The S&P 500 and Nasdaq hit new all-time highs last week, and as our friend Sam Ro wrote on his substack (T’ker), this isn’t sitting well with many people. There’s also a steady stream of commentary along the lines of “this doesn’t make sense” and “risk assets are detached from reality.” Or that markets are looking past the crisis. As Sam writes, markets aren’t “ignoring anything.” They’re focused on what matters: profits.

The S&P 500 is now up 4.5% year to date (as of April 17), including dividends. That’s entirely on the back of rising profit growth estimates. Let’s unpack this.

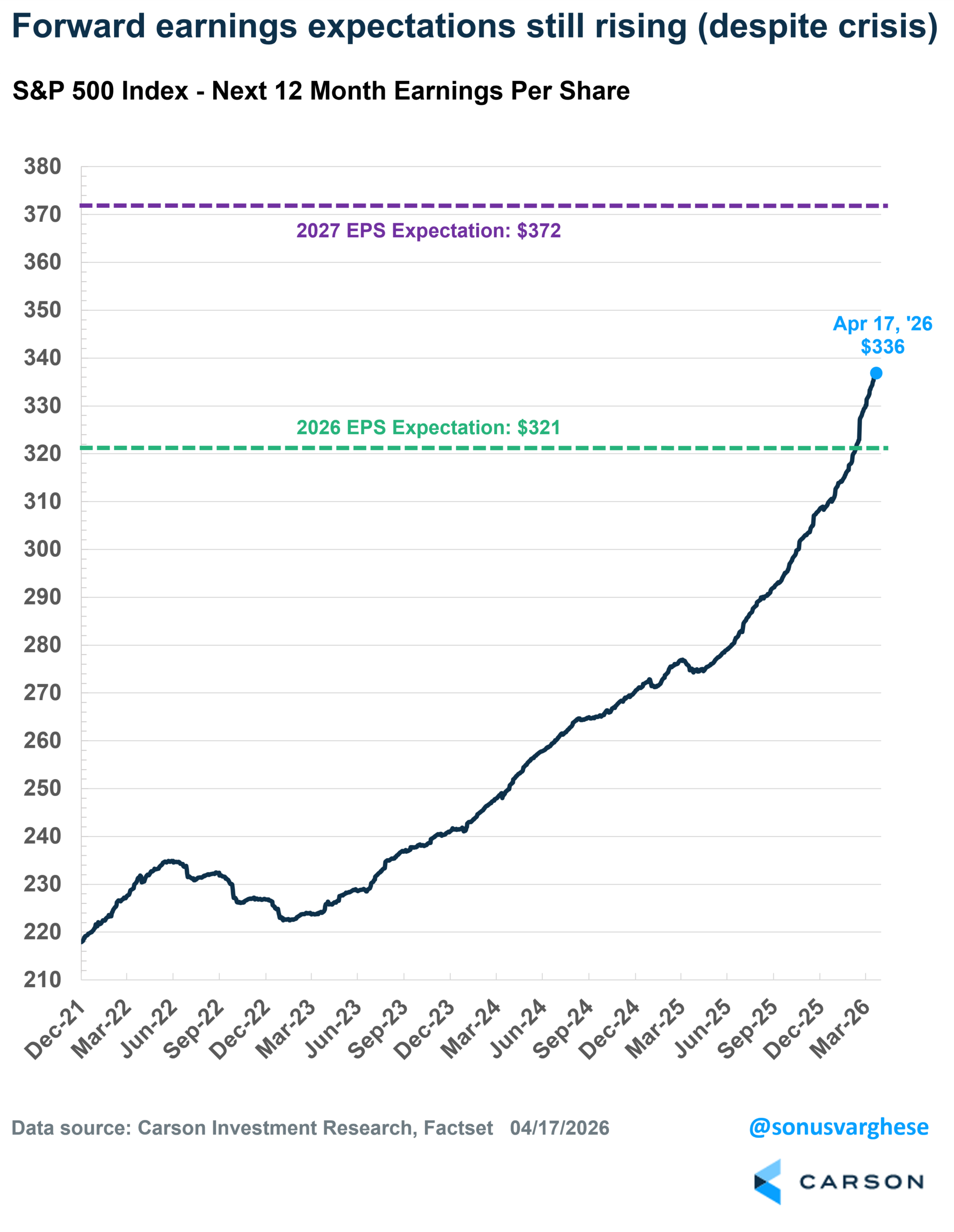

The S&P 500’s next 12-month earnings per share (NTM EPS) is currently $336/share, up 9% since the end of last year and 5.8% over the past seven weeks (since the crisis began). In other words, almost two-thirds of the gain in NTM EPS has come while the crisis was raging on.

