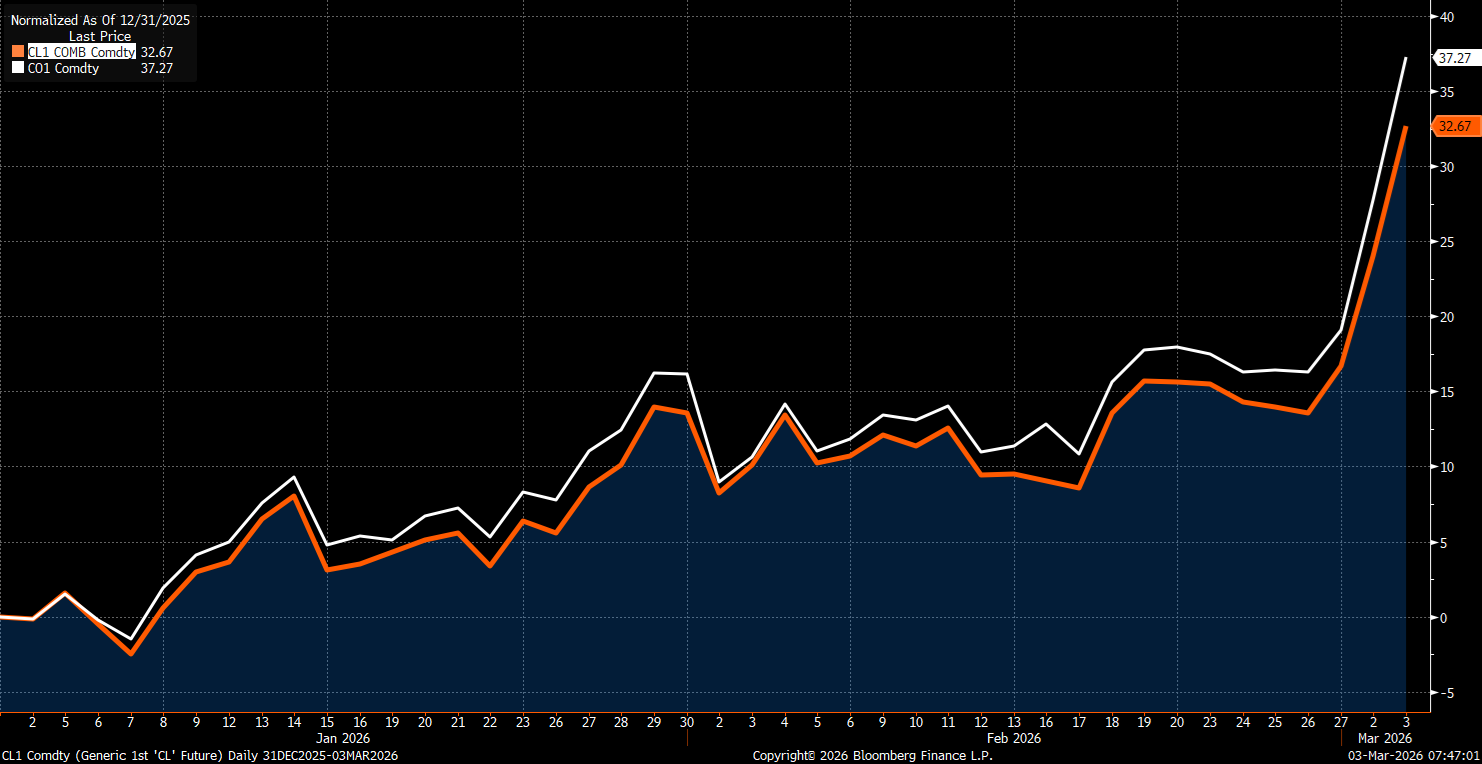

War tends to be inflationary, period. Especially one in the Middle East that drives up oil prices. Since Friday, WTI crude prices have risen over 10% to $76/barrel, while Brent prices rose over 15% to $83/barrel. That doesn’t sound like a lot given the magnitude of hostilities in the region, but as Ryan wrote in our prior blog, investors have been pricing in the possibility of conflict for a month now. Oil prices have risen sharply this year, and with Monday’s increase, WTI (orange line in the chart) is up 32.5% year-to-date and Brent (white line) is up 37%.

