So much for the “AI is killing jobs” narrative, let alone “the Fed should keep rates low to protect the labor market”. We’ve been in the camp since the start of the year that the labor market looks better than a lot of economists, market bears, and even the good folks at the Federal Reserve (Fed) think. We even suggested the labor market may see some re-acceleration. Well, the data are bearing that out right now.

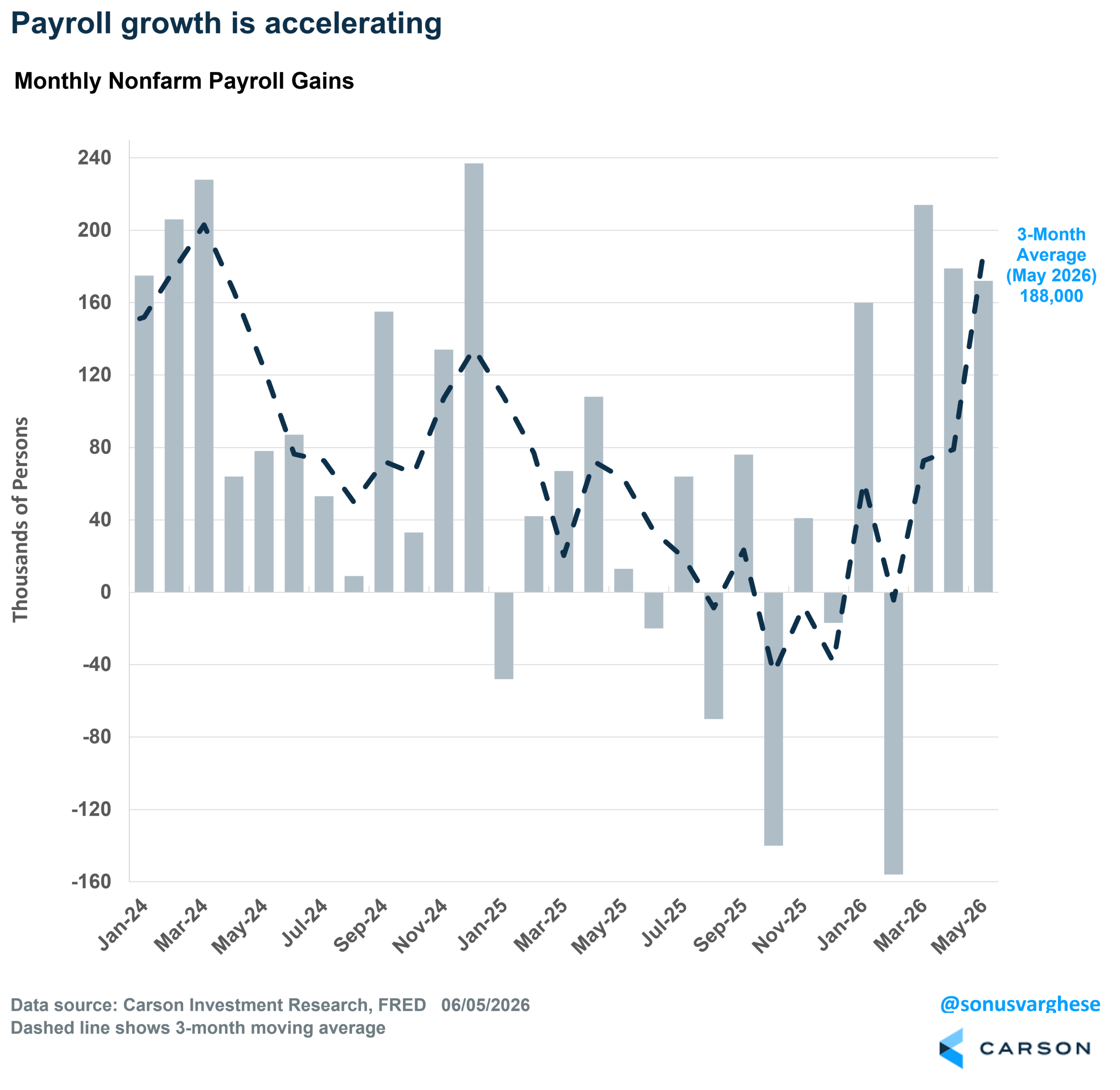

The May payroll report blew past expectations, with the economy adding 172,000 jobs, well above economists’ expectations of just 88,000. Moreover, payroll growth for March and April was revised up by a total of 93,000. That’s a reminder that the initial estimate can vary widely, and why it’s useful to focus on the 3-month average. The 3-month average of payroll gains is currently 188,000, the highest since March 2024. For perspective, the 3-month average was -39,000 at the end of 2025, and across all of last year, payroll growth averaged a measly 10,000 per month (116,000 jobs created over the full year). What else would you call that other than re-acceleration?

