Kevin Warsh sat before the Senate Banking Committee on Tuesday for the start of his confirmation hearings as the next Chair of the Federal Reserve. He sidestepped most of the political gotchas, reiterated his commitment to Fed independence, and outlined what amounts to a reform agenda: replacing the Fed’s inflation models, shrinking the balance sheet, and paring back Fed communications. The S&P 500 finished down less than a percent on the day, and Treasury yields barely moved.

That muted reaction is worth dwelling on, because it tells you something important. Markets right now are focused on what’s directly in front of them: Profits. As I wrote yesterday, this year’s return has been driven almost entirely by rising earnings expectations, with profit margins hitting an all-time high of 15.2%. Against that backdrop, a change at the top of the Fed feels like a longer-term question. While it is, “longer-term” doesn’t mean “unimportant,” and there are a few things worth understanding now.

Near-Term

Warsh probably won’t be at the Fed anytime soon. Senator Thom Tillis has said he’ll hold up the nomination in committee until the administration drops its probe into outgoing Chair Jay Powell, and for the moment, that’s a stalemate. Betting markets assign roughly 28% to confirmation of Powell’s May 15 departure date, 67% to June 1, and 80% to July 1.

Even once Warsh is seated, one important fact gets overlooked: a Fed Chair is one vote out of twelve on the FOMC. The Chair has an outsized influence on the committee’s direction, but cannot unilaterally cut rates. And Warsh faces a specific credibility challenge on this front. He has been on record as a hawk for most of his career, including at moments when hawkishness looked badly miscalibrated. He argued for tighter policy in 2009 when unemployment was near 10% and core inflation was below 1%. He then shifted to a more dovish posture during the 2017 Fed Chair consideration process, and again more recently. Whatever one thinks of the underlying views, the pattern is likely to make it harder to persuade a committee of career central bankers who hold their own convictions.

As I noted when the nomination was first reported, the most likely near-term outcome is a Fed that’s a bit more hawkish at the margin because other committee members are unlikely to follow a Chair whose arguments for cuts look politically convenient. That’s roughly what we’ve seen: markets currently price in about a 63% probability of at least one cut in 2026, well below what you’d expect if a “dovish” Chair were truly taking over, especially since the odds just 2 months ago were over 90%.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The Balance Sheet

The more consequential question, and the one we think deserves more attention, is what Warsh wants to do with the Fed’s $6.7 trillion balance sheet. He has been consistent for 15 years in arguing that it’s too big, distorts markets, and has contributed to inequality by inflating asset prices.

The first two points are defensible, and reasonable people disagree. The third deserves scrutiny because it’s the argument most often used to justify aggressive balance-sheet reduction, and the data doesn’t really support it.

