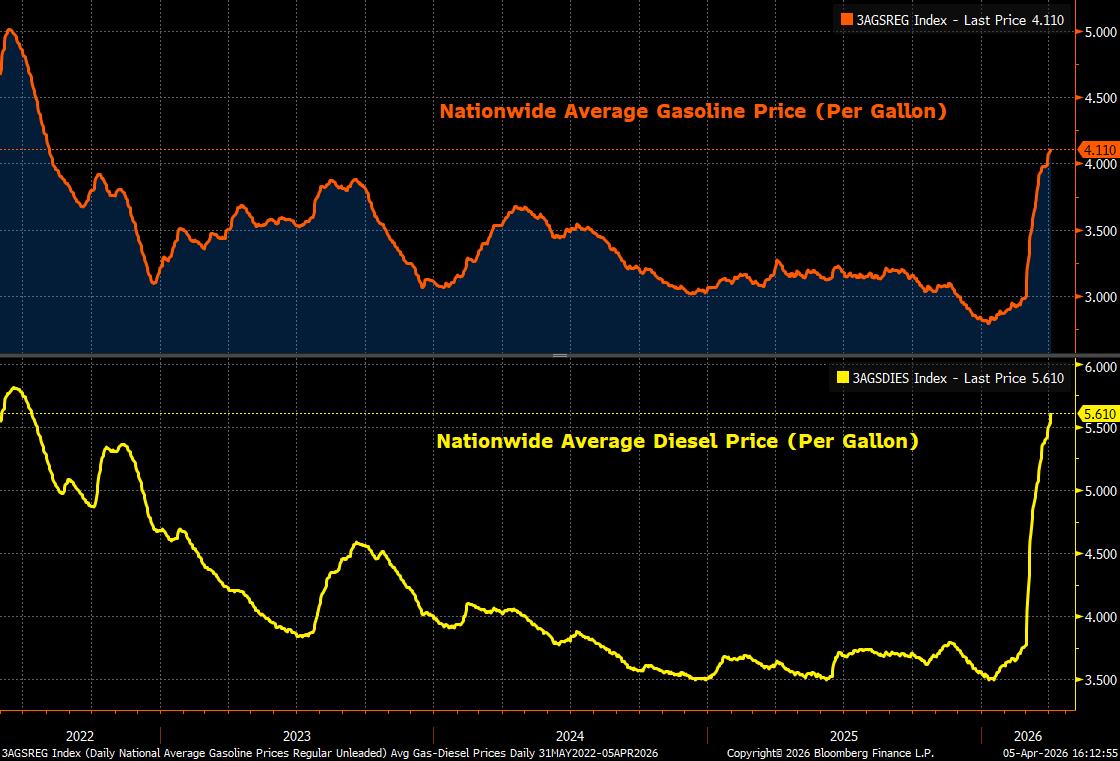

The crisis in the Middle East is in week six right now, and it’s not hyperbole to say that the world is on the edge of an energy crisis. Oil prices have surged over the past several weeks, with the price of WTI (the US benchmark) surging over $100/barrel last week—it was at $65/barrel on the eve of the crisis on February 27. No surprise, that’s sent gas and diesel prices to the highest levels since 2022:

- Nationwide average gasoline prices are at $4.11/gallon, the highest since August 2022, and up from sub-$3/gallon in February.

- Nationwide diesel prices have surged even more, to $5.61/gallon, the highest since July 2022, and up from $3.75/gallon pre-crisis.

Keep in mind that higher diesel prices are going to hit food prices, since food has to be transported via trucks. Shipping fuel costs are rising, which is going to increase the price of goods (and we still import a lot of goods from Asia and Europe, including a lot of capital goods required for the AI buildout). Jet fuel prices in Asia and Europe are also surging, which is going to make air travel a lot more expensive. All this to say, this is not going to be just about higher oil prices translating to higher gasoline prices. There’s going to be a wider inflation problem.

The ugly inflation outlook leads to two important questions about the labor market:

- Is the labor market strong enough to withstand the shock?

- How will policymakers at the Federal Reserve balance inflation against the labor market, as they look to achieve their dual mandate of low and stable prices and maximum employment? “Low and stable prices” are out of the window (and kind of have been for about five years now). The question is how far the Fed will go to get things back on track (if they do anything at all), and that depends on the labor market.

