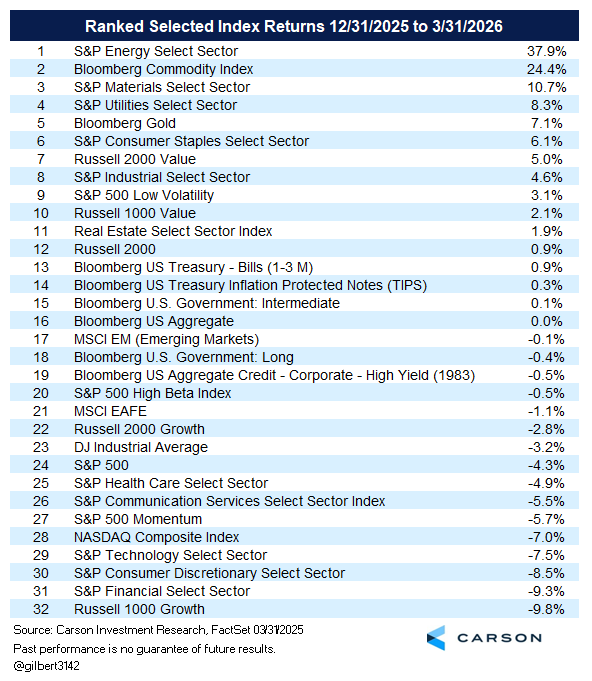

In the first quarter, the S&P 500 had a total return of -4.3%, with the Russell 1000 Value Index outperforming the Russell 1000 Growth Index by 12.1% while energy led all sectors. Oh, wait, sorry, that was the first quarter of 2025. In the first quarter of 2026, the S&P 500 posted a total return of -4.3%, with the Russell 1000 Value Index outperforming the Russell 1000 Growth Index by 11.9%, while energy led all sectors. Not a typo. While details varied, the first quarter of 2026 looked a whole lot like 2025. As a matter of fact, I created a quarterly “similarity score” for market texture across 55 major indexes going back to the start of 2012 (earliest date available for all indexes), and the first quarter a year ago scored the most similar to the quarter just completed. (If curious, the next two most similar quarters were Q2 2016 and Q3 2021, but that’s a blog for another day.)

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Returns are one thing, but there are similarities in the background events too, and that’s important because it increases the odds of a similar follow-up.

Taking a look, in the first quarter of 2025, President Trump took unilateral action on tariffs, bypassing congressional approval to implement a policy that had meaningful repercussions for global markets and the economy. Policies were eventually moderated, and the “TACO” acronym gained purchase, although the end result was still a major practical and philosophical shift from the US policy path over the last century.

And in 2026? President Trump also took unilateral action, bypassing congressional approval (although that’s the norm with short-term conflicts), that had meaningful repercussions for global markets and the economy. That policy decision looks like it may be running its course, gauging by the market reaction the last two days, although we’re still in wait-and-see mode on that. The macroeconomic consequences of the 2025 and 2026 policy decisions aren’t the same, and we’re at a different starting point, but the stylistic similarities tell a story.

We don’t expect what we saw over the rest of 2025 to strictly repeat in 2026, but it’s a reasonable expectation for things to at least rhyme. (See Carson’s Chief Market Strategist Ryan Detrick’s blog yesterday for a nice dive into some of the numbers that support this.)

For reference, over the final three quarters of 2025, the S&P 500 had a total return of 23.1%, and the Russell 1000 Growth Index (+31.7%) trounced the Russell 1000 Value Index (+13.5%). We would expect the numbers over the rest of 2026 to be much less dramatic, but to even hit the low end of our 2026 total return forecast from Carson’s Market Outlook 2026: Riding the Wave of 12-15% (which we haven’t changed), we would need to see a return of just over 17% over the rest of the year from the end of Q1. And while we would expect a narrower spread between growth and value, we would at least need participation from tech-related large-cap stocks to reach our forecast for the broader S&P 500.

One important difference between 2025 and 2026: In 2025, bonds provided decent diversification in the first quarter—the Bloomberg US Aggregate Bond Index (“Agg”) was up 2.8%. But in 2026, while the Agg was just short of flat in Q1 this year. But then our outlook for bonds in 2026 (3-5% for the Agg) is lower than it was in 2025. To hit the lower end, we would need to see the yield from the Agg roughly flat over the rest of the year (the current yield on the Agg is 4.57%). Despite inflationary pressure and the Fed on hold, with credit spreads having widened some from the conflict and bonds already giving back early-year gains, we think that’s very doable.

One more big difference. Last year in Q1, the small-cap Russell 2000 Index more than doubled up the decline of the S&P 500, falling 9.5% to the S&P 500’s -4.3%. This year, with the same return for the S&P 500, the Russell 2000 gained 0.9% despite recent rate uncertainty. Over recent years, there has been a lot of concern that equity markets are primarily supported by just a handful of giant tech companies. We think the worries were exaggerated—we saw more strength underneath the surface than many pundits, even if the gains of megacaps were outsized. But this year, at least, gauging by small-cap resilience, there does still seem to be confidence in the underlying economy.

Like last year, the first quarter was uncomfortable, although some real assets, small and mid-cap, or even international exposure provided some diversification. But despite the lingering effects of high tariffs relative to history, businesses were able to navigate the environment and mitigate some of the tariff impacts. This year, even if the US campaign in the Middle East ends over the next several weeks, there will also be lingering effects, and unlike arcane tariff rules, they’ll be harder to mitigate. But as Ryan discussed in yesterday’s blog, the difference maker is still earnings potential, and with valuations more reasonable following first-quarter headwinds, we think earnings growth is likely to support solid stock gains by the end of the year.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.

8855999.1. – 2APR26A