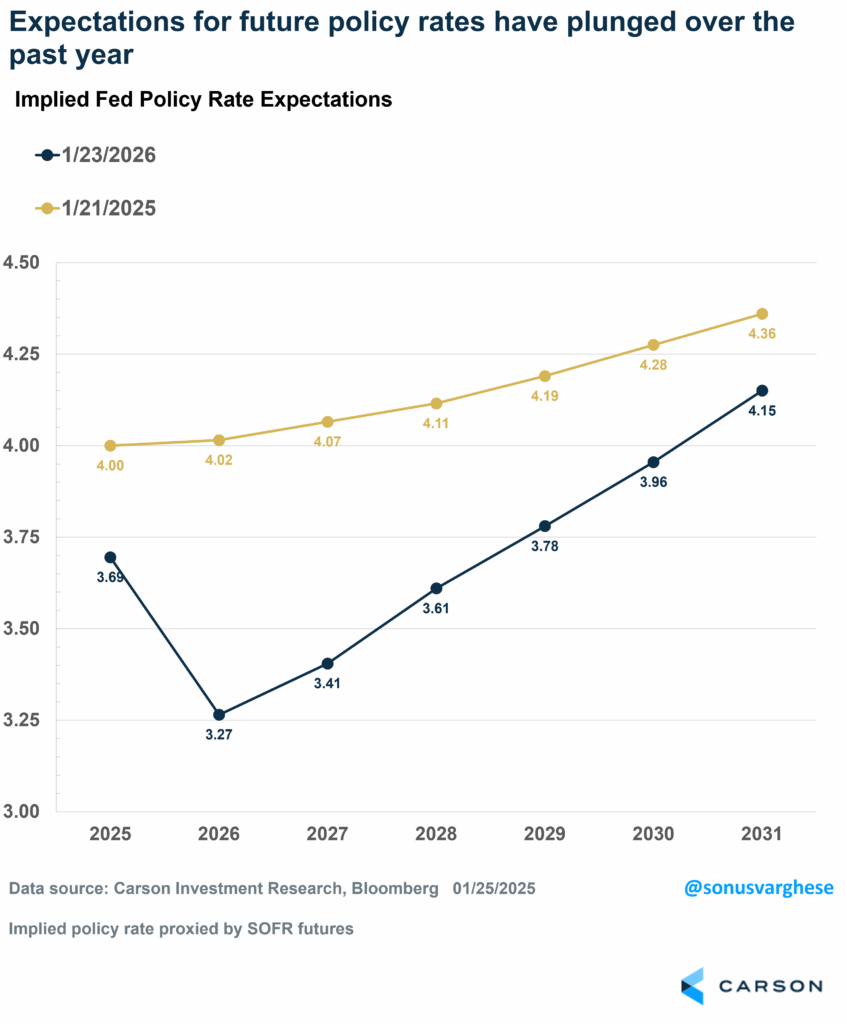

But the big reason rates fell is that policy rate expectations plunged. Here’s a look at the forward curve of market-implied policy rate expectations for the next several years, compared to where it was a year ago. You can see how expectations for policy rates in 2025 and through 2031 have collapsed since the start of the year. In other words, markets are pricing in a much more dovish Fed.

- The Fed dropped rates more than expected at the start of 2025.

- But even 2026 policy rate expectations have plunged by over 70 bps.

- Policy rate expectations for 2027 and beyond are also much lower, though the markets still expect the Fed to raise rates from 2028 onwards.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

To a first approximation, long-term rates are average expected short-term rates over the next several years, and since future short-term rates are essentially expected policy rates in the future, it shouldn’t be a surprise that the 10-year yield fell.

However, long-term yields also contain something called the “term premium.” The term premium is the additional return longer-term investors demand for future rate uncertainty, with inflation uncertainty a major component. If there is greater inflation uncertainty, investors will demand a higher “term premium” when buying a long-term bond rather than rolling over a series of short-term bonds.

Like everything that happens in the bond world, anything that pushes rates higher is bad for bond investors in the near term because it pushes bond prices down, but good for bond investors in the long run, because yields are a strong predictor of future bond returns simply because of how bonds work.

One thing to keep in mind here is that the Fed’s inflation mandate is to keep inflation “low and stable.” Usually, the focus is on “low,” but “stable” is equally critical. Inflation may very well average 2% over the next decade, but it could also be very volatile, in which case investors would charge a much higher term premium.