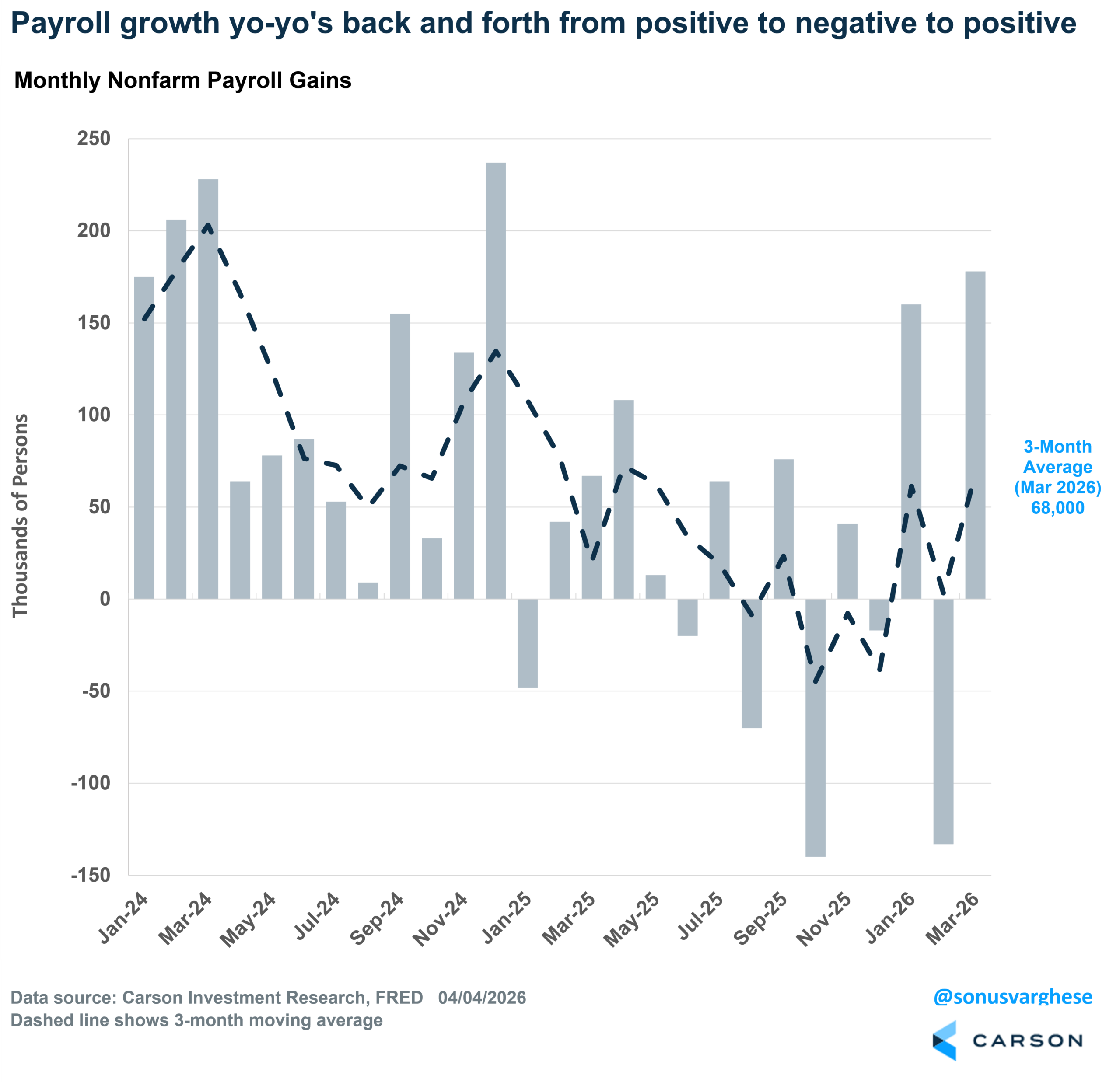

A Solid Payroll Report Points to an OK Labor Market

The March payroll report was solid on the surface, with the economy creating 178,000 jobs in March, well above the 65,000 forecast. At the same time, payroll growth for February was revised down by 41,000, from -92,000 to -133,000, while January payrolls were revised up by 34,000, from +126,000 to +160,000. We always recommend looking at a three-month average and right now that’s sitting at 68,000, which is pretty good.