Keep in mind that the NTM EPS is now mostly about 2026 EPS expectations. Almost 2/3 of NTM EPS is expected EPS for 2026 ($321) and 1/3 expected EPS for 2027 ($372). At the end of the year, the NTM estimate will match the 2027 estimate exactly. As 2026 gets underway, NTM EPS should continue rising, as it incorporates more of 2027 EPS expectation (as long as 2027 EPS doesn’t fall significantly). In other words, we’re looking at yet another year of strong EPS growth. Right now, the expectation is that 2027 EPS will be 16% higher than 2026 EPS.

We can separate the S&P 500’s return into contributions from:

- Earnings growth

- Multiple change (change in the price-to-earnings ratio, a proxy for what investors are willing to pay for earnings)

- Dividends

The S&P 500’s year-to-date return of 4.5% came from:

- Earnings growth contribution: +8.7%-points

- Multiple growth contribution: -4.6%-points

- Dividends: +0.4%-points

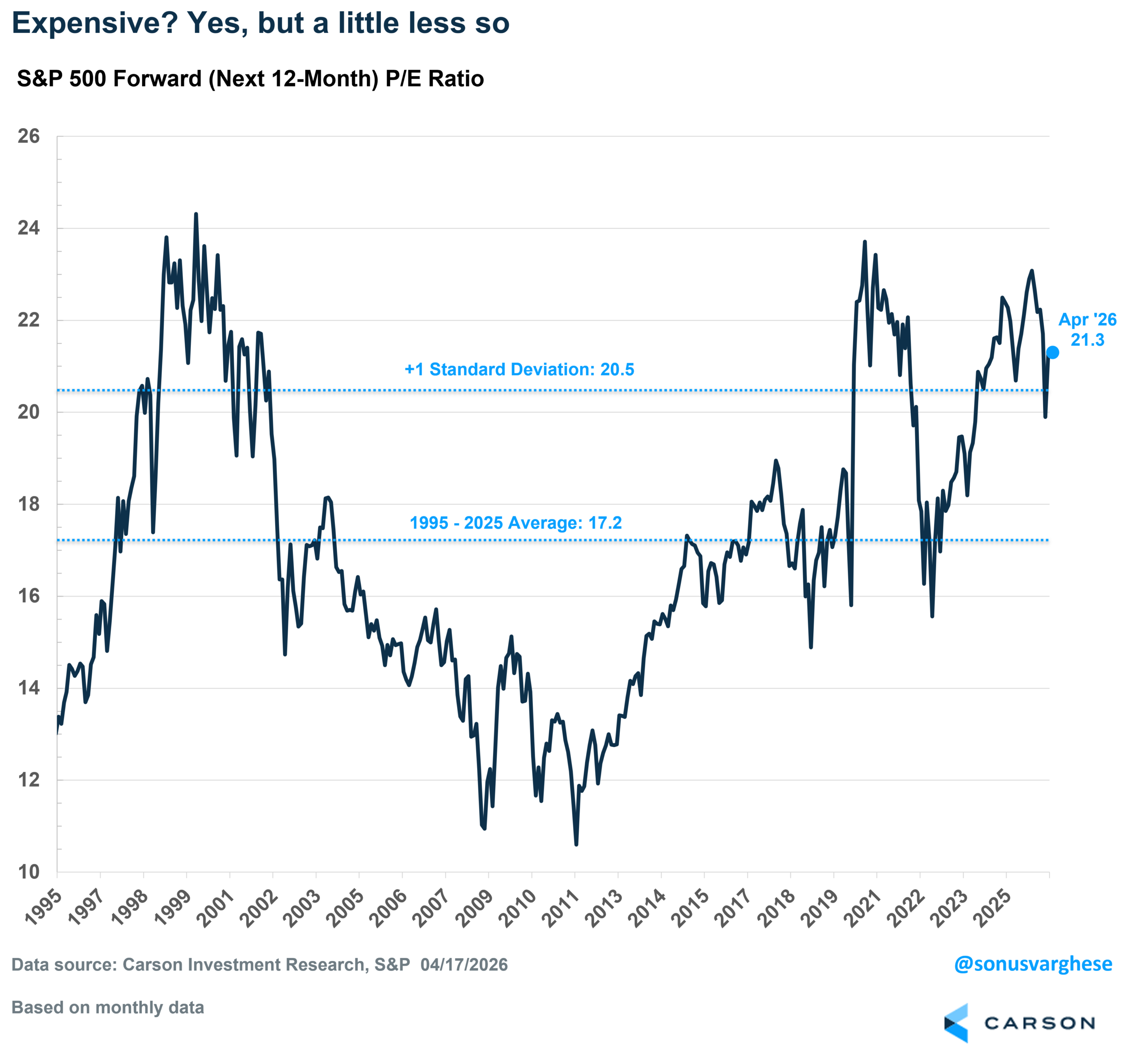

In short, the year-to-date return is almost entirely on the back of rising profit expectations, which have more than offset multiple contractions. The forward P/E is now at 21.3x, down from 22.2x at the end of 2025. At the pre-crisis all-time high (January 27), the forward P/E was 22.5x, and back in October of last year, the forward P/E had gotten as high as 23.5x. At the lowest point of the recent pullback (March 30), the forward P/E had fallen as low as 19.3x.

All this to say, the index is at new record highs, but multiples are lower now than they were a few months ago. Usually, as earnings expectations rise, you tend to see more optimism and valuations rise. But that’s not happened recently, and the big reason is that real rates have jumped recently as investors priced in a less dovish Fed amid higher inflation.

