The December payroll report was yet another upside surprise as far as employment data go. Monthly payrolls rose by 223,000, above expectations for a 200,000 gain. The unemployment rate was expected to remain at 3.7% but fell to 3.5% – tying for the lowest rate since the 1950s. This is not remotely indicative of an impending recession. However, what matters for markets is how Federal Reserve (Fed) officials react to the strong employment data.

As inflation falls, much focus is going to be on the employment picture since this is what is going to matter for the Fed. Especially since they are focused on wage growth being a driver of underlying inflation, i.e., services ex housing, as Chair Powell noted after the December FOMC meeting. In their minds, a softer employment picture is required for inflation to get close to its target of 2% and remain there. If not, they are going to need to see a significant and persistent decline in price data to be convinced that inflation is heading the right way. Only then are we likely to start seeing rate cuts.

The “problem” is that a slew of recent data suggests the labor market remains far from soft. Let’s walk through four key data points.

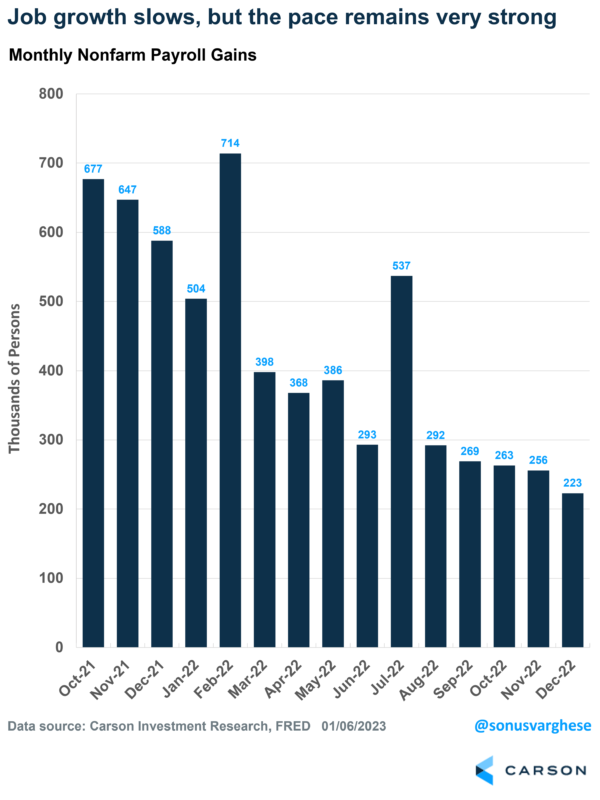

- Strong job growth

Job growth has slowed from more than half a million at the beginning of 2022 to just under 250,000 over the last three months of 2022. But make no mistake, this is still a very strong pace of job growth. As Powell has noted, the economy needs to create about 100,000 jobs a month to keep up with population growth. And we’re more than double that currently.

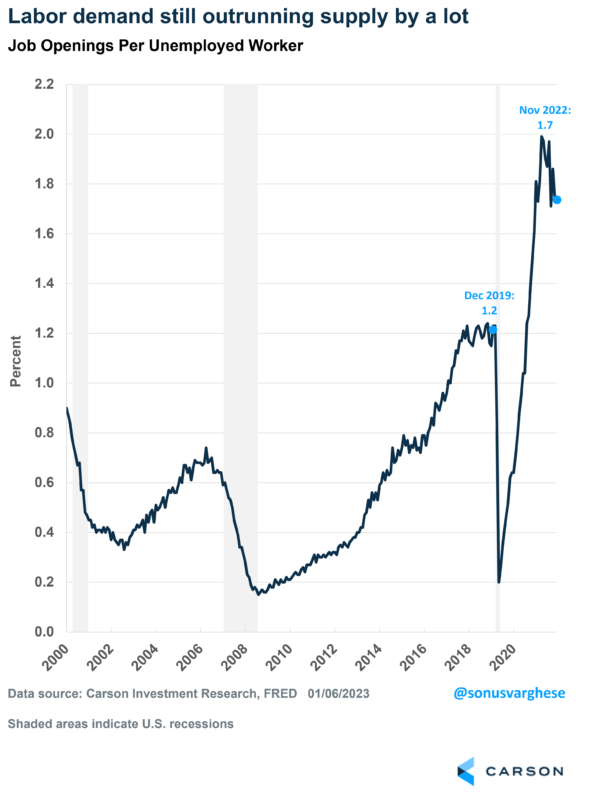

- Labor demand still out-running supply

Earlier this week, we got the November JOLTS data (Job Openings and Labor Turnover Survey), which showed that job openings remain elevated at 10.5 million. It was around 7 million before the pandemic. Powell’s favored metric is the vacancy ratio, which is the ratio of job openings to unemployed workers – that is currently at 1.7, down from 2.0 a few months ago but well above the pre-pandemic level of 1.2.

- Elevated Quits

The JOLTS data also showed that the rate at which workers voluntarily leave their jobs, i.e., the “quit rate,” remains elevated. For private sector workers, the quit rate had been declining over the past six months, but it rose to 3% in November, which is well above the pre-pandemic rate of 2.5-2.6%. This indicates that workers are confident enough to quit their jobs; often for jobs with greater pay – driving up wage growth. The Atlanta Federal Reserve finds that “job switchers” have seen much faster wage growth than “job stayers.”