As you can see in the chart below, payroll growth has yo-yoed between positive and negative growth for 10 months now, with payroll growth averaging 15,000 over the past six months and 22,000 over the last twelve. So, the most recent three-month picture looks like a bit of a pickup, but it could also be noise.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Due to the big drop in immigration, the economy needs a lot fewer jobs to keep up with population growth (the “breakeven rate of employment”). Researchers at the Dallas Federal Reserve found that the breakeven rate averaged about 166,000 in 2024, but fell to 10,000 by July 2025 and declined to near zero thereafter, averaging about -3,000 jobs per month from August to December 2025. That is incredible. Declining population growth means the economy does not have to create net new jobs to keep the unemployment rate from going up! The latest three-month average of 68,000 looks pretty good relative to that.

On top of that, the payroll growth data is derived from a really large survey of over 150,000 businesses across 600,000+ locations (which is why only the government is practically able to pull this off) but this isn’t an exact science. The Bureau of Labor Statistics (BLS) says that the 90% confidence interval is about 122,000 jobs per month. That effectively means that if the breakeven rate is around zero, we’re going to see large positive and negative numbers.

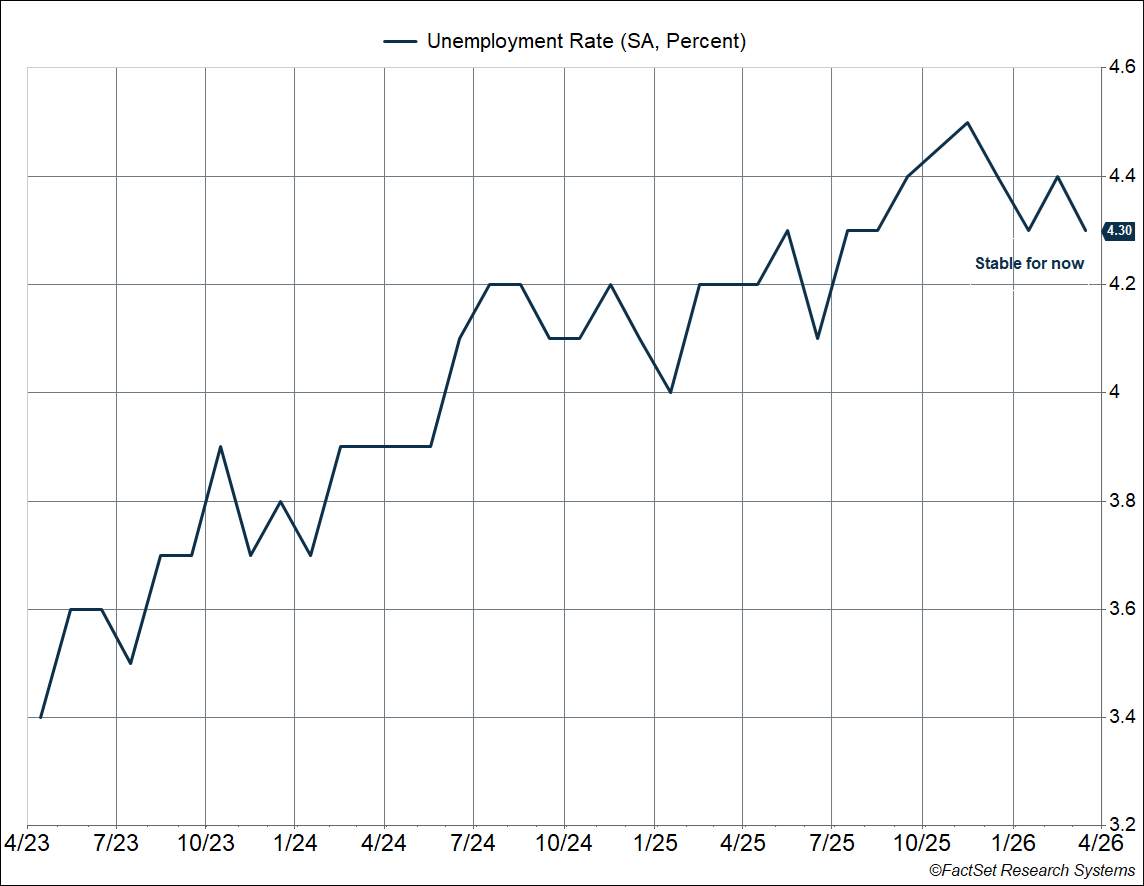

This is why it’s probably better to focus on the ratios like the unemployment rate right now. And the news is good. The unemployment rate fell from 4.44% in February to 4.26%, the lowest since last June. The only wrinkle here is that the apparent drop is because a lot of people looking for jobs have dropped out of the labor force and stopped looking for work (so they’re no longer counted as “unemployed” by the BLS). Nevertheless, the big picture is that the labor market cooled a lot after 2023. That cooling accelerated in mid-2025, which is essentially what prompted the Fed to cut rates by 1.75%-points. But things have stabilized over the last four months.

