The economy created just 143,000 jobs in January, well below expectations for a 175,000 increase, and less than half of the gain in December (which was revised up from 256,000 to 307,000).

Over the last three months, job growth has averaged about 237,000 jobs, which is really strong. However, the payroll numbers are messy right now. For one thing, January could have been impacted by snowstorms in the south and the wildfires in California. We also got significant revisions for the prior couple of years. Total job gains in 2023 was revised down from 3.0 million to 2.59 million, while 2024 was revised down from 2.23 million to 2.0 million. Make no mistake, these are strong numbers, and if anything, it tells us productivity growth was actually better than was reported since GDP growth is still fairly strong. Still, there’s a lot of uncertainty with these monthly payroll numbers, more so than usual.

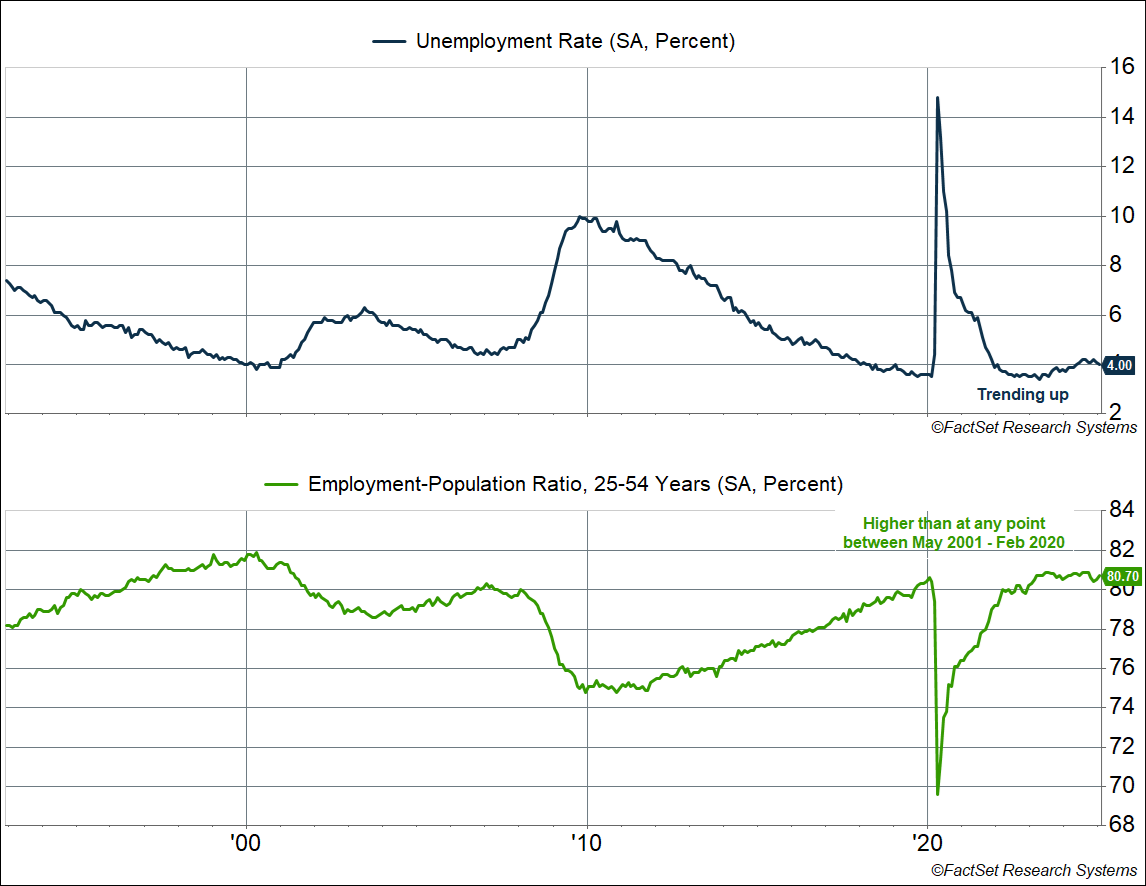

The good news is that readings that are slightly more resilient to revisions, like the various ratios (since both the numerator and denominator get revised) are still looking quite good. The unemployment rate fell from 4.1% to 4.0%, the lowest since last May. The prime-age (25-54) employment-population ratio, which is a way of controlling for demographic effects and labor force participation issues, is 80.7%. That is higher than at any point during the last two expansion cycles (2000s and 2010s) and not far below the recent peak of 80.9%.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The relatively stability of these numbers tells you that most people are employed, more so than we saw over the past two decades. Hiring has certainly eased over the last two years, but fewer workers are quitting their jobs and layoffs are still really low, so net hiring (hiring net of separations) is strong enough to keep up with population growth.