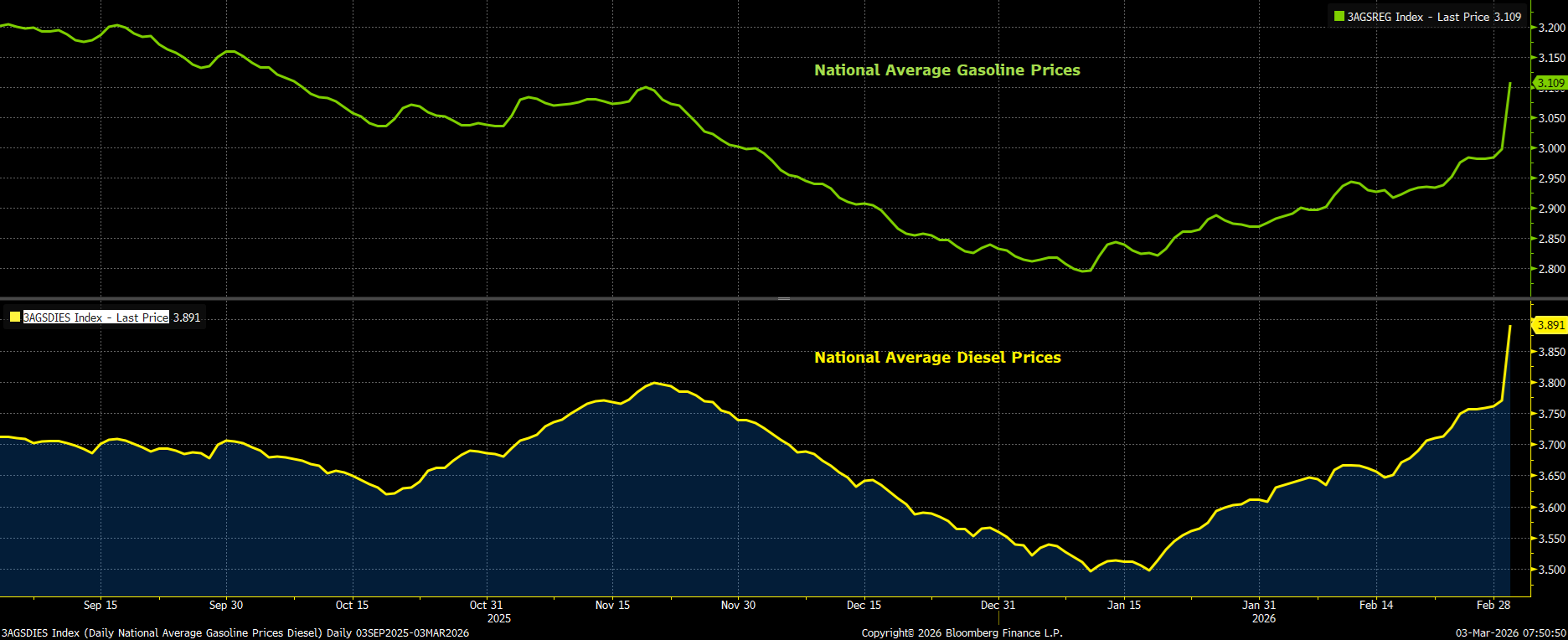

Surging oil prices led to the largest single-day increase in gasoline prices since March 4th, 2022. Average gasoline prices pierced the $3.0/gallon level once again, rising to $3.11/gallon, the highest since late November. Prices are likely to be headed toward $3.30/gallon if the conflict doesn’t end soon.

There’ll be pain on the trucking side as well, with diesel prices hitting $3.89/gallon, the highest since May 2024. Prices look set to climb towards $4.00/gallon. This may put upward pressure on food prices, as diesel is used to transport food.

On the topic of food, sugar prices worldwide rose on Monday, and a big reason is that the world’s largest standalone sugar refinery is in Dubai.