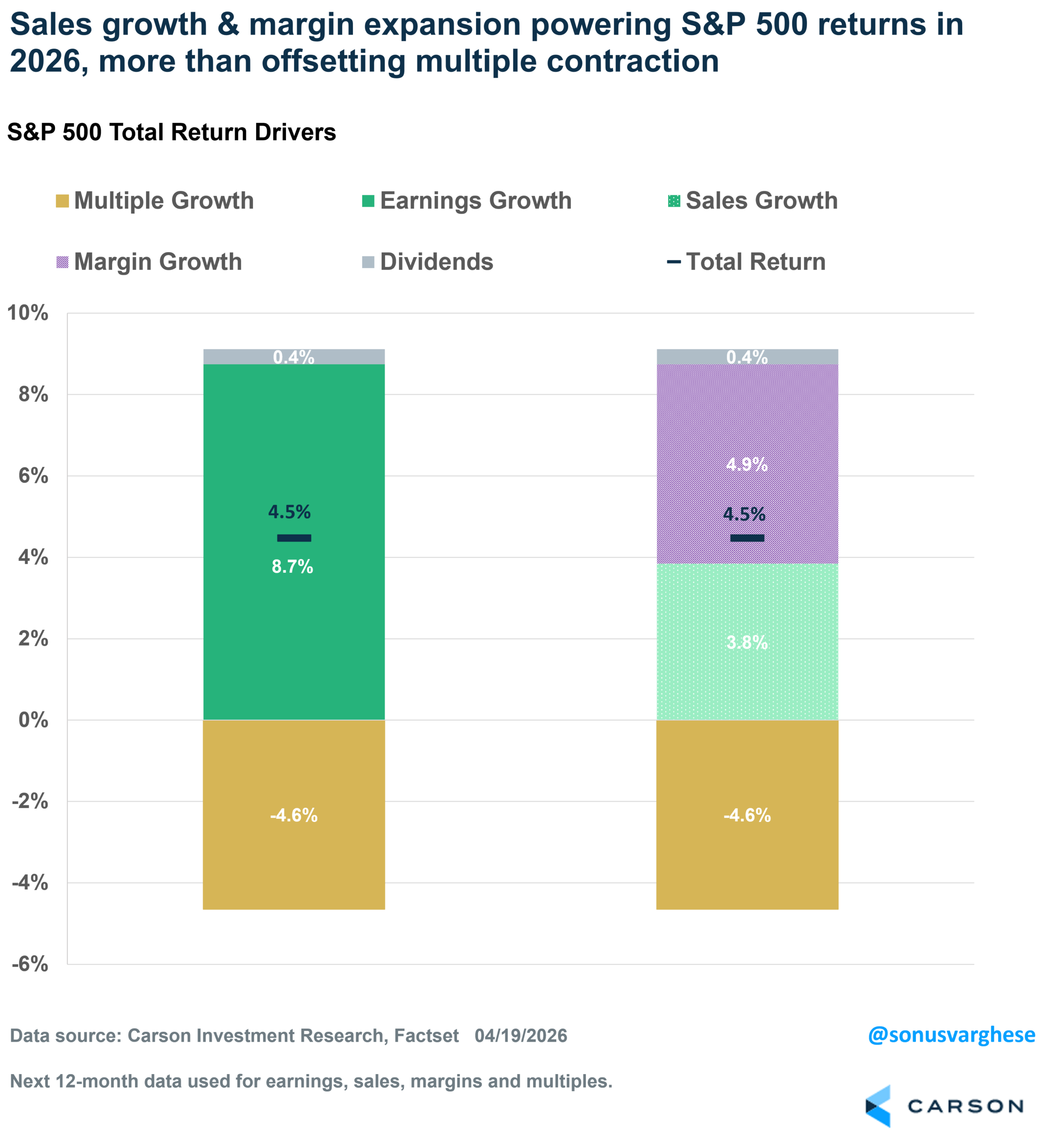

The claim is that the Fed’s expanding balance sheet has artificially boosted the stock market. If that were true, we would expect to see S&P 500 gains driven primarily by multiple expansion, i.e., investors paying more for the same dollar of earnings. But decompose the S&P 500’s annualized 14% return since 2009, and you get roughly:

- Earnings growth: +10 percentage points

- Multiple expansion: +2 percentage points

- Dividends: +2 percentage points

In other words, earnings did the work. The market has risen because corporate profits have risen. That same dynamic is playing out right now. As of April 17, the S&P 500 is up roughly 4.5% entirely on the back of rising profit expectations, while multiples have actually contracted by 4.6 percentage points. If the Fed’s balance sheet were the engine of asset price inflation, we’d expect the opposite.

This matters because if the diagnosis is wrong, the remedy could create problems. Aggressive balance sheet reduction in a system that has grown accustomed to ample reserves risks a repeat of September 2019, when a reserve shortage caused overnight funding rates to spike and forced the Fed into emergency repo operations. The Fed actually restarted modest balance sheet growth late last year for exactly this reason. Warsh’s framework may not account for this distinction.

What To Watch

The pace of any balance sheet reduction. There’s a wide gap between let it drift lower as bonds mature, and active sales or aggressive runoff. The former is benign; the latter could put meaningful upward pressure on longer-dated Treasury yields, which would hit equity multiples, particularly for longer-duration growth stocks that have led this year’s rally.

Bond market volatility. A Fed Chair who has publicly stated he wants to reduce Fed communications and change how inflation is measured is, by definition, a source of uncertainty for bond investors. Reduced forward guidance means wider distributions of possible outcomes, typically leading to higher rate volatility.

Credibility in the next crisis. This is the long-tail risk that doesn’t matter at all until it matters enormously. The Fed’s most important function is not setting rates in calm periods. It’s coordinating with Treasury and Congress during genuine crises, as Bernanke did in 2008 and Powell did in 2020. That requires credibility with both parties. A Chair who arrives via a politically contested confirmation, with a track record of views that shift with administrations, starts that job with less of it.

The Bottom Line

None of this should drive wholesale portfolio changes today. Markets are correctly focused on the profit cycle, which remains strong, and on the Fed’s current policy stance, which is data-dependent regardless of who is in charge.

But Fed leadership transitions do matter on longer horizons, and this one comes with more open questions than most. The right posture is to stay invested in what’s working, stay diversified against what could go wrong, and watch the balance sheet debate play out in the months ahead.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8892902.1. – 23APR26A