A Closer Look at Profit Growth

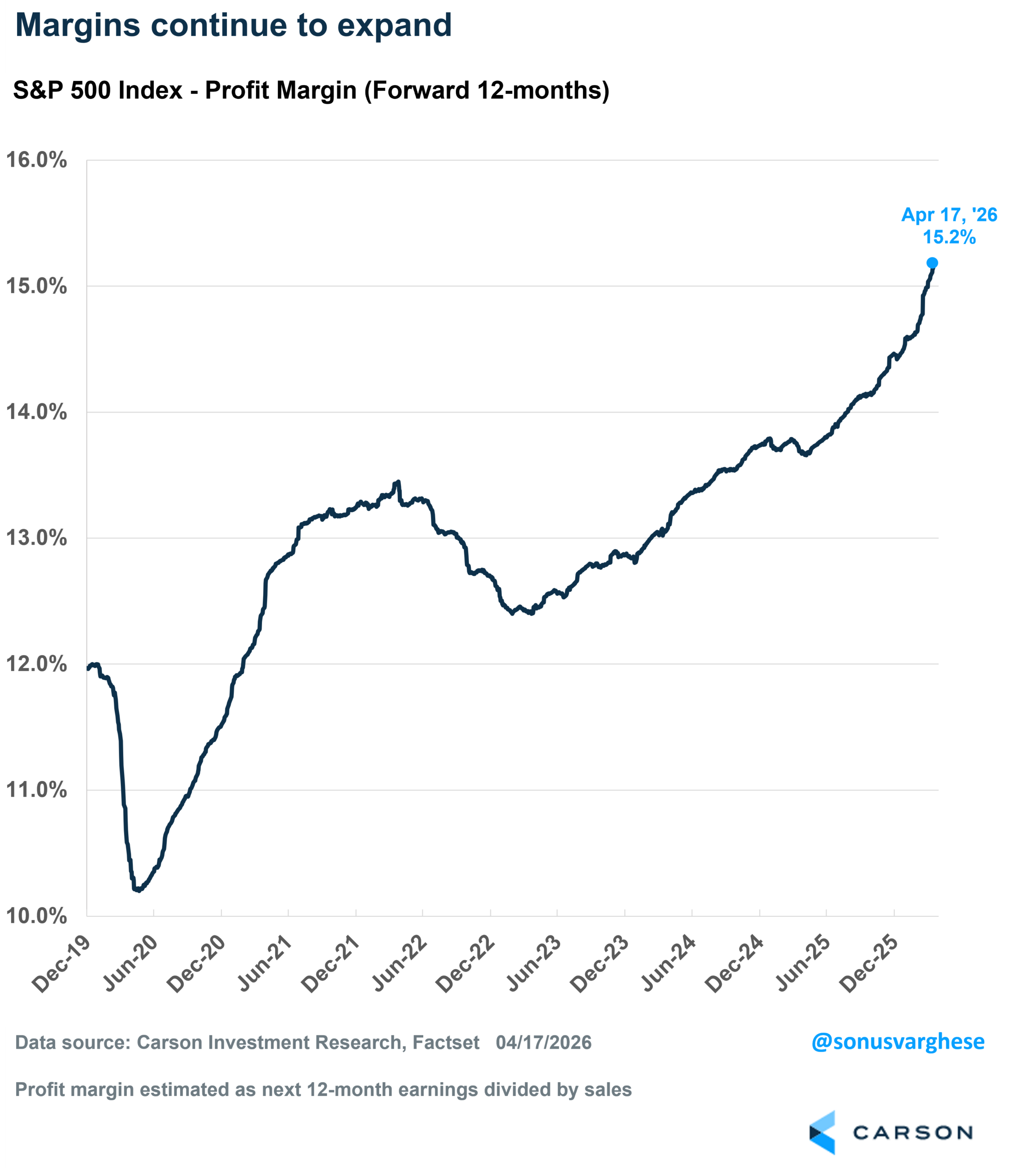

Profit growth can be separated into two pieces: sales growth and margin expansion. Sales growth is closely tied to nominal GDP growth, and as long as we don’t have a recession sales growth should run fairly strong. This was the case even in 2022, when sales growth was strong (+8.5%) as nominal GDP growth clocked in around 8% for the year. But EPS growth was weak in 2022 (+3.8%) because of a pullback in margins amid surging interest rates.

However, margins have expanded a lot over the last three years. Forward margins were around 12% at the end of 2019 and had expanded to 12.7% by the end of 2022. Margins sat at 14.5% by the end of 2025, a new all-time high. And they’ve expanded to 15.2% this year.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