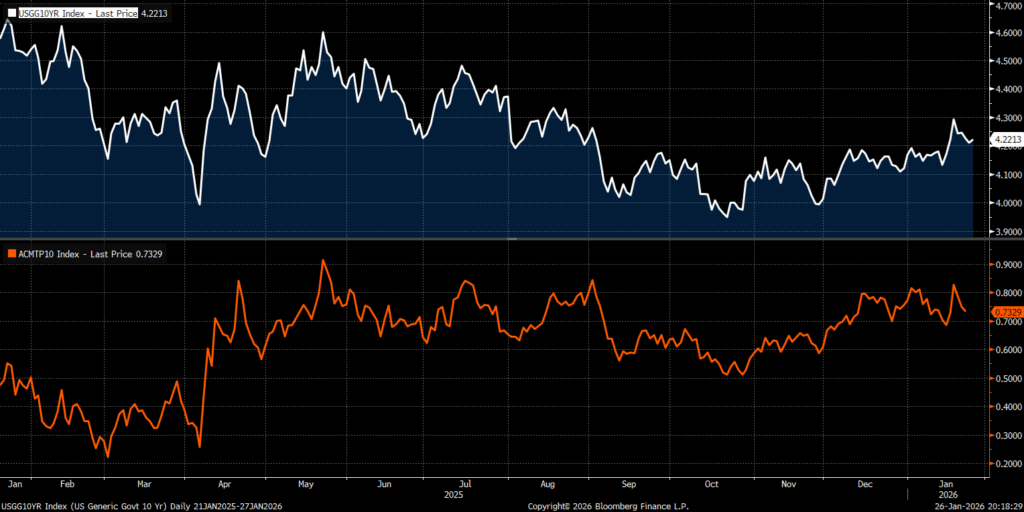

Here’s what’s interesting: while the 10-year yield has fallen about 0.26% over the past year (the white line in the chart below), the term premium has increased (the orange line). The term premium was 0.47% on January 21, 2025, and 0.73% on January 23, 2026, an increase of 0.26%. This tells us that if the term premium had stayed where it was, 10-year yields would have been about 0.25% lower than they are now, or a little below 4%, which is what the average expected path of short-term policy rates would imply. This helps us see how a policy that changes inflation uncertainty, even if it’s neutral on expected inflation, could push interest rates higher.

The policy impact of higher inflation uncertainty, even if it has little impact on the point estimate for inflation, is an underrated aspect of the tariff chaos we’ve seen over the past year. Note that if inflation expectations changed, it would tend to be reflected primarily in short-term rate expectations, not the term premium, since the Fed would likely be expected to follow a more aggressive rate path. (But there is a degree to which higher inflation tends to be accompanied by higher inflation uncertainty because of added fear of runaway inflation and how hard it can be to get inflation back under control.)

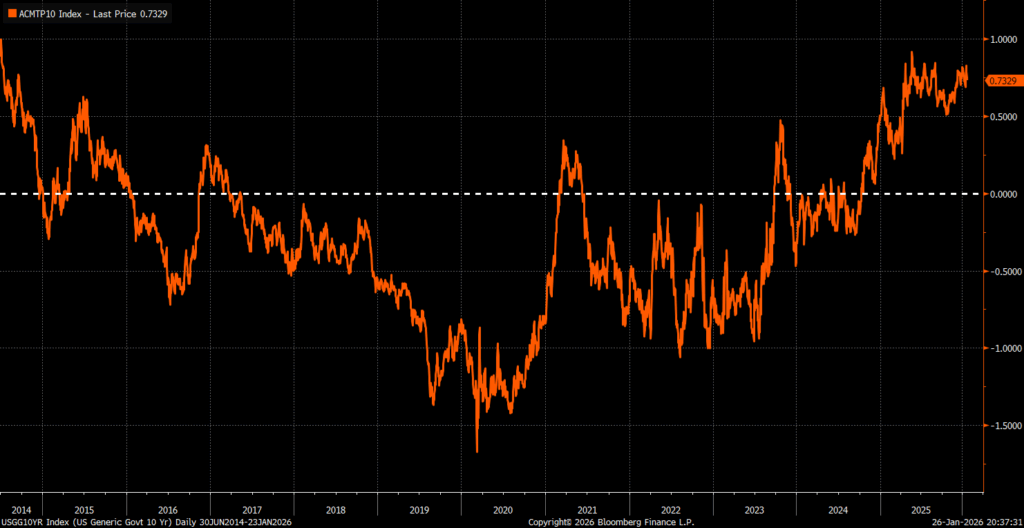

This added pressure on rates from the term premium, in fact, is something we haven’t seen much of over the past decade. Call it “the return of the term premium.” For a large part of the last decade (2016-2024), the term premium was negative, meaning investors were paying a premium to hold more risky long-term bonds rather than receiving one. One big reason was that inflation was low (along with inflation volatility), and many investors wanted the safety of Treasury bonds, not to mention their inverse correlation with risk assets. At times, major central banks were even struggling to reach their inflation targets. What’s incredible is that even in 2021-2022, when inflation was running at the fastest pace in 40+ years, the term premium was negative. It decisively rose only after November 2024 and has trended even higher since.

