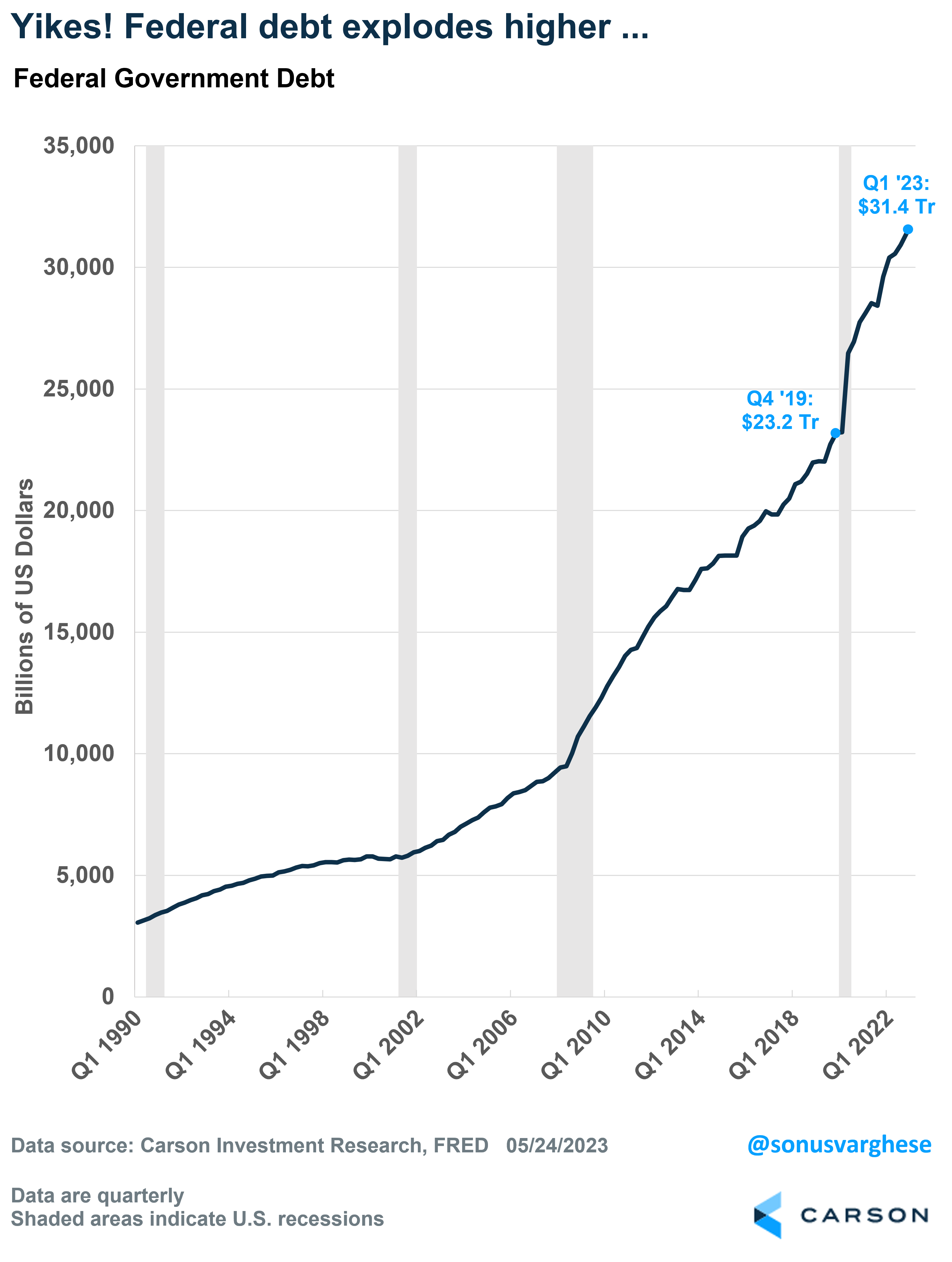

The fight over the debt ceiling in Washington D.C. has focused attention on the size of U.S. government debt. And it’s not pretty to look at. From the end of 2019 through the end of 2022, government debt has increased by a whopping 35% to $31.4 trillion. That translates to a dollar increase of $8.2 trillion!

The debt-to-GDP ratio jumped from 108% before the pandemic to 120% at the end of 2022. The only solace is that it’s fallen from 135% in the second quarter of 2020 – primarily because GDP increased by $4.4 trillion since then. Note that the denominator in the ratio is “nominal” GDP, i.e. it’s not adjusted for inflation. Nominal GDP has been increasing rapidly over the past two years thanks to inflation, rising 12% in 2021 and 7% in 2022. So, one way in which debt-to-GDP can fall is with higher inflation.