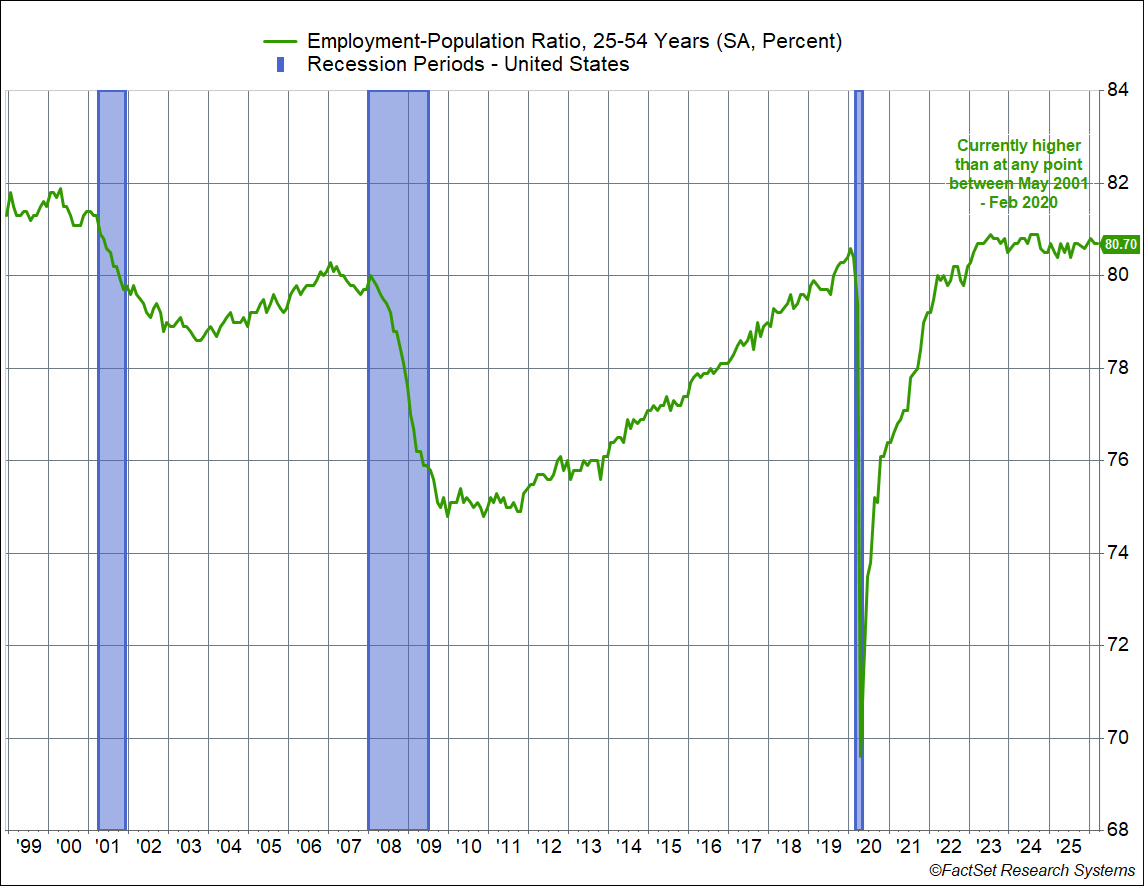

The picture looks better if we look at the prime-age employment-population ratio, which avoids issues around definitions of who is unemployed and demographics (due to an aging population). The ratio is at 80.7%, close to the peak we’ve seen this cycle (80.9% in September 2024) and higher than at any point between May 2001 and February 2020. In other words, more people in their prime-age working years are working now than at any point in the 2000s or 2010s expansion cycles (as a percent of the population).