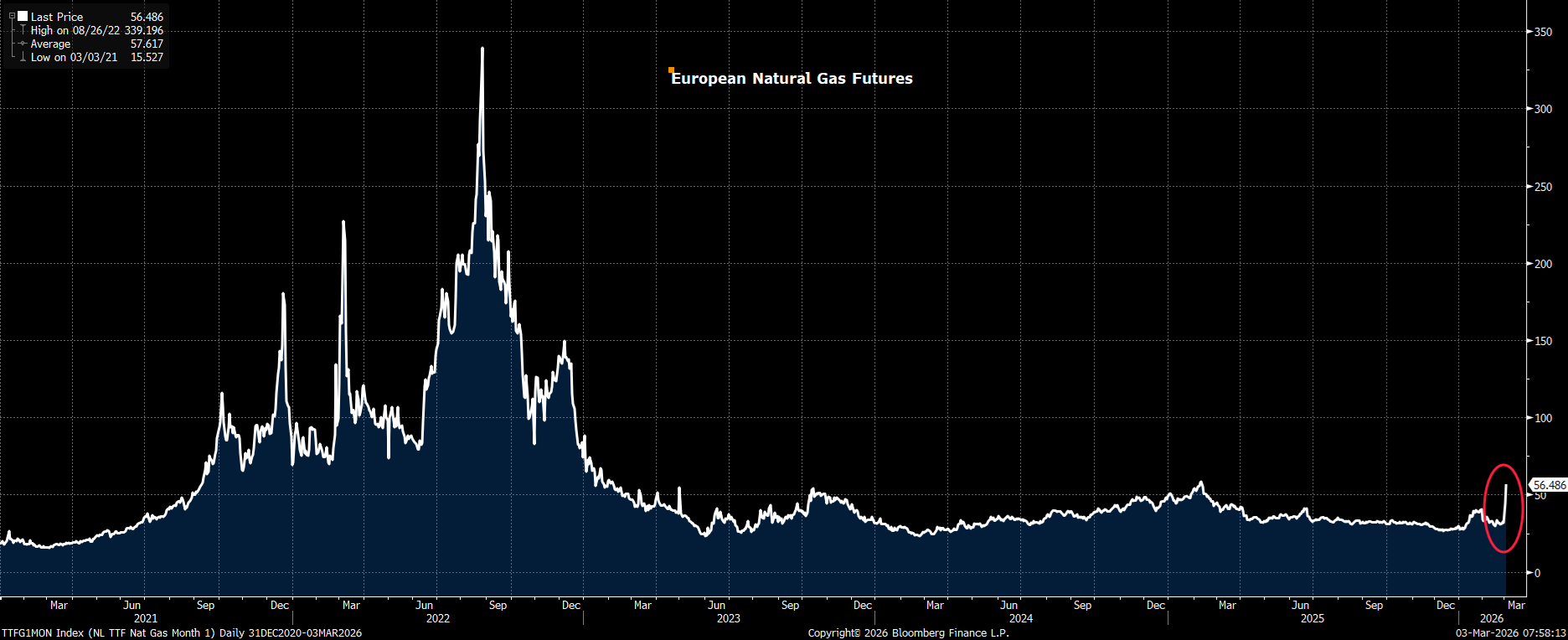

It’s not just the US that will be impacted. Asian countries such as India, China, and Japan import much of their oil from the Middle East. There’s also the problem of liquefied natural gas (LNG), of which Qatar is the second-largest producer. The country shut down LNG production at the world’s largest export facility, which covers about 20% of global LNG supply. That sent benchmark gas futures prices in Europe surging by over 75%, the biggest jump since Russia invaded Ukraine. For now, prices are well below the levels we saw in 2021-2022.

