President Trump took office a year ago, and markets continue to be driven by his policy ambitions. Especially tariffs. In our 2025 Outlook we warned that tariffs were a looming threat. That materialized in dramatic fashion on Liberation Day (April 2nd, 2025), but as we noted a year ago, President Trump likely sees the stock market as a report card on his performance, so a negative market reaction may prompt him to temper some of his proposals. Back in April, negative reactions in the stock and bond market led to a significant pullback on tariffs, including several key products (especially related to AI) getting exceptions.

While most of the tariff headwind is likely behind us, the risk has clearly not been eliminated, as the president (“Mister Tariff”) reminded us this past weekend. He’s threatened to impose large tariffs on countries that oppose his intention to control Greenland, which currently includes Denmark, Norway, Sweden, France, Germany, and the UK. That would also undo the trade deal the EU and UK signed with the president last summer.

At this point, the onus is on the administration to prove these renewed threats are not empty. Until then, markets are likely to treat them as largely idle threats. Of course, if the Trump administration seems serious about the tariffs, markets will likely react in an adverse way, and then we’re back to the dynamic of last April, when the market reaction forced the administration to pull back. It doesn’t seem like the administration has a very high tolerance for a negative market reaction, and this may be even more true as midterms start to loom (more on that below).

Then there’s the upcoming Supreme Court decision on last year’s tariffs, which is expected any day now. If the Supreme Court rules against the administration, it could make everything go haywire, as the administration would be forced to scramble and re-up the tariffs using other authorities. Some of those would require Congressional approval (good luck with that) and others are cumbersome to impose as they require long, drawn-out investigations.

Midterm Year = More Populism

On the positive side, there are a couple of tailwinds, especially ones that the administration would be more than happy to tout.

- As we wrote in our 2026 Outlook, the tax cuts passed by Congress last year will make an immediate impact in the first half of 2026, including lower tax withholding for paychecks (boosting take-home pay) and higher refunds.

- We expect the Fed to continue their cutting cycle, though this may only restart after Trump replaces Fed Chair Powell and puts in his own person as Chair (presumably someone amenable to cutting rates).

Of course, it’s also a midterm year which means lawmakers are a little more prone to go populist, even more so for the current administration. We saw a slew of policy announcements over the last two weeks, including:

- Taking over Venezuela’s oil and pushing U.S. energy firms to invest money and rebuild Venezuela’s decrepit energy infrastructure to boost production and drive oil prices lower (and therein, gasoline prices).

- An increase in the defense budget from $1 trillion to $1.5 trillion for a “dream military.”

- Not permitting defense companies to return cash to shareholders via dividends and buybacks unless they speed up production and maintenance of military equipment.

These are remarkably market interventionist proposals, quite unlike anything we’ve seen in recent history. This is in addition to Trump announcing $2,000 tariff dividends for households (again, this is unlikely to happen without Congress, and that’s a long shot now), something he’s been floating intermittently for a while.

Trump Takes a Few Swings at Affordability

Affordability is a key source of angst amongst households right now, amid elevated inflation over the last several years and low real wage growth. It’s no surprise that the administration wants to tackle this before going into November elections.

Trump recently called for a one-year cap on credit card interest rates of 10%. While on the surface this may appear as a panacea for those with large credit card debt (and high interest rates on that debt), it’s likely to limit credit availability. A lot of households may even see their cards being cancelled by banks. The reality in the credit card business is that there’s a lot of cross-subsidization. Credit card companies make a lot of money from interest on loan balances that are not paid off in the first month they are incurred (revolving balances) and late fees. That allows card companies to offer loans to subprime borrowers, as risk-based pricing subsidizes access. It even allows companies to offer rewards for more affluent customers.

In other words, a subprime borrower has access to credit cards because the bank can charge 20-30% APR. Same with rewards, which also rely on behavioral inefficiencies and consumers who revolve their balances. Remember that points/rewards are a liability for credit card companies. If margins shrink, the liabilities get repriced, which means reward and premium benefits shrink. Premium rewards will require more explicit, higher fees, since there’s no longer hidden cross-subsidization. It’s also likely to force less credit-worthy borrowers into riskier borrowing channels. And will also benefit debit over credit. Credit becoming more scarce and less flexible isn’t great for the economy, since credit is key for consumption.

Affordability is a problem even on the housing front, thanks to mortgage rates over 6% and home prices continuing to rise (amid low inventory). This is also something the administration is trying to tackle, with a couple of notable proposals.

Trump ordered his “representatives” to buy $200 billion in mortgage bonds in a bid to lower mortgage rates and make housing more affordable. The goal is obviously to bring mortgage rates down, thereby improving affordability for prospective homeowners.