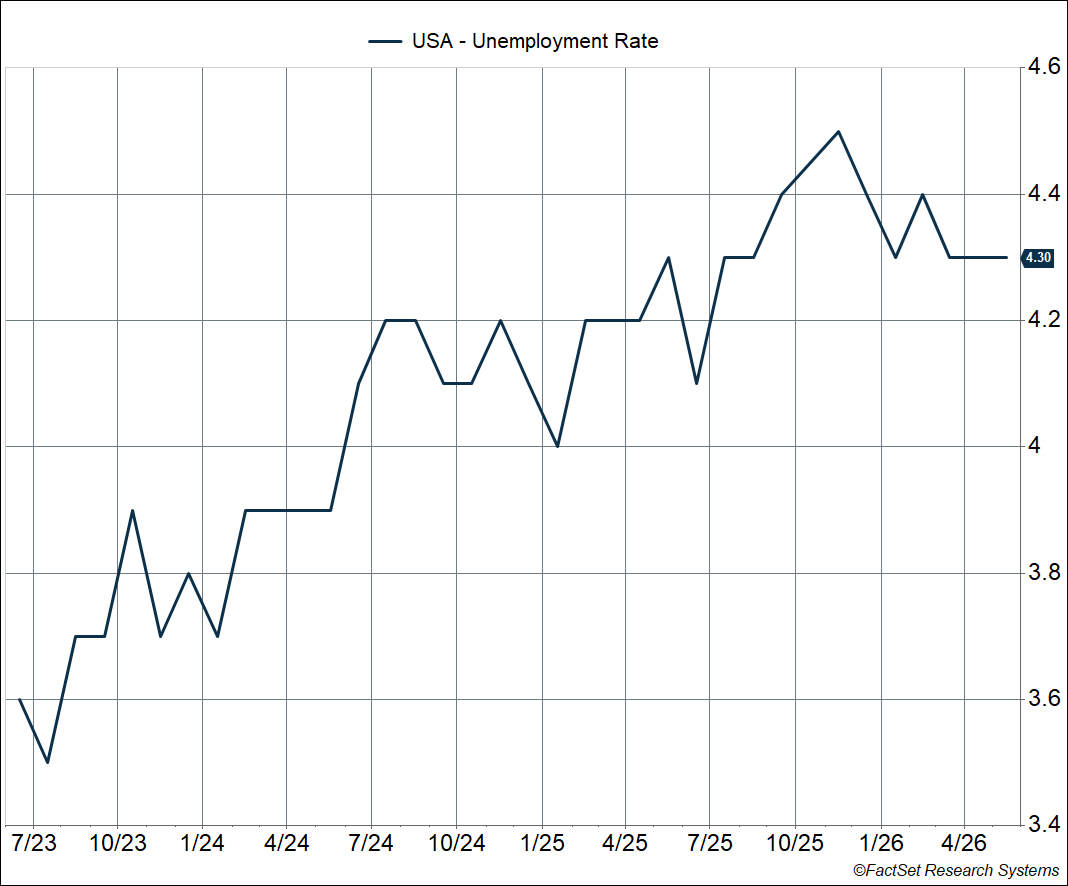

As I noted above, payroll growth can and has been revised a lot in recent years, and that’s why it’s useful to corroborate what’s happening with other data points. Notably, the unemployment rate comes from a household survey (payroll growth numbers come from a business survey). Well, the unemployment rate is sitting near historical lows at 4.3%. This shouldn’t be a huge surprise, given that payroll growth is clearly outrunning population growth (especially with immigration pulling back). There’s no question that the labor market was weakening last year, with the unemployment rate rising from 4% to 4.5 between January and November, but we’ve clearly turned the corner now.