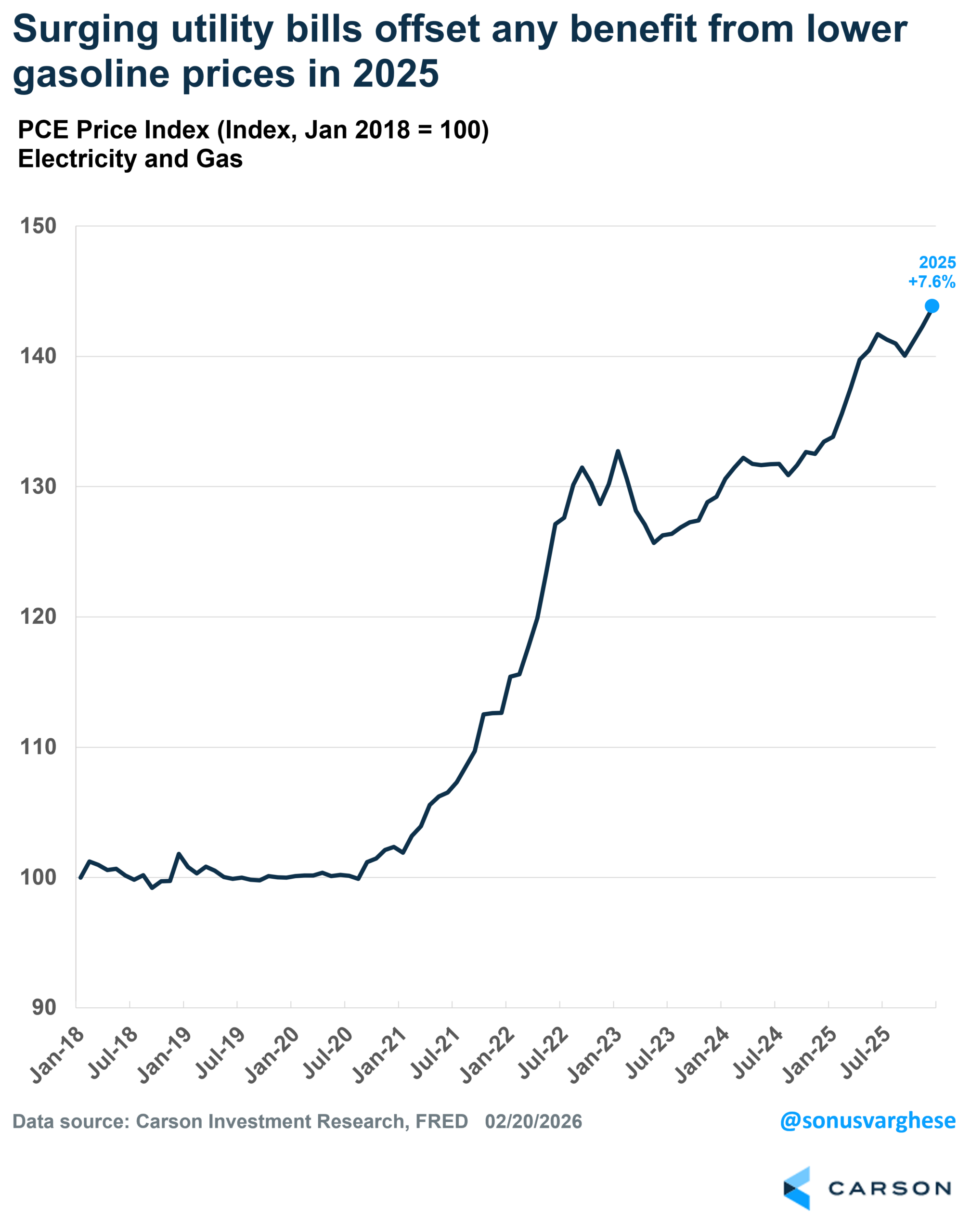

On the face of it, this would be a big positive for US LNG exporters, but that will also mean gas prices in the US (which are significantly lower than global prices now) could be pulled upward towards export prices if export capacity becomes a larger share of US production – potentially resulting in higher utility bills for US households. That’s on top of electricity bills that have risen significantly over the past year amid the vast buildout of AI-related datacenters (which shows no sign of slowing). Last year, the increase in utility bills offset any relief from lower gas prices.

All this translates to more inflationary pressure.

Of course, things could subside sooner rather than later if hostilities cease quickly. I’m not going to make a prediction on that – it doesn’t look like anyone has any idea what the endgame is here. However, the longer tankers remain stranded in the Persian Gulf, the longer it’ll take for prices to revert to last year’s levels.

Still, if it were just oil, we could probably set it aside as “transitory”.