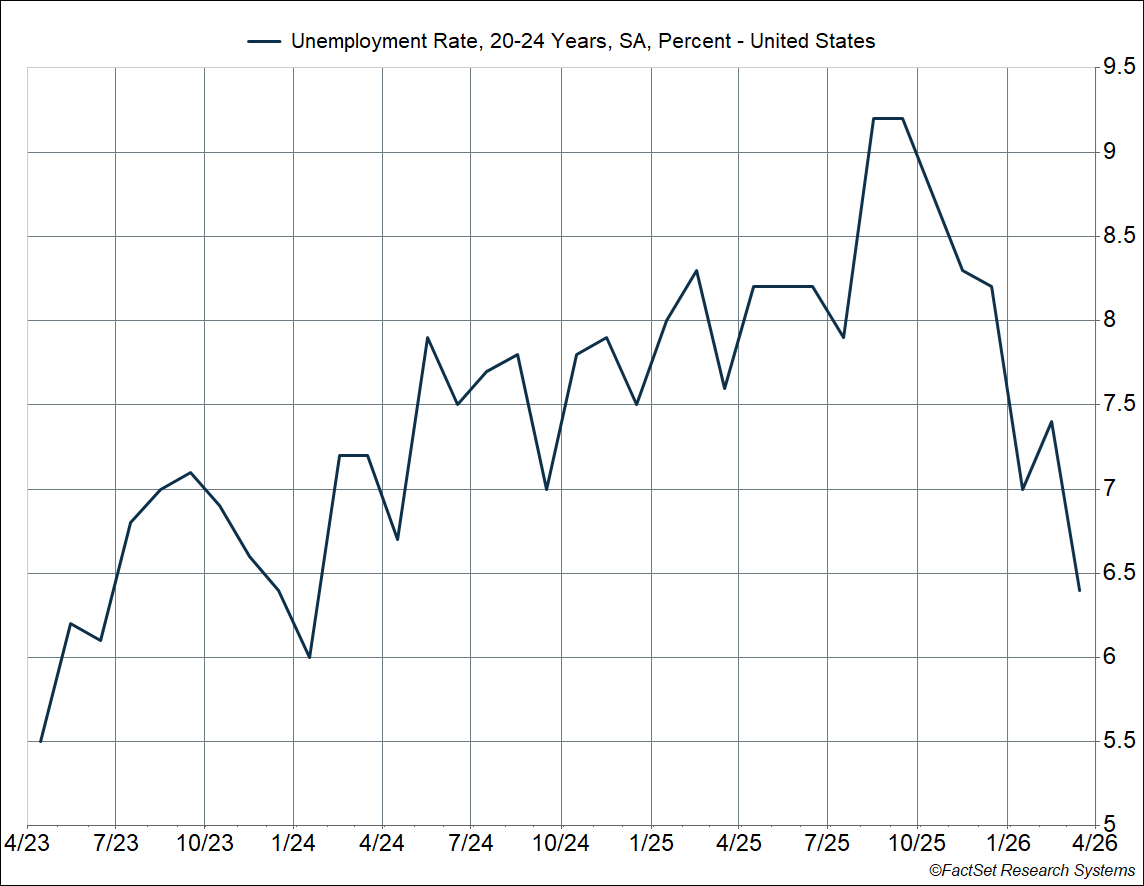

One question that’s recently come up is the impact of AI and whether that’s pushed the unemployment rate higher for less experienced workers. It doesn’t seem like there’s been a huge impact as yet, with the unemployment rate for 16–24-year-olds falling from a peak of 10.6% in November to 8.5%. That’s the lowest in almost two years. Interestingly, that’s been driven by a falling unemployment rate for 20-24-year-olds, from 9.2% in September to 6.4% in March, the lowest since January 2024. If anything, you’d think recent college graduates in the 20-24 range would be most negatively impacted by AI. This data is noisy, but as you can see below, the recent downtrend is quite clear.