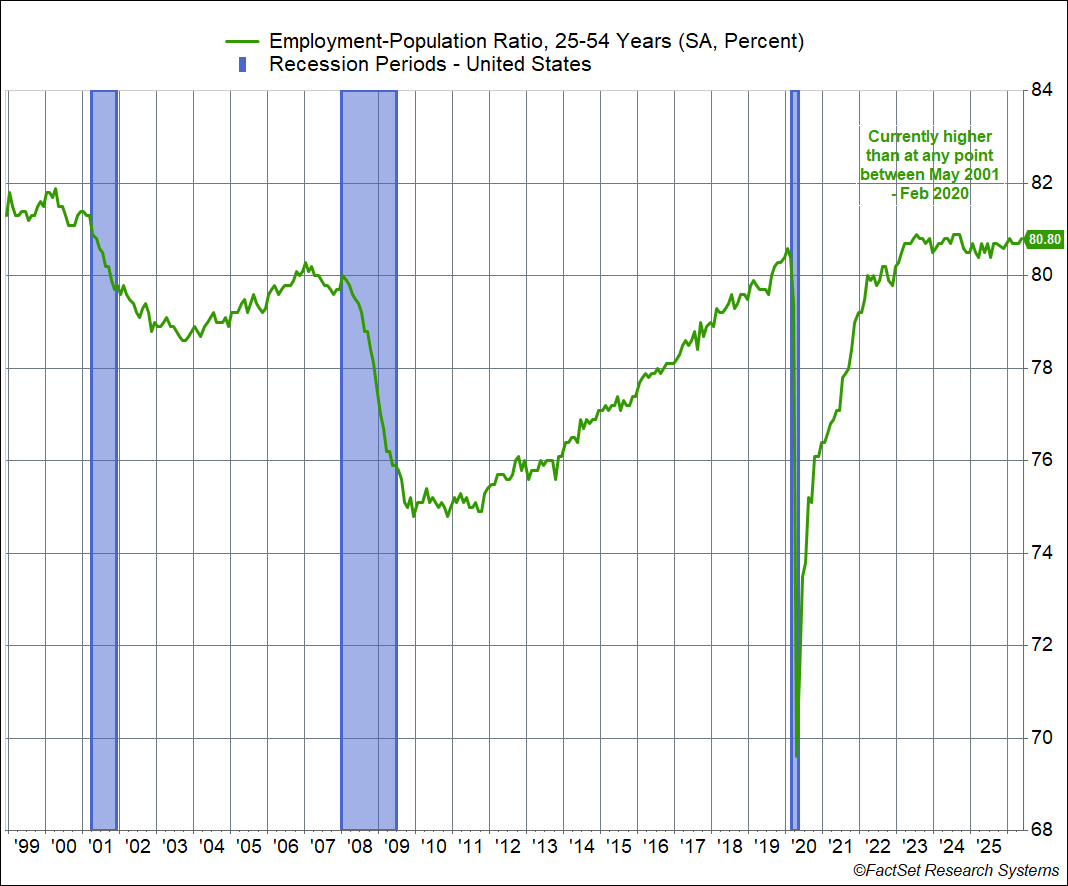

Better yet, the prime age (25-54) employment-population ratio rose to 80.8%, just shy of this cycle’s peak of 80.9% and higher than at any point between May 2001 and March 2023. In other words, more people in their prime working age years are employed today than at any point during the last two expansion cycles (relative to the age group’s population).