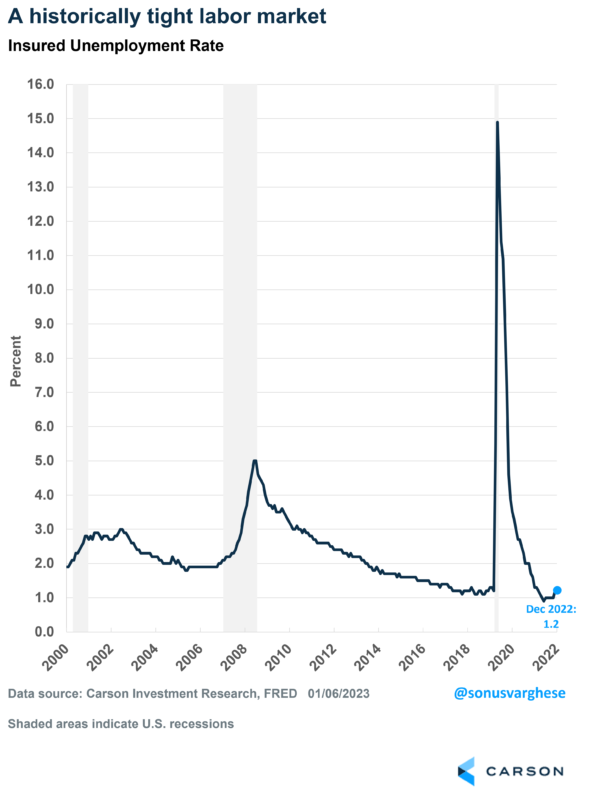

- Low level of layoffs

Initial claims for unemployment benefits, which is a leading employment indicator, closed out 2022 at 204,000 – the lowest level since September and a sign that layoffs remain low. Meanwhile, continued claims, which represent the number of unemployed workers who continue to receive benefits, remain steady at around 1.7 million. It has trended higher in recent months, indicating that unemployed workers are finding it a little harder to land a job as hiring slows, but the recent data don’t suggest anything alarming. In fact, the insured unemployment rate is at 1.2%, close to a record low. This measures the number of people currently receiving unemployment insurance benefits as a percentage of the labor force. It is a more useful and timely measure, as there is an observed action, i.e., filing for unemployment benefits, associated with being among the insured unemployed.

All the above points to a hot job market. Which is great by itself but not what the Fed wants to see. In short, it means the Fed is likely to keep rates higher for longer.

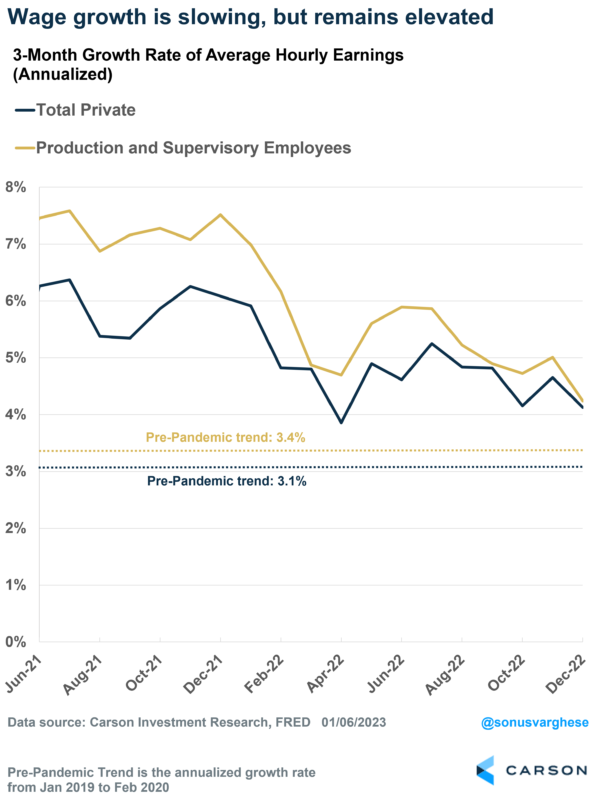

But wage growth is easing

Here’s what is strange but certainly good news: Wage growth is showing signs of declining momentum even as the employment picture remains strong.

Average hourly earnings for private workers rose at an annualized pace of 3.4% in December, which is only slightly above the pre-pandemic pace of 3.1%. For “production or non-supervisory employees,” wage growth registered just 2.6%, well below the pre-pandemic pace of 3.4%. Non-managerial workers earn less income and tend to spend a greater portion of their income – faster wage growth for this group can potentially put upward pressure on prices. Monthly numbers can be noisy, but even the 3-month wage growth numbers clearly show declining momentum for all workers and for non-managerial workers. We’re yet to get to the pre-pandemic pace, but the trend is positive.

Ultimately, the “Goldilocks” scenario is this:

- Strong employment growth

- Wage growth eases

- Inflation falls

This is not what “theory” says should happen, but it is exactly what we’ve seen recently. We’ll take it. And if it continues, we believe it’ll only be a matter of time before the Fed takes notice.