It’s Not Just Price Pressure From Oil

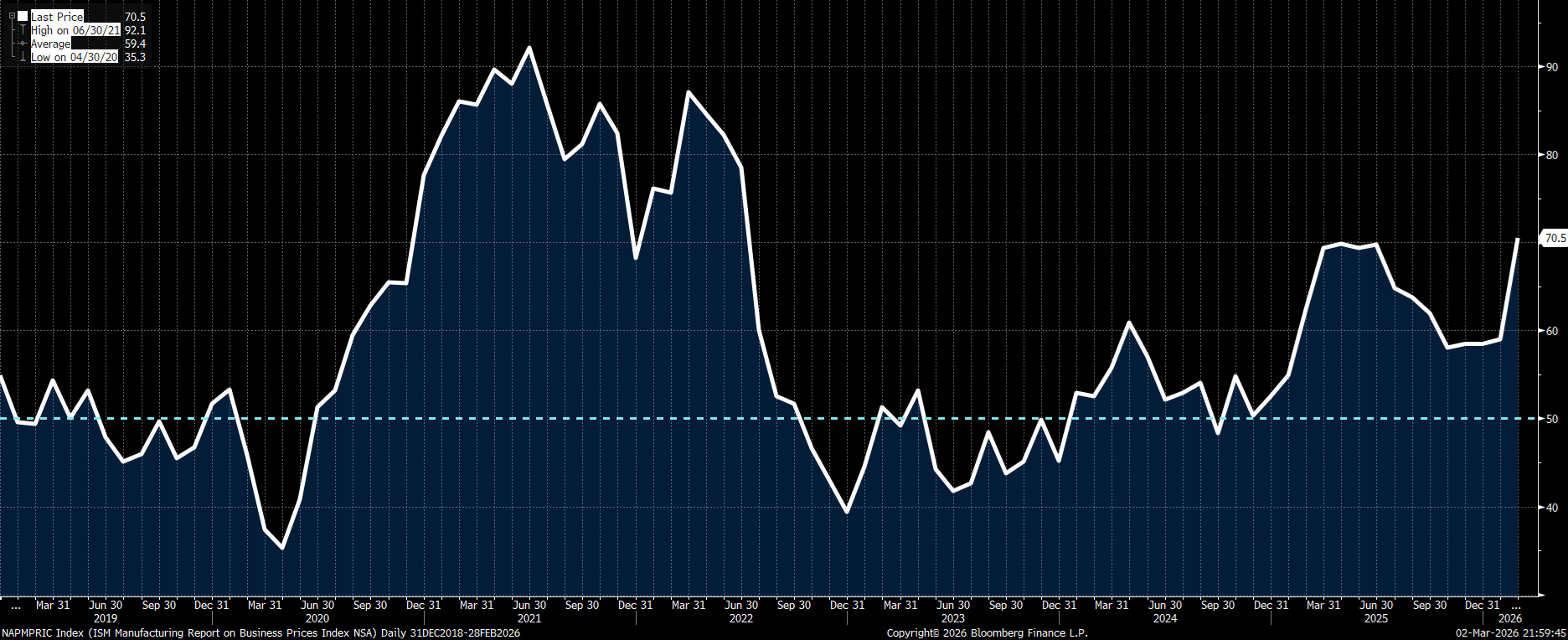

The ISM Manufacturing PMI for February had good news, showing the manufacturing sector expanding for the second consecutive month, with a reading of 52.4 (a 50+ reading indicates the sector is expanding). However, the bad news is that “prices” sub-index surged 11.5 points to 70.5, the highest reading since June 2022 (when inflation hit the highest level in 40+ years). Raw materials prices have now been rising for 17 straight months, driven by tariff-related increases in steel, aluminum, and many other imported goods.

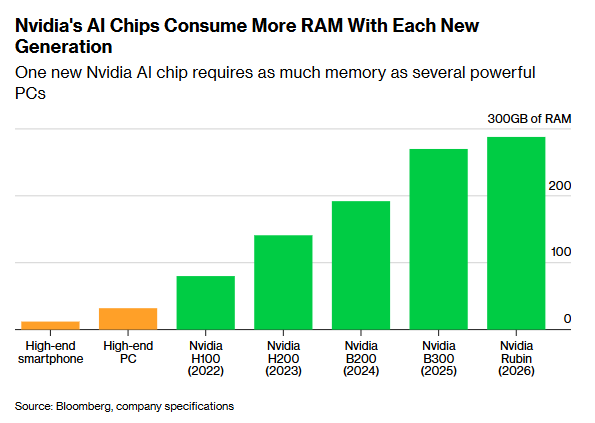

The ISM report also asks respondents which commodities are in short supply, and these caught the eye: electrical and electronic components, memory chips, and rare-earth components.