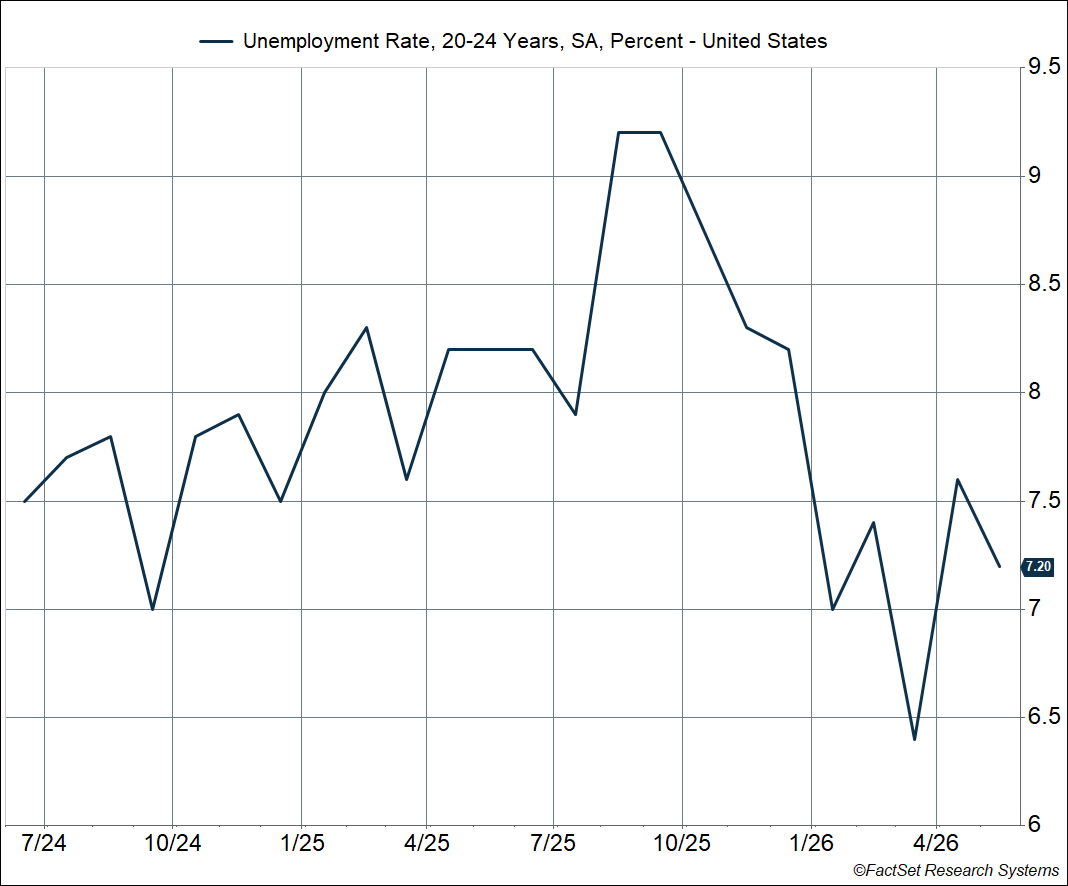

The prime-age employment-population ratio is useful because it gets around the fact that we have an aging population (so more people leave the labor force every day), and definitions around who is actually counted as “unemployed” – an unemployed worker who is “actively” looking for a job is counted as unemployed, but not someone who has given up after months of searching. The fact that the prime-age employment-population ratio is as high as it is goes against the prevailing narrative that “AI is taking away jobs.” That’s not even the case for young people, whose job prospects AI would have a greater (adverse) impact on. Yet, for 20-24 year olds, the unemployment rate has fallen from 9.2% last September to 7.2% in May, even as the AI-wave has grown.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Better Employment Breadth