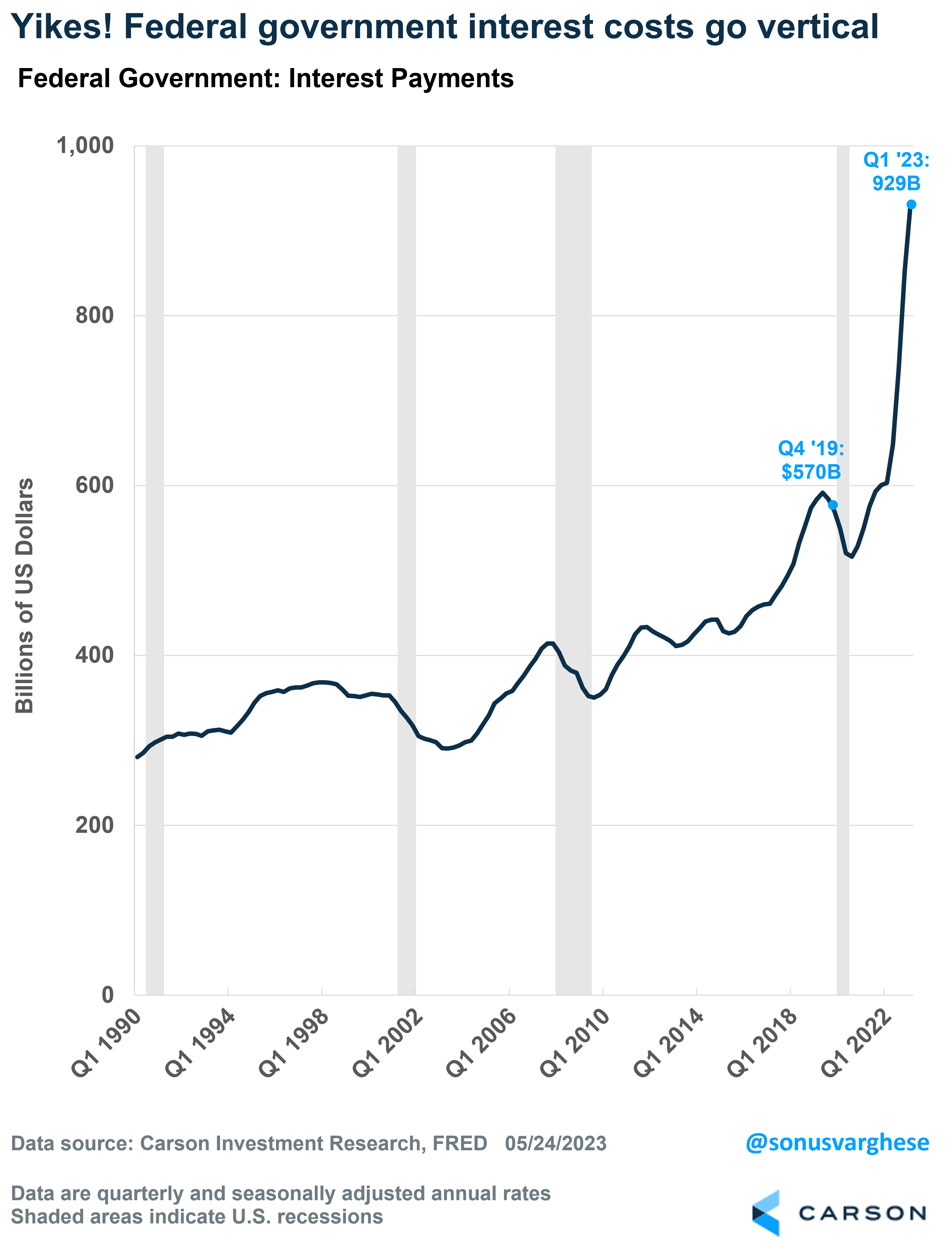

The problem with inflation is that the Federal Reserve is likely to react aggressively to bring it down, which is what happened last year. They raised benchmark interest rates from near 0% to above 5% over the past 14 months to clamp down on the highest inflation in 40+ years.

Higher interest costs for the government were a direct consequence of this. Interest payments on the federal debt have risen by $359 billion since the end of the pandemic through the first quarter of 2023.

But here’s the good news …

One thing that is weird about the debt-to-GDP ratio is that you’re comparing the “stock” of outstanding debt to GDP, which is a “flow”, i.e. the total dollar value of all finished goods and services produced within the country over a quarter.

It’s akin to looking at your mortgage balance as a percent of your monthly or quarterly income. A better measure of financial stress, or lack thereof, is mortgage debt service costs as a percent of income.