Memory chips are a particularly big concern here because of a shortage that can inflate prices for items like laptops, smartphones, gaming consoles, cars, and even data centers. Several companies, like Apple and Tesla, have said there’s a shortage of DRAM (Dynamic Random Access Memory), and that’s going to curb production (or reduce margins, for example, on iPhones).

The squeeze is mostly being driven by the buildout of AI data centers. Quoting from a recent Bloomberg article:

“Companies like Alphabet Inc. and OpenAI are gobbling up an increasing share of memory chip production — by buying millions of Nvidia Corp. AI accelerators that come with huge allotments of memory — to run their chatbots and other applications. That’s left consumer electronics producers fighting over a dwindling supply of chips from the likes of Samsung Electronics Co. and Micron.”

The cost of a particular type of DRAM surged 75% m/m in January. Every new NVIDIA chip requires more memory and several powerful PCs.

In short, costs are going up even as demand surges – this also tells you that AI demand is not slowing. In fact, the AI data center construction blitz is only set to accelerate this year, and actual building is yet to commence.

This is also helping companies like Samsung, Micron, and SK Hynix. There’s a reason the South Korean stock market is on fire: the MSCI South Korea index is up over 50% year-to-date (through March 2nd). Samsung and SK Hynix make up over 40% of the index. From the same piece:

“In the three years since ChatGPT, Samsung, SK Hynix and Micron have diverted the bulk of their manufacturing, research and investments toward the HBM (high-bandwidth memory) used in AI accelerators from Nvidia and Advanced Micro Devices Inc. That means less plant capacity to make plain-vanilla DRAM for basic electronics like phones. The three companies are prioritizing HBM over DRAM because of simple math.”

Set aside any “transitory” impact of oil and even tariffs, we’re probably in a “super-cycle” of AI demand, and that’s going to result in higher prices for goods across the board. Just last week, everyone was talking about AI-related deflation, but to get there, you first need AI infrastructure, and right now, key items required for that buildout are in short supply.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The Problem Is that Inflation Is Already Elevated

It would be one thing if inflation were running low, say below 2%, as it did over the past decade. But right now, inflation as measured by the core personal consumption expenditures (PCE) index is running around 3%. I use the core PCE index not just because it’s the Fed’s preferred inflation metric, but also because it covers a wider range of goods and services (partly why the Fed prefers it) and is less skewed by shelter. Core CPI has a 42% to shelter, whereas the corresponding weight in core PCE is 17%.

Based on the latest CPI and PPI (producer price index) data, we think PCE is going to come in hot.

- Headline PCE is expected to increase 0.34% in January (equivalent to 4.2% annualized) and rise 3.0% year-over-year

- Core PCE is expected to increase 0.44% in January (equivalent to 5.4% annualized) and rise 3.2% year-over-year

That’s hot! Core PCE clocking in at 3.2% year-over-year would be the highest reading since November 2023. And all this is before any potential impact from higher oil prices in January-February (core inflation also gets hit by oil prices through things like jet fuel and freight costs for transporting goods), or the memory shortage.