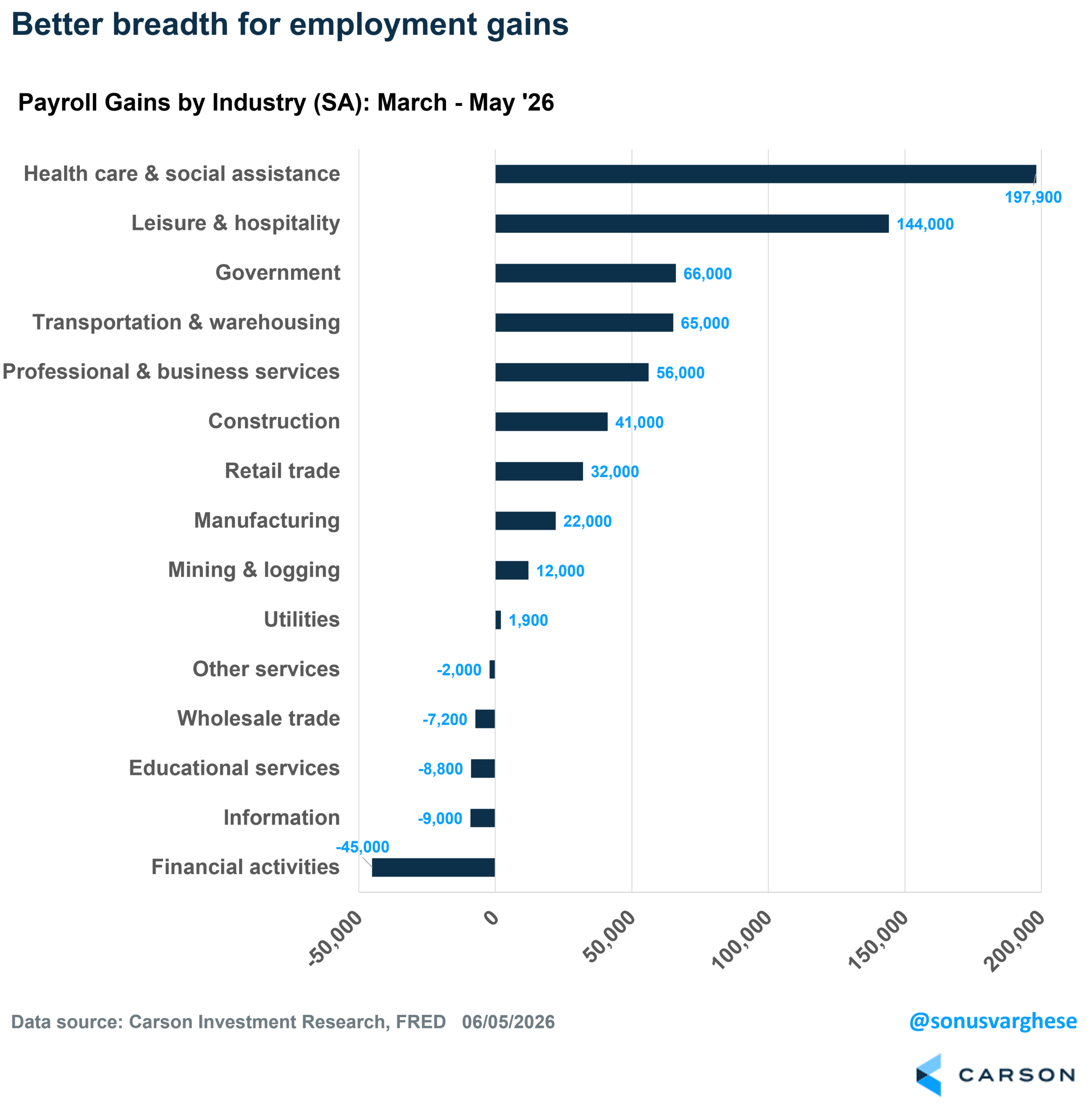

Things are even looking better under the hood. Over the past few years, employment gains within the health care sector have dominated job growth, while more cyclical areas of the economy lagged. This was especially the case in 2025, but that’s changed recently.

Over the past three months, payrolls have grown by 565,000. Health care payroll growth remains dominant, accounting for 35% of total payroll growth (198,000 jobs). But several cyclical areas are also showing up well, including leisure and hospitality (+144,000), transportation and warehousing (+65,000), professional and business services (+56,000), construction (+41,000), and even manufacturing (+22,000). The rebound in manufacturing is welcome, especially since manufacturing payrolls fell by 88,000 between February 2025 and February 2026.

One prominent area where job growth is lagging is the tech industry. Payrolls across the telecommunications and data processing/histing/related services industry have fallen by about 40,000 over the last year and have been flat recently. However, rather than AI replacing workers, it’s more likely a result of companies laying off workers to free up capital budgets for AI-related infrastructure.