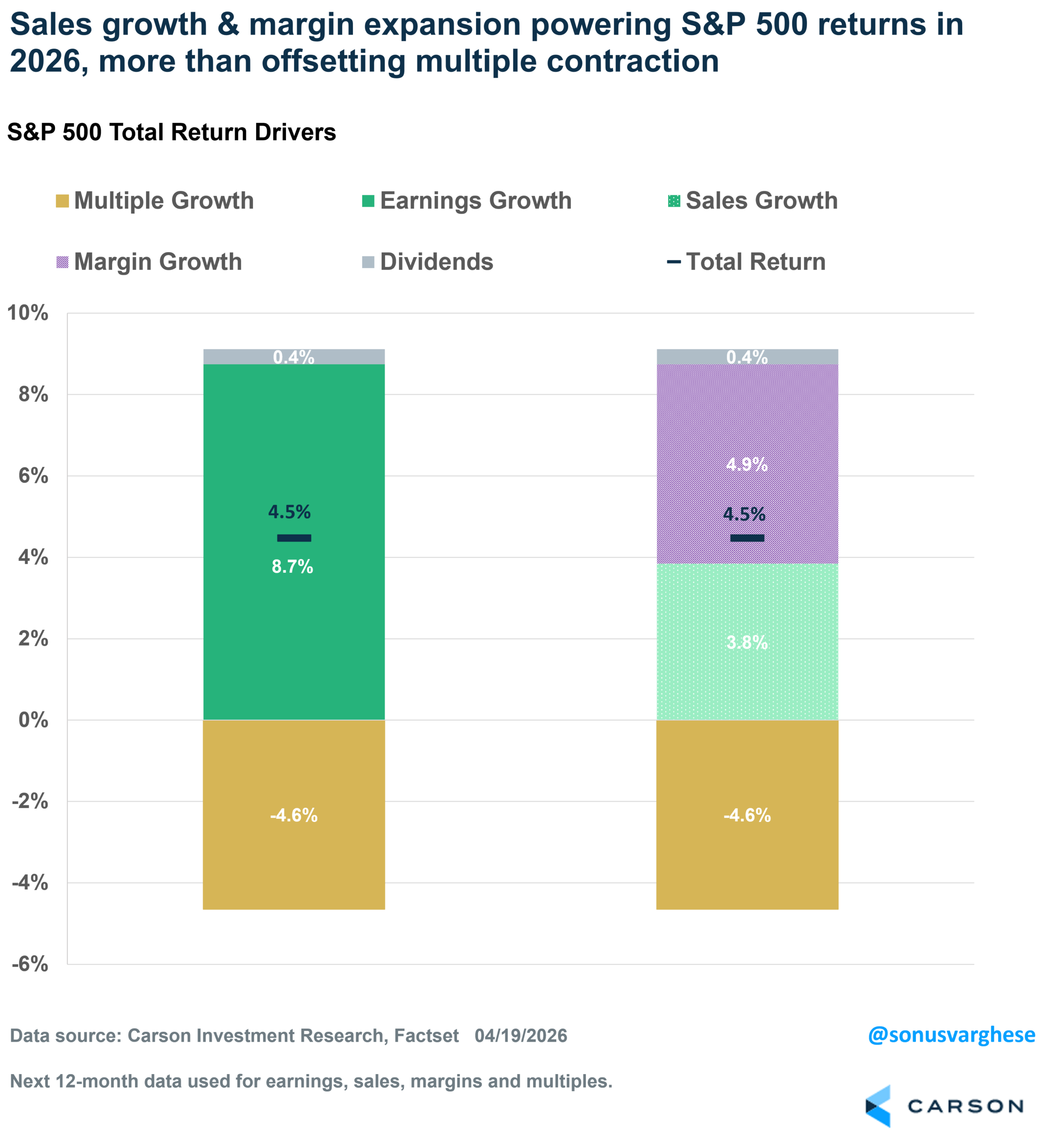

Here’s a look at how this has actually helped S&P 500 returns year to date. I break down EPS growth into sales and margins. As I noted above, the S&P 500 is down 6.7% year to date. Here are the contributions:

- Earnings growth: +8.7%-points

- Sales growth: +3.8%-points

- Margin expansion: +4.9%-points

- Multiple growth: -4.6%-points

- Dividends: +0.4%-points

In short, profit margin expansion (expected) is the biggest driver of profit growth so far in 2026, even more so than sales growth expectations.

In fact, the above chart showing return drivers for the S&P 500 explains what’s happened this year, and why the index is at an all-time high despite a major crisis in the Middle East.

- The primary driver of the year-to-date return is margin expansion, but the other side of this is inflation.

- Sales growth is strong on the back of strong nominal GDP growth (5-6%), but that’s on the back of inflation rather than real GDP growth (which is likely to run ~ 2%, below trend for a second straight year).

- Multiple contractions have been a drag on returns, as markets price in fewer rate cuts and a relatively less dovish Fed amid higher inflation.

A Profit Margin Expansion Story Is Also an Inflation Story

Too many commentators are making the mistake of translating an inflation surge into weaker real consumption, and hence weaker economic growth and profit growth. But as we can see, inflation also means margins are rising, and that’s driving profit expectations higher. This becomes clearer if we look at individual sectors.