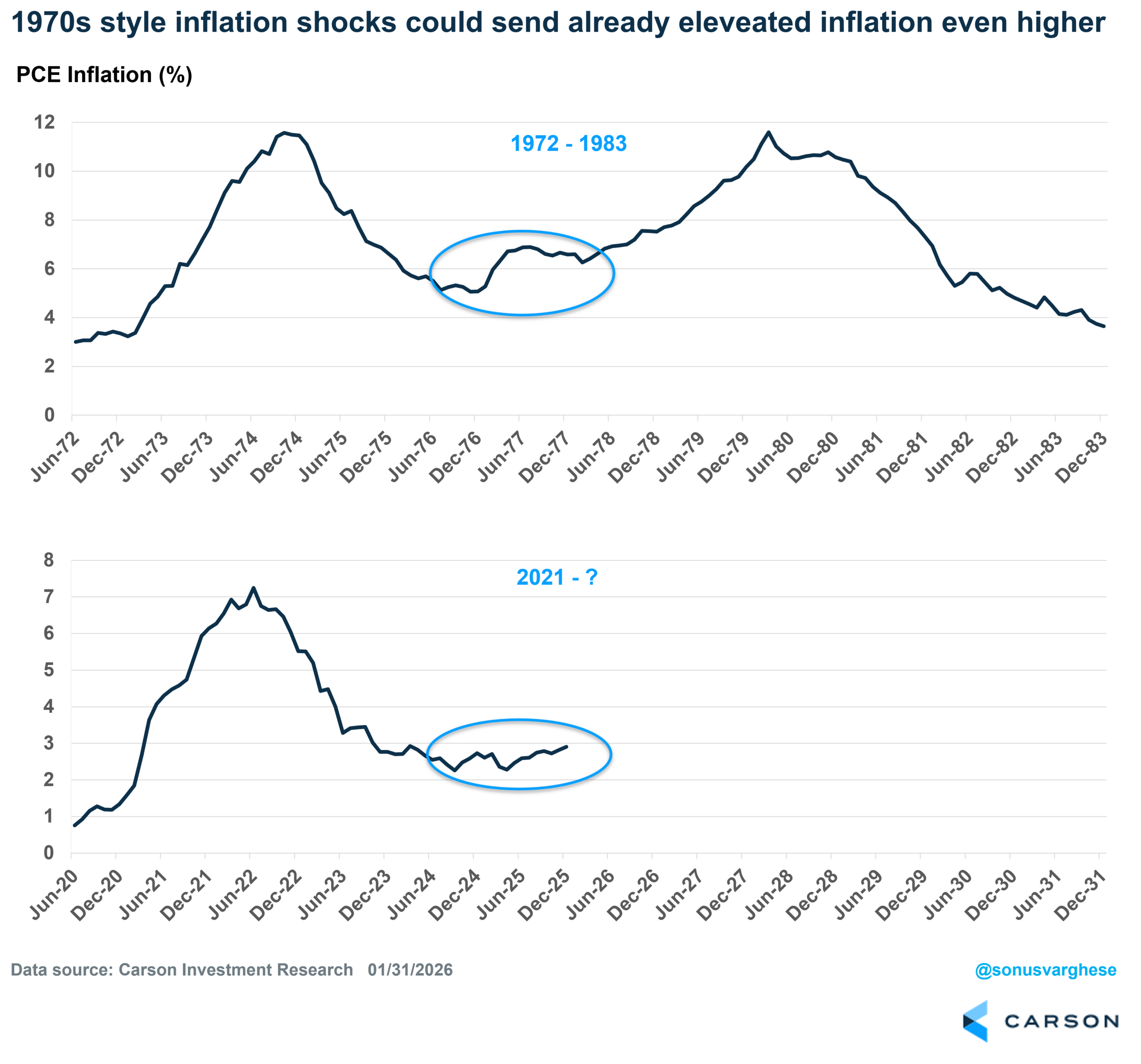

We have written in our outlooks for a couple of years that we’re likely in a regime with higher inflation volatility. That doesn’t mean we’ll see inflation average 4-5% over the next few years, but we could certainly experience shocks that could send inflation briefly higher. That’s part of why we have been underweight bonds and overweight commodities.

In a way, this is qualitatively similar to what happened in the 1970s. We had a series of price shocks in 1973-1974 (the oil embargo, food price increases, and Nixon’s removal of price controls), which subsided in 1975. But as the Fed eased interest rates, inflation didn’t quite pull down to the pre-1973 levels of around 3%. Inflation remained elevated around 5-6% even in 1976-1977. Then, when we got another food and energy price shocks in 1978-’79, which sent inflation surging over 10% once again. Subsequently, it took a massive surge in interest rates under Volcker to get lower inflation, though he broke the economy in the process.

I’m not saying we’ll see inflation anywhere close to those levels this time around. But a potential shock on top of already elevated inflation could send inflation surging above 3.5-4%. That’ll be immensely problematic for the Fed, let alone households.

If PCE inflation remains around 3% this year, with no sign of a pullback, it’s highly unlikely we will see any rate cuts from the Fed. On Friday, investors were pricing in 2 more 0.25%-point Fed cuts in 2026 and a 44% probability of a third cut. That’s shifted – investors are now pricing in just 1 cut in 2026 and 74% odds for a second.

If the probability of rate cuts approaches zero, expect quite a bit of market volatility.

For more content by Sonu Varghese, Chief Macro Strategist click here.

8801891.1. – 3MAR26A