Source: Donald J. Trump via Truth Social (January 8, 2026)

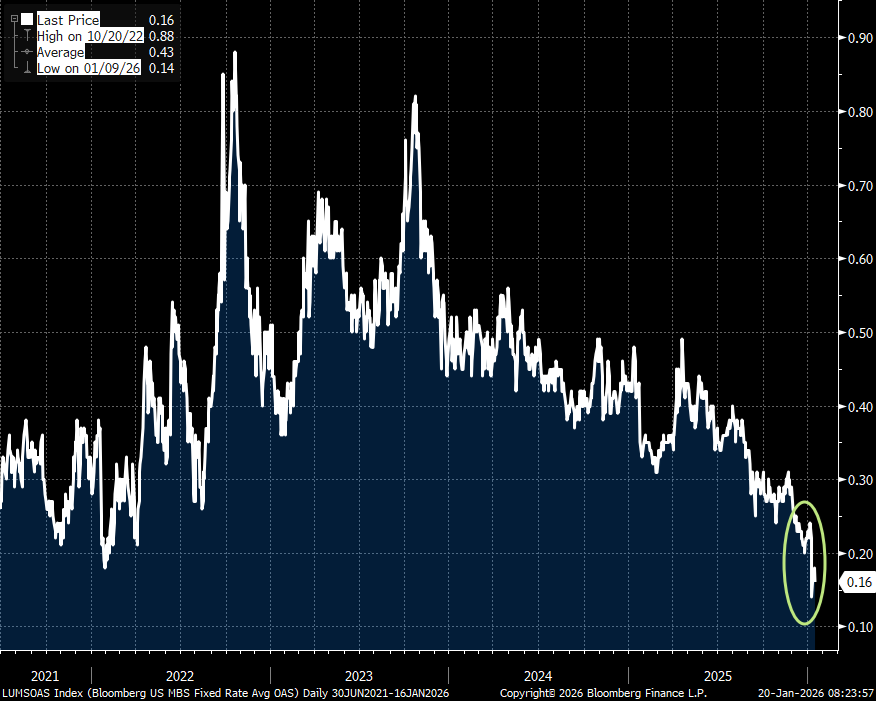

Presumably, he will direct his people at the Federal Housing Administration to have Fannie and Freddie buy $200 billion worth of mortgage-backed securities. For perspective, the two GSEs (government sponsored enterprises) have about $173 billion of accumulated net worth. So, this deployment, assuming it happens, would be significant and more or less use up the entire capital cushion these entities have built up. Markets moved quickly, suggesting investors are taking this seriously. Here’s a look at option-adjusted spreads (OAS) for mortgage-backed securities (MBS). We’re seeing a forced, policy-driven collapse in spreads — OAS dropped 0.1%-points after the directive, which is a relatively big move. And that makes sense if a buyer that is not sensitive to price is going to come in to buy a whole bunch of MBS.

The spread is key, because even if US Treasury yields stay where they are, mortgage rates can fall. 30-year mortgage rates key off of 10-year Treasury yields, and if 10-year yields don’t move the spread is the only way to bring mortgage rates down.

Of course, mortgage rates are not the only factor that determines affordability of a home. Home prices are also a big factor. The housing market still doesn’t have a lot of inventory. If you boost demand by lowering mortgage rates, that’s also going to push up home prices. In fact, any savings for monthly payments that come about due to lower mortgage rates may be entirely offset (and maybe even more) by higher home prices. In the interim, if mortgage rates do come down, we could see a pickup in refinancings and a temporary pickup in activity. Until inventory dries up again. Then we’re back to the push-pull between lower rates vs higher home prices.

The key thing to monitor to determine how successful the administration’s policy is will be MBS spreads and Treasury yields. If tariff threats result in higher yields, that can potentially erase any benefit from compressing spreads.