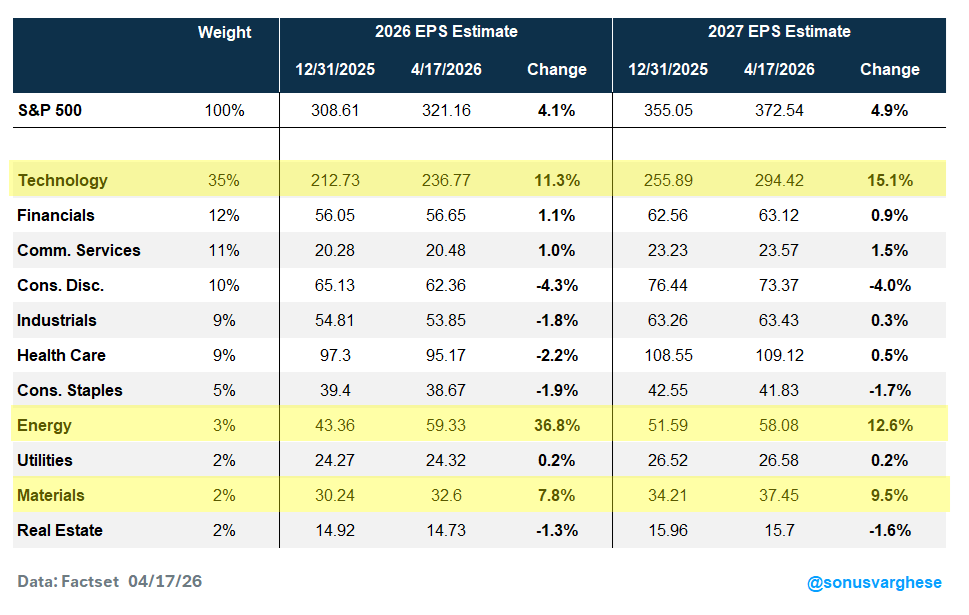

The S&P 500’s 2026 EPS expectation has risen over 4% since the start of the year, from $309 to $321. The 2027 EPS expectation has jumped even more, rising almost 5% from $355 to $373.

A breakdown of the 11 S&P 500 sectors shows exactly which sectors are boosting the aggregate index’s profit (EPS) expectations. From the start of the year through April 17:

- The tech sector has seen 2026 EPS expectations grow by 11% and 2027 EPS grow by 15%.

- Energy has seen 2026 EPS expectations grow by 37% and 2027 EPS by 13%.

- Materials has seen 2026 EPS expectations grow by 8% and 2027 EPS by almost 10%.

The remaining sectors haven’t seen EPS estimates pull back in a significant way, including for sectors like consumer discretionary, industrials, health care, and consumer staples, which would be hit by higher input prices.

This is not to say it’s all “predatory pricing.” A lot of these firms are in the right place at the right time, whether it’s chip manufacturers (in the US or even in South Korea and Taiwan) or energy companies. As John Maynard Keynes said:

“Profiteers are a consequence, not a cause of rising prices.”

In any case, the ultimate beneficiary: stock prices (and investors), as long as the Fed continues to view yet another inflationary episode as transitory (although bond yields haven’t moved all the way back to pre-crisis levels, reflecting inflation concerns).

The good news is that we have a dovish tailwind in the form of a Fed that is likely to look the other way on inflation. For a moment there, markets had taken out the possibility of any rate cuts this year amid renewed inflation concerns, but over the last week, markets are once again pricing in a higher probability of at least one cut (about 40%).

As I’ve highlighted in recent weeks and months, inflation remains elevated even outside of energy, and the Fed had a problem even prior to the Middle East crisis. In fact, the Fed holding rates steady would imply policy is getting looser as inflation picks up, setting aside any rate cuts in this environment. That would be a tailwind for stocks, at least until the Fed gets serious about inflation and lands in a situation where they’re forced to hike rates to such a degree that it not only curbs inflation but also kills the economy in the process. Surging policy rates would raise real rates and hit multiples hard, pulling the index lower.

For now, that’s not on the cards and hence the focus on potential upsides. At the same time, an inflationary regime means we must balance contrasting ideas in our heads, like the prospect of rising corporate profits even as inflation remains elevated. I spoke about this with the New York Times and the Wall Street Journal last week. The inflation picture confounds normal analysis of what the economy and companies are likely to do, and here it’s important to differentiate between real and nominal GDP growth. It’s the latter that matters for revenues and profits.

Ryan and I also discussed this on our latest Facts vs Feelings episode.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8890312.1. – 22APR26A