Here’s another way to look at what’s happening with yields. As discussed above, long-term rates are essentially future expectations of short-term rates. But if you take the 10-year or 30-year yield, it’s actually the average expected yield over the next 10 or 30 years. So knowing that it went up is not very useful, because it doesn’t tell you how rate expectations changed. Did short-term expectation shift? Intermediate term? Long term? All of the above?

But we can decompose yields into short-term yields and future expectations of short-term yields. There is a “term premium” in there too, but it’s a reasonable approximation. The 30-year yield can be decomposed into

- The 2-year yield, reflecting near-term expectations for Fed policy

- The 8-year yield expected after the first 2 years (“2-year/8-year”)

- The 20-year yield expected 10 years from now (“10-year/20-year”)

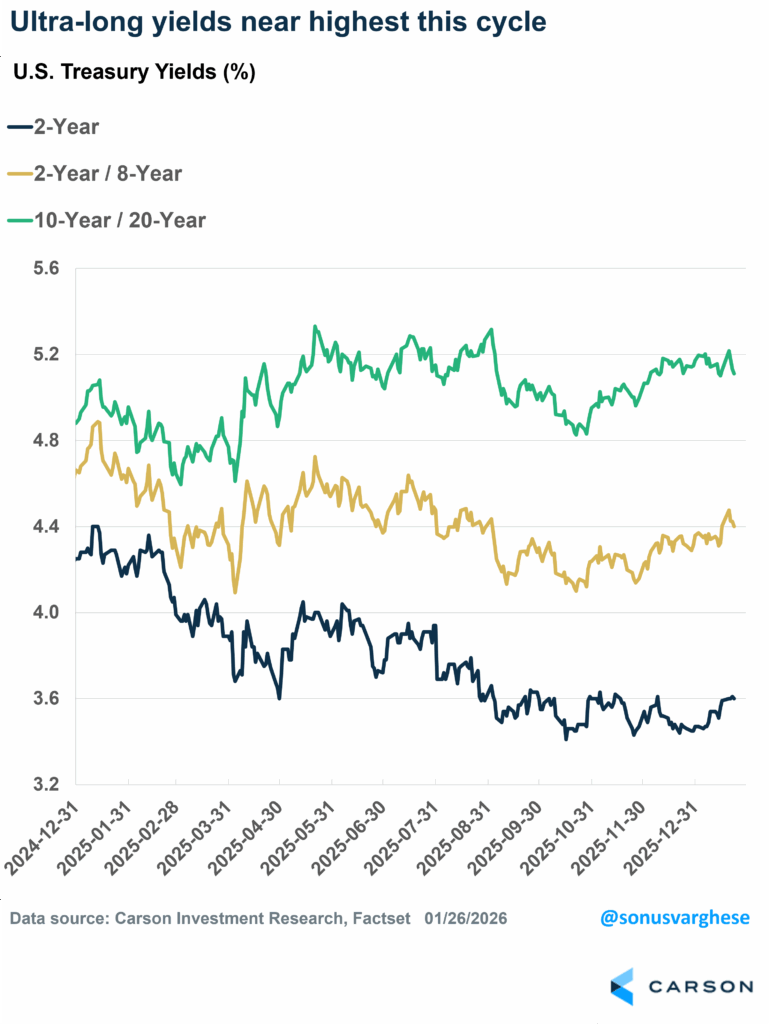

The chart below shows the results:

- The 2-year yield has collapsed since January 1, 2025, falling 0.69% to 3.60%, reflecting expectations of rate cuts.

- The 2-year/8-year yield has also fallen, reflecting a more dovish Fed and lower policy rate expectations over the intermediate term. The 2-year/8-year yields have pulled back by 0.24% to 4.40%.

- The 10-year/20-year is the most interesting here. It’s actually risen 0.20% over the past year (note that the 30-year yield is up just 0.02% because it includes what’s happening with short- and intermediate-term rates too).

In fact, 10-year/20-year yields are as high as they were in the immediate aftermath of Liberation Day, when policy uncertainty was at its maximum. Now that could partially be because this is where the term premium is expressed most strongly, but it’s still useful as a first approximation.

So why this deep dive? Up top, I said that we didn’t expect falling short-term rates to act as strongly as a gravitational force on 10-year yields going forward as they have historically. (This is for our base that near-term economic growth continues in 2026.) Because of that, we haven’t gone all in on intermediate core bonds in our fixed income/”cash” allocation, even though longer-term yields are more attractive. Don’t get me wrong—that yield advantage still counts, and we like intermediate maturities more, but we still have a healthy tactical allocation to short-term instruments too. There will come a time when shifting more fully toward bonds is appropriate. But as long as inflation uncertainty persists and the economy seems healthy, we’re certainly not there yet.

For more content by Barry Gilbert, VP, Asset Allocation Strategist click here.

8742347.1. – 28JAN26A