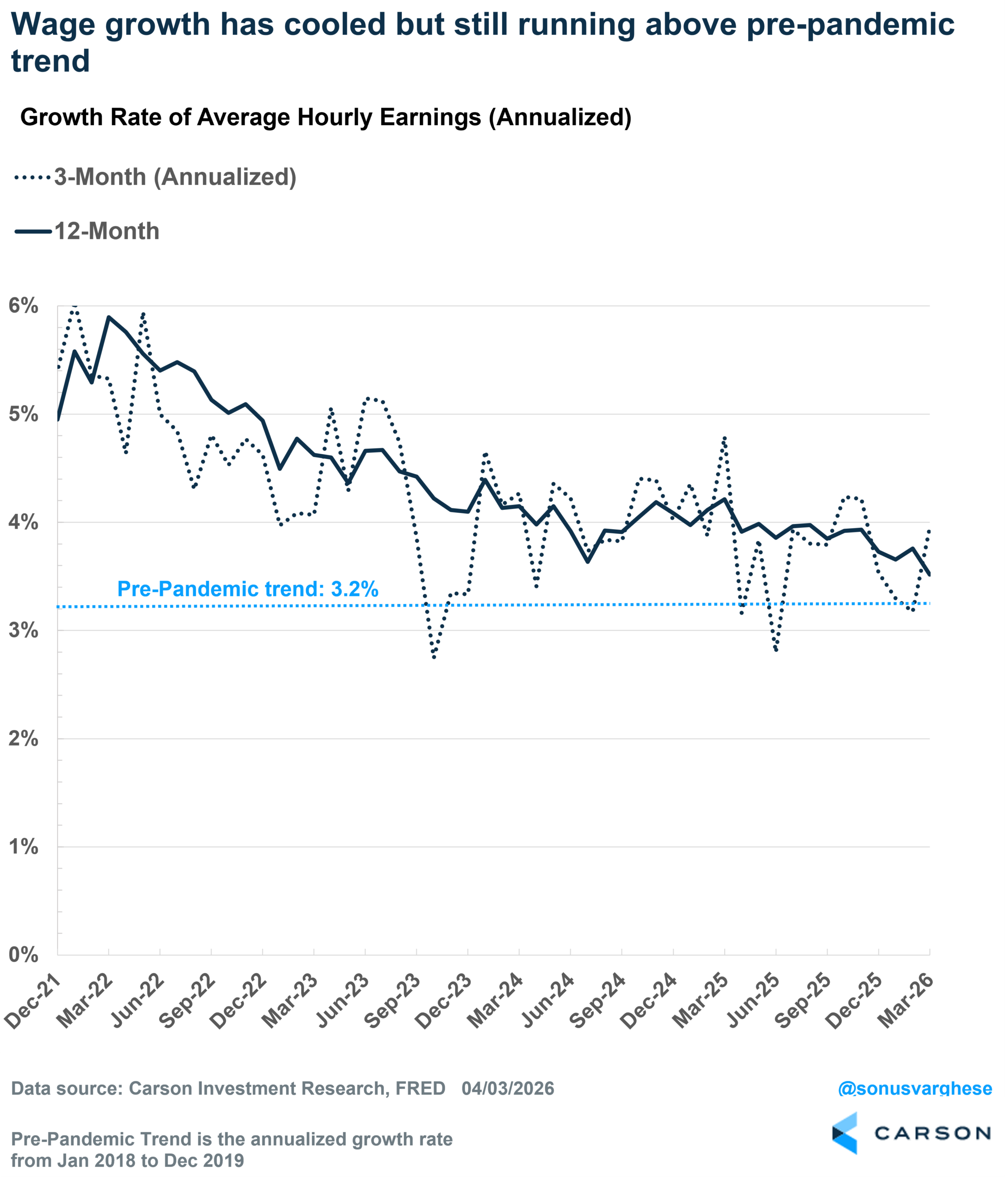

Another datapoint you’d look at if you want to see whether the labor market is tight or not, and a potential source of inflationary pressure, is wage growth. Wage growth has steadily cooled over the past year and is currently running at a 3.5% year-over-year pace, but that’s still above the pre-pandemic pace of 3.2%. Moreover, wage growth is running at a 3.9% annualized pace over the past three months.

None of this data points to an especially weak labor market. However, that also means the Fed may be more focused on the inflation picture, and that means more rate cuts are not coming anytime soon. Whether that means rate hikes are on the horizon is another whole question, but that’s going to depend on the inflation data over the next few months, which in turn depends on the length of the conflict in the Middle East and its outcome. Don’t be surprised to see more market volatility as investors furiously try to price out the potential interest rate policy path on the back of what happens in the Middle East (and resulting inflationary pressures).

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8859207.1. – 6APR26A