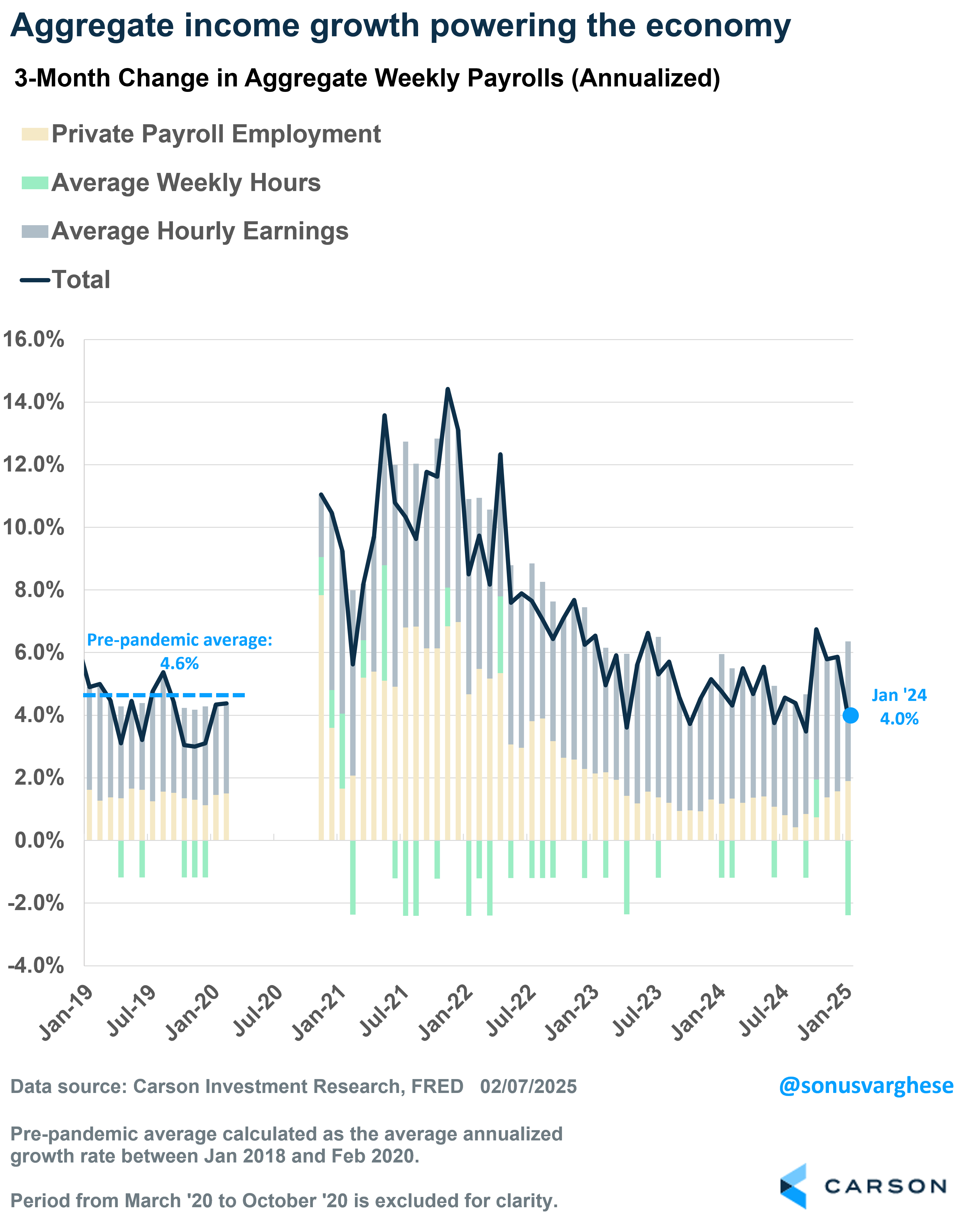

Ultimately, what matters for the economy is consumer spending, and since that’s powered by income growth, that’s where you want to look. Aggregate income growth, across all workers in the economy, is the sum of employment growth, wage growth, and change in hours worked. Over the past three months, that’s running at an annualized pace of 4%. That is not too far below the pre-pandemic average of 4.6% and tells you that the backbone of the economy is strong enough for now.