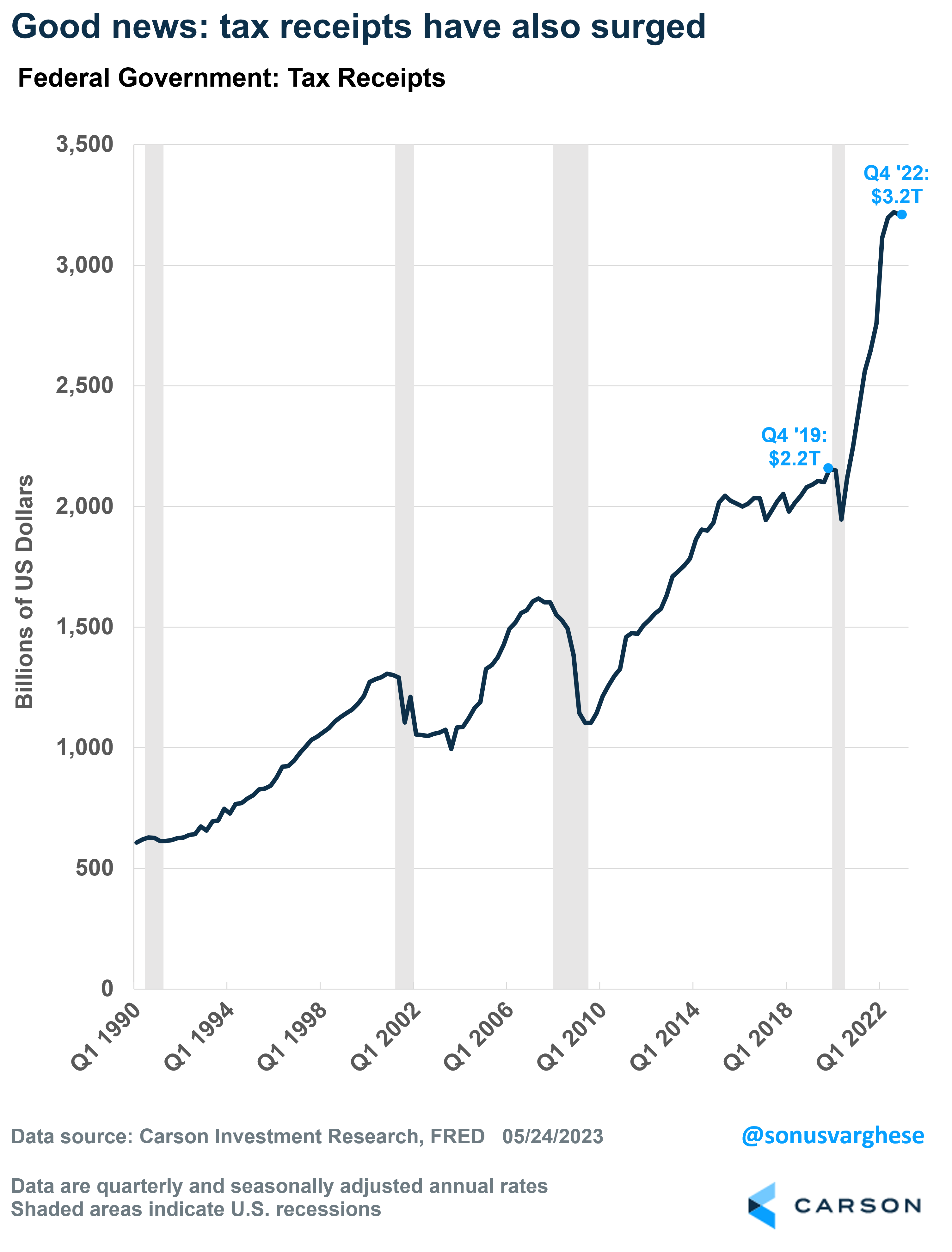

We can do the same thing for the government, in which case “income” is tax receipts.

As I noted above, debt-to-GDP fell over the last couple of years because nominal GDP grew. The other side of higher nominal GDP is that tax receipts for the government have also surged. Tax receipts have risen from about $2.2 trillion at the end of 2019 to $3.2 trillion by the end of 2022, an increase of $1 trillion.

This is the other side of government spending that kept the economy afloat in 2020-2021. Stimulus checks, PPP loans, and expanded unemployment benefits ensured that consumer spending held strong – the downside was higher inflation, as the pandemic shut down a lot of supply even as demand recovered immediately. Nevertheless, one person’s spending is another person’s income, and income is taxed.

The other reason tax receipts surged, especially in 2021, was an increase in capital gains receipts thanks to rising asset prices. This was less so in 2022. However, 4.8 million more people gained jobs in 2022, which helped push tax receipts higher.

The chart below shows government interest costs as a percent of tax receipts, and right now it’s just under 27%. It’s gone almost straight up over the last few quarters but remains slightly below where it was in 2019, which was right along the historical average of 27.3%.

Things don’t look too concerning when you look at the chart above. Ultimately, if the economy is growing, the debt-to-GDP ratio should remain stable (or fall), and tax receipts will continue to rise.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Recession is a real concern because that’s when tax receipts fall amid a rise in unemployment. This is why the ratio between interest costs and tax receipts jumped to over 50% in the early-to-mid 1980’s. Fed Chair Paul Volcker had raised interest rates sharply to combat high inflation, which resulted in:

- Higher interest costs on the federal debt

- A recession, which meant there were fewer tax receipts as spending and employment fell

Right now, we don’t believe we’re in a similar situation, and our base case is that the U.S. can avoid a recession this year.

Ryan and I just talked to Libby Cantrill, who analyzes policy and political risk at PIMCO, in the latest episode of our Facts vs Feelings podcast. She gave us a complete rundown on where things stand with the debt ceiling negotiations and discussed potential outcomes. Take a listen.