The Fed is Fiddling While Inflation Burns

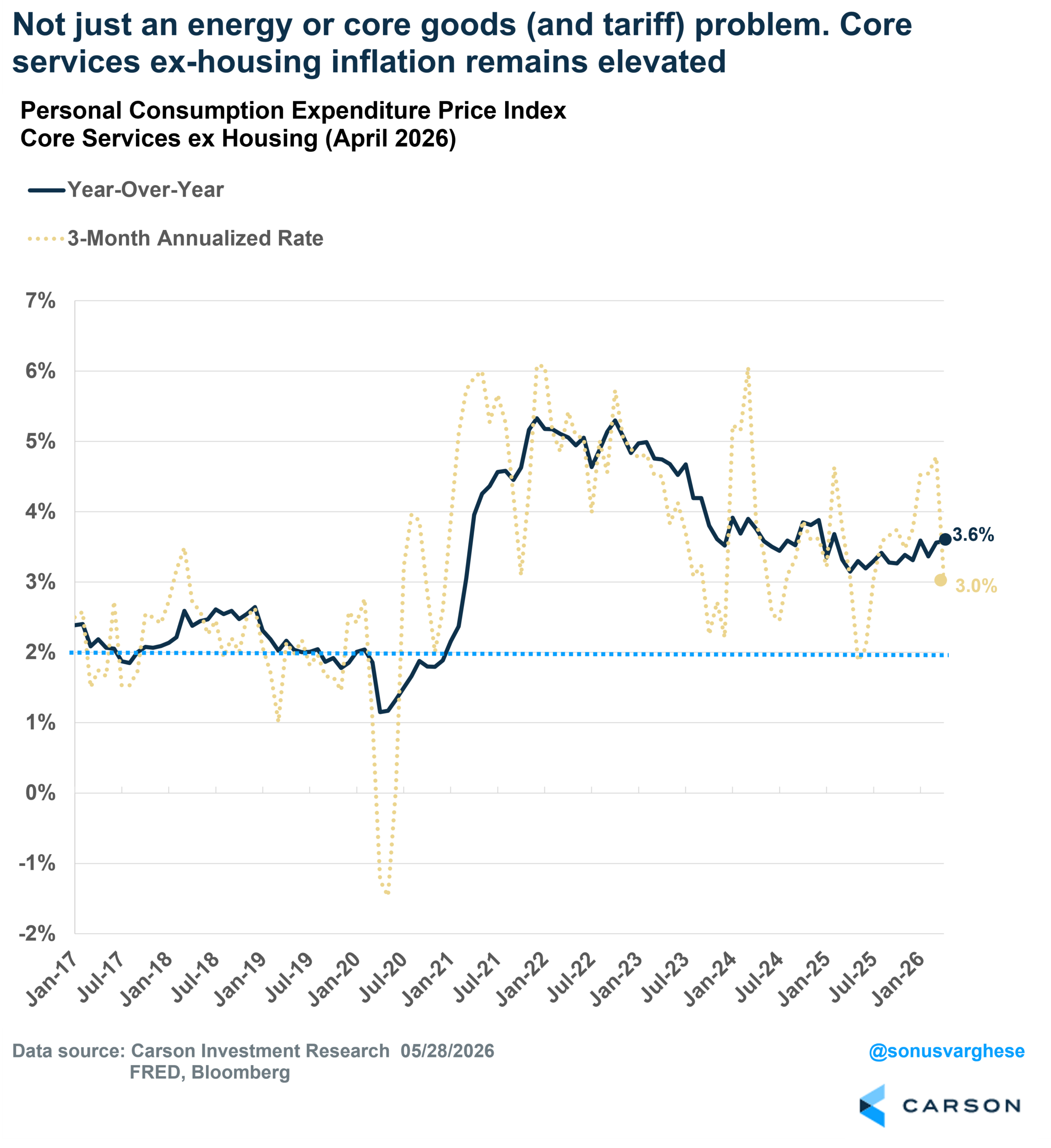

The labor market looks strong right now, and inflation is heating up. As I’ve been pointing out for several months now, this is not just an energy problem because the Strait of Hormuz remains shut. The fact that the Strait remains shut is certainly a problem, and it’s going to feed into non-energy inflation as well, via higher food prices and transportation costs. But we’re also seeing elevated inflation due to AI-related bottlenecks, tariffs, and even core services (ex housing) inflation. The personal consumption expenditures (PCE) index for core services is up 3.6% from last year and running at a 3% annualized pace over the last three months (through April). For perspective, the pace was just 2.2% in 2018-2019. The fact that services inflation is running hot has been a sign that the labor market is in better shape than headline numbers suggested up until a few months ago, i.e., there wouldn’t be upward price pressure on services if wage growth was weak and people were losing their jobs.

The fact that inflation is running hot and rising, while the Fed keeps interest rates unchanged, to me means policy is getting loose. Normally, a backdrop of a relatively healthy labor market and elevated (and rising) inflation would have the Fed thinking about rate hikes. Instead, it looks like the Fed, especially under incoming Chair Kevin Warsh, will look past elevated inflation.

For now, an easier monetary policy is good news for the stock market. However, the problem grows behind the scenes. At some point, whether it’s a year from now or 2-3 years from now, the Fed may realize that inflation has run too high for too long and will have to be even more aggressive to get inflation back to target. Policy rates should probably be about 0.5% to 1.0% higher than they are now. To be clear, the inflation problem can hardly be laid at the Fed’s feet. The fiscal deficit is running around 6% of GDP, well above anything we’ve seen this deep into an economic expansion – usually as expansions wear on, the deficit gets smaller, but the opposite is happening now. With Congress and the administration asleep at the wheel, the job lands at the Fed to pull things back. But it doesn’t look like a Warsh-led Fed is ready to tackle it; instead, it wants to move the inflation goalposts (including removing “outliers”) to keep policy easy and run things hot.

In my opinion, there’s clearly a cost, in the form of higher inflation and higher bond yields (which add to the federal government’s interest burden). Higher inflation means real (inflation-adjusted) wage growth is falling. Higher bond yields translate to higher borrowing costs across the economy, including higher mortgage rates, and that’s shutting out an entire cohort of millennials from the housing market. Keep in mind that housing has historically been the primary vehicle for building wealth for middle-income households, but the entryway is now blocked.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8964278.1. – 5JUNE26A