Elevated Interest Rates Are Not Helping

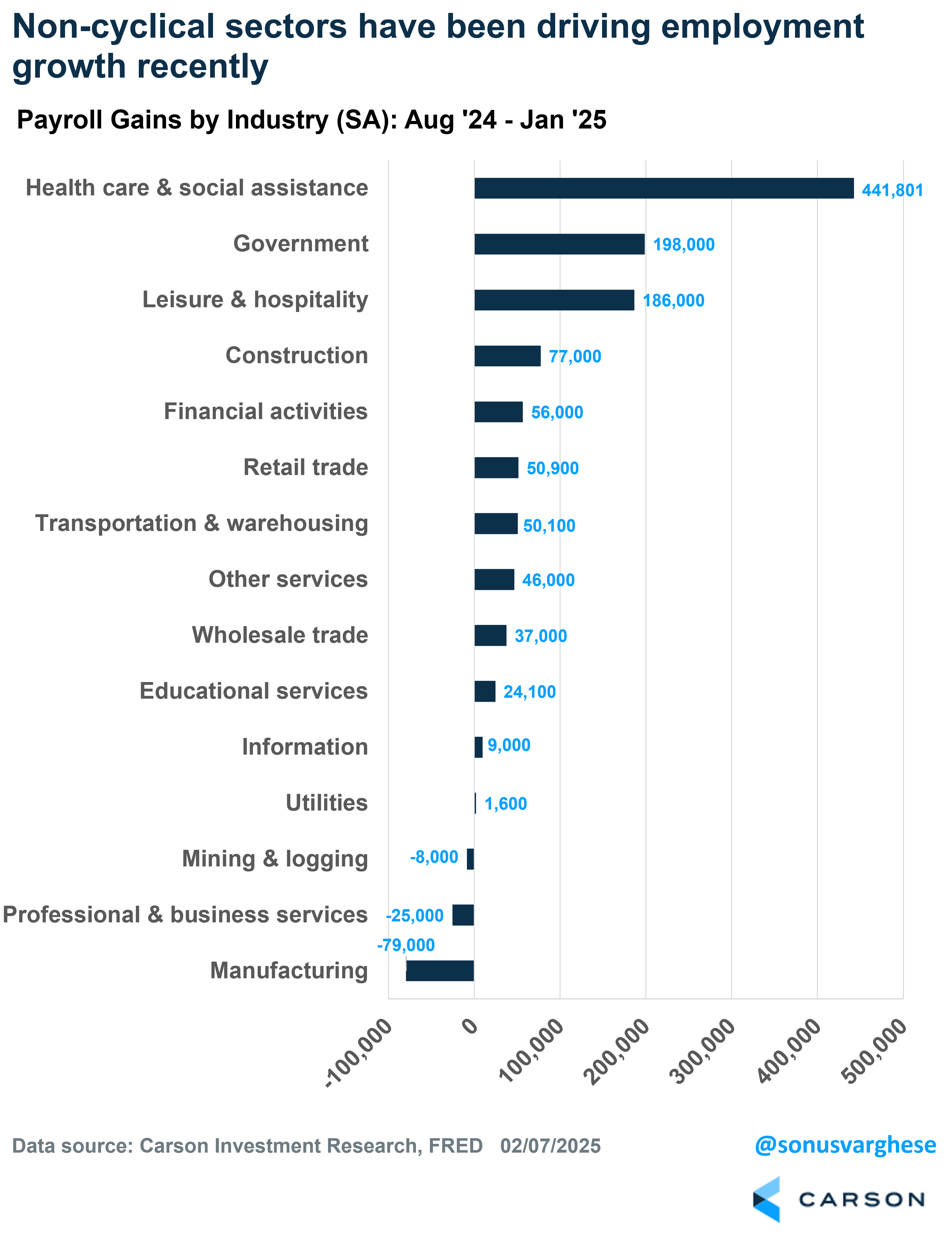

We are seeing some weakness when looking at the composition of where job growth is happening. Around 69% of jobs created in January were in health care and social assistance (+66,000) and government (+32,000, of which 23,000 was state/local government). A single month can be noisy, but we’ve seen this pattern play out over the last six months as well. Payrolls have grown by 1.1 million during this period, but a majority of that has come from non-cyclical areas, like health care and social assistance (+442,000; 41% of the total) and government (+198,000; 19%). Job growth in leisure and hospitality (+186,000; 17%) and retail trade (+51,000; 5%) were also significant, but these are less important than fields like manufacturing and professional services if you’re looking for an accelerating economy. Manufacturing payrolls fell by 79,000, while professional and business service payrolls fell by 25,000 over the last six months. It tells you that that cyclical areas of the economy are still struggling to get on their feet and are likely weighed down by interest rates.

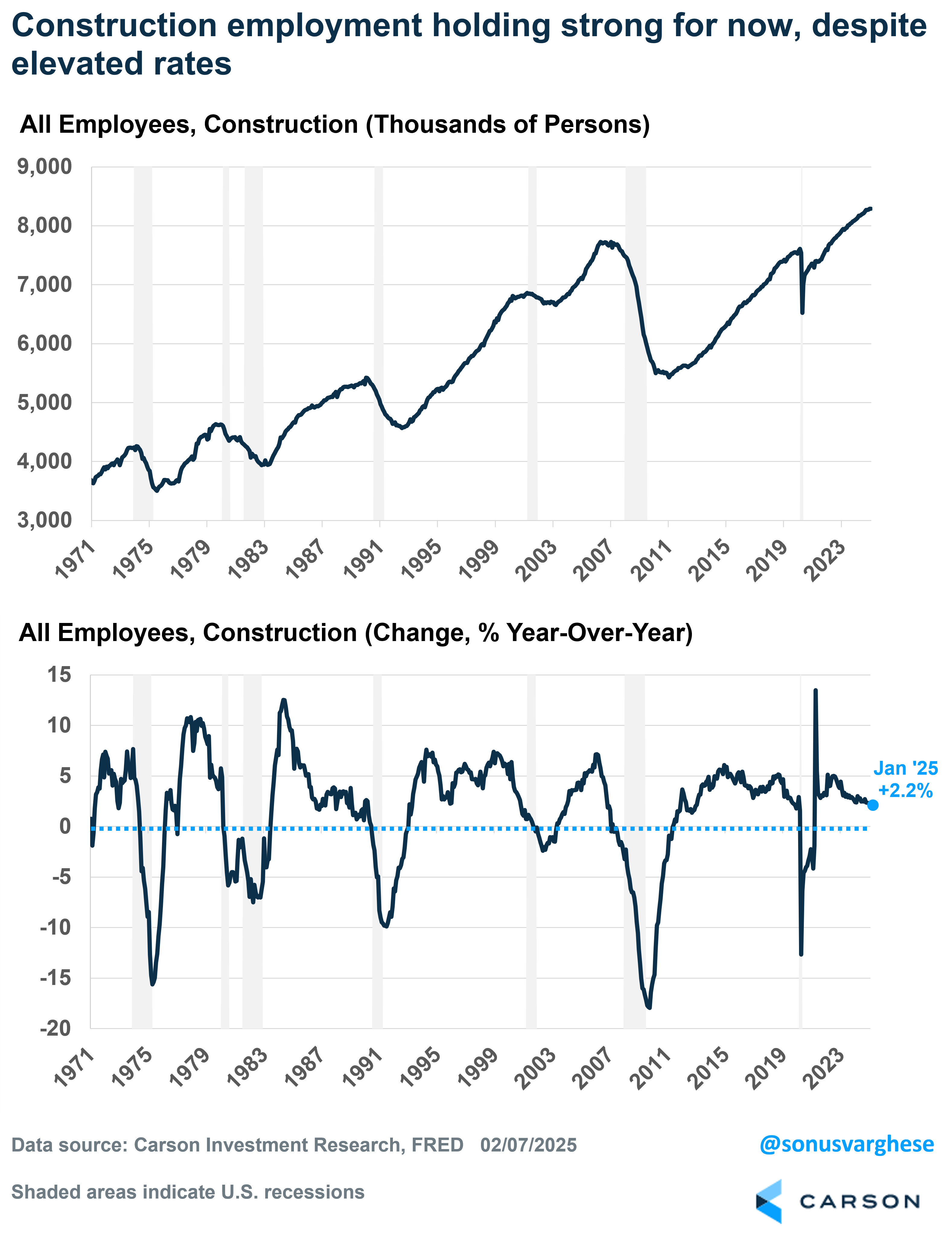

The one cyclical area that is holding relatively well is construction, despite the obvious headwind of higher rates. Historically, weakness in construction employment has foreshadowed further weakness across the labor market (and recessions), which makes sense because elevated interest rates (and tight monetary policy) have preceded past recessions. If housing remains weak due to elevated rates, we could see construction employment start to pull back. For now, construction employment is rising at a 2.2% year-over-year pace — still healthy, especially relative to the 1.8% increase in 2019, but the current pace is down from 2.5% six months ago. The slowing pace of growth is something we’ll be keeping a close eye on for the next several months. One notable area driving the slowdown is home improvement, where payroll growth has slowed to 0.6% year over year, versus 1.3% six months back.

The big picture right now is that the labor market is in a relatively healthy place. If you have a job, it’s very likely you’ll keep it, as employers are reluctant to let people go. Workers are also seeing their wages grow at a fairly good pace. However, hiring has certainly eased significantly from a year ago, let alone two years ago, and so if you’re looking for job, it’s not that easy to find one. Employers are clearly being very selective, and perhaps more so in the cyclical areas of the economy like manufacturing and professional services.

But therein lies the challenge of interest rates staying elevated for longer — it’s clearly a headwind if you’re looking for further economic acceleration, especially to achieve something like 3% GDP growth. This is exactly what