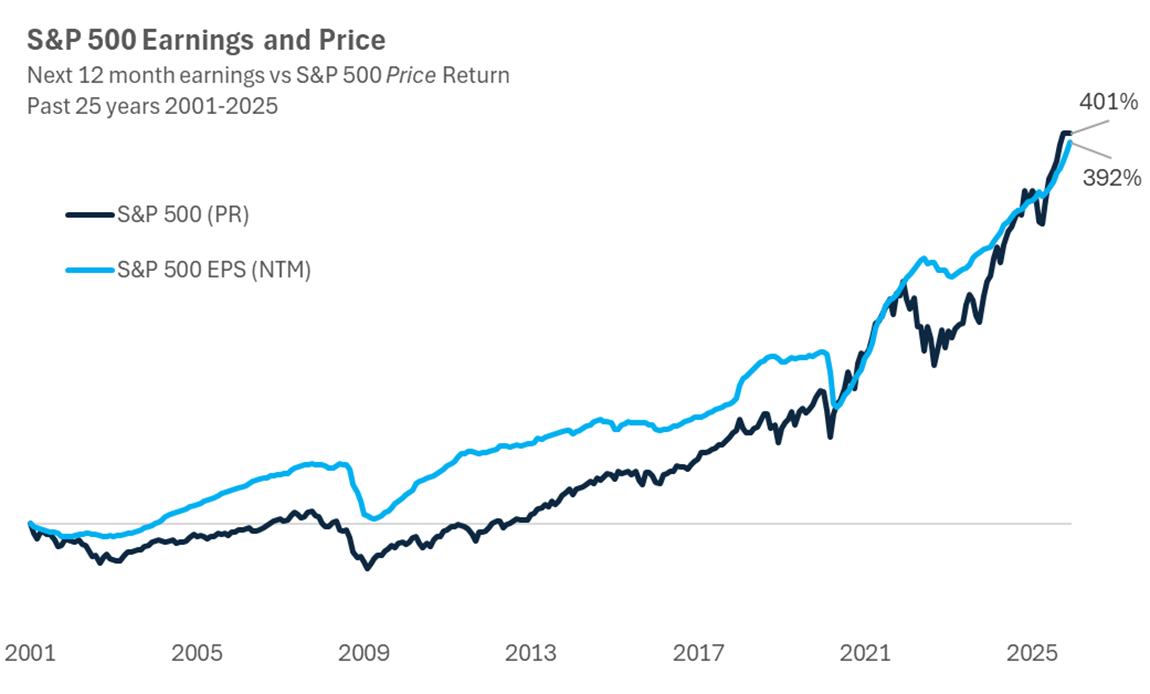

Wars, unemployment, the Fed…. Greenland — noise is and always will be abundant in financial markets. This noise isn’t all bad, and it’s our job to parse through it for you, but as we say time and time again, what really matters for stocks is earnings. Ultimately, a lot of factors affect earnings, but the trajectory of those earnings is the long-term driver of stock prices. The chart below illustrates this over the past 25 years. Forward-looking earnings (after all, the stock market is a discounting mechanism) track against market price returns closely. There are certainly ebbs and flows, times when the market gets ahead of itself and vice versa, but overall, the path of earnings and the path of stock prices align. We get to peer into corporate America every quarter, with financial results, but also rhetoric and corporate commentary that can be instructive.

Sources: Carson Investment Research, FactSet

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

We recently highlighted the strength in earnings the past couple of years and how investors should not be surprised with the strong gains we’ve seen. Let’s review this further for the earnings results we already have, and preview expectations for the final quarter of 2025 as we embark on earnings season.

Review – Q3

Earnings season for the 3rd quarter of 2025 wrapped up for the S&P 500 in mid-December, and the results were quite strong. Here are the numbers (according to Factset):

- 83% of companies beat earnings expectations, and 76% of companies beat revenue estimates.

- Earnings grew 13.6% y/y in Q3, and revenues grew 8.5%. Both numbers exceeded estimates by substantial margins.

- Tech companies grew earnings 29.2%, while Communication service company earnings fell -7.8%.

- S&P 500 companies with greater than 50% of revenues from overseas grew both earnings and sales faster than their more domestic-oriented counterparts.

- Profit margins have been the driver and supporter of continued earnings growth, total margins reached 13.1%, exceeding estimates. Financials, materials, and utilities companies saw the largest number of companies increasing margins for the quarter.

- Mag 7 earnings growth reliance continues to drop, with the other 493 contributing 9.1%-points of EPS growth.

Preview – Q4

We are just now starting to get a look at full fiscal year 2025 earnings. This week kicks off with a number of large banks reporting earnings. It is very early on, and so far those earnings have been mixed and overshadowed by calls for a 10% cap on credit card interest, affecting not just large financial institutions that issue credit cards but also companies like Delta whose revenue streams directly depend on the ability for credit to be extended broadly.

That being said, expectations for Q4 are very strong:

- The S&P 500 is expected to report 8.3% growth — a dip compared to recent quarters and projected future expectations, but still a very strong number and one that keeps rising.

- Revenues are expected to grow with similar strength at 7.7%, a number that has risen more than 1% since the prior quarter ended.

- Net profit margins are expected to drop slightly from the prior quarter down to 12.8%, but remain near record levels.

As always, we will be closely monitoring earnings reports in the coming weeks and months, as well as what CEOs and CFOs are mentioning about the local and global economy. Our team’s research framework that blends fundamental, economic, technical, valuation, and policy keeps us balanced, honest, and focused on the long-term while not ignoring the here and now.

For more content by Grant Engelbart, VP, Investment Strategist click here.

8715090.1. – 15JAN26A