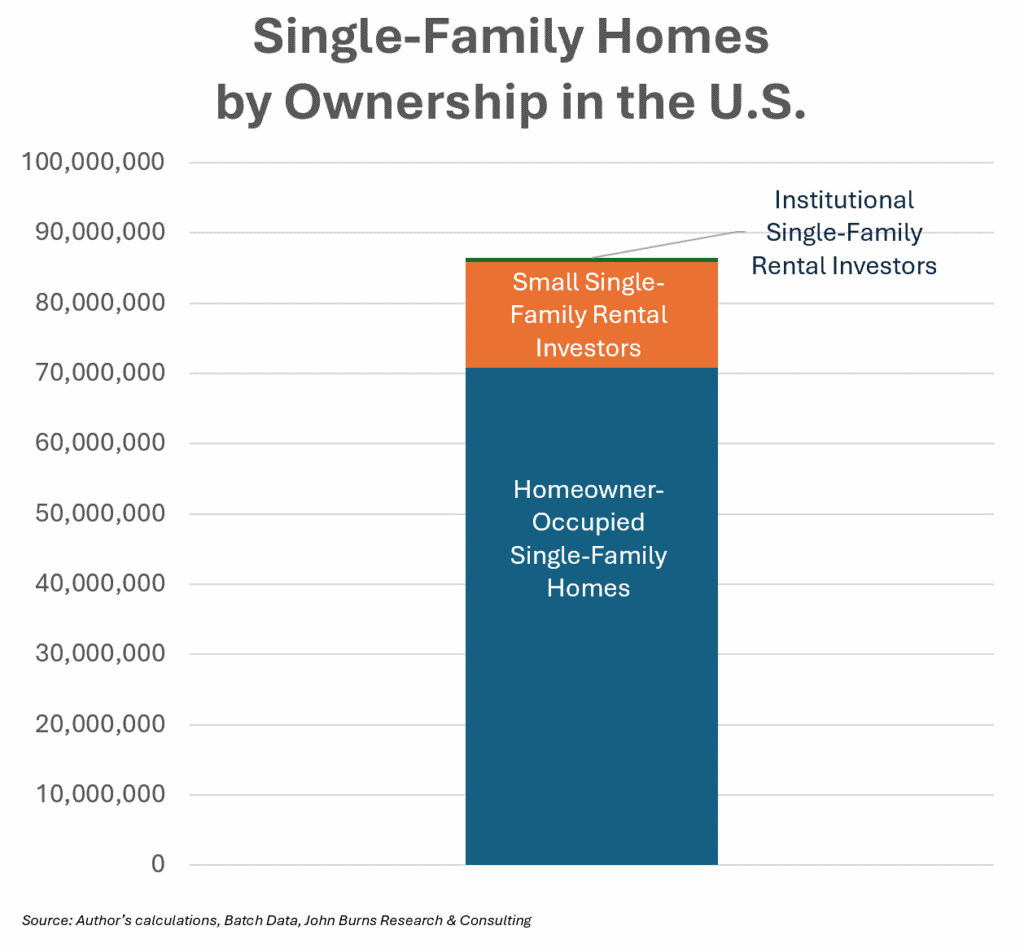

Trump is also looking to ban large investors from buying homes. The theory here is that large institutional buyers (like Blackstone) come in and out-compete potential home buyers who are looking for a single-family home and then rent it out. So, banning them will presumably 1) reduce home prices, and 2) increase inventory and purchases by households.

Source: Donald J. Trump via Truth Social (January 7, 2026)

The problem is that institutional investors, or landlords with 100+ properties, account for just 1% of US home purchases. Institutional investors represent ~ 3% of single-family rentals, but closer to 0.5% of ALL single-family homes. Most single-family rentals are actually smaller landlords. The reality is that large single-family rental operators like Blackstone are also focused on cap rates and yields and competing with homeowners on low inventory/high priced homes would kill yields. They probably focus more on homes undervalued by the market, since they can do repairs much more cheaply with the crews they typically work with. Competing with homeowners in bidding wars will push up market prices, and crush yields.

Also, after the financial crisis mortgages for starter homes became rare, so the only buyers of cheap single-family homes were institutions looking to rent them out (and frankly these wouldn’t have been built otherwise). The ban on institutional ownership is going to do nothing for home affordability on the price front. And it may make things worse by reducing the inventory of homes, which would only add to the current problem. Institutional buyers buy a lot of homes directly from builders (and rent them out). This also keeps construction demand going at a time when housing is weak. However, if these firms are forced out of the market, builders will take a hit, as will construction.

Now, all real estate is local and there certainly are pockets where institutional investors are a much larger player, especially locations in the South and Southwest, including Atlanta, Phoenix, Nashville, Orlando, Tampa, Vegas, Charlotte, Austin, and Dallas. However, in all these areas, home prices are actually easing and in fact rents are falling at a faster rate than in the rest of the country.

All this to say, a lot of these proposals may not have the intended effect. At best, they’d be neutral and at worst, it could make affordability worse. Of course, a lot of these proposals will require Congress to get involved, and passing anything in a two-seat Republican majority House may be almost impossible. Still, don’t expect the policy proposals to stop coming in. As I noted at the top, it’s a midterm year after all.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

8725394.1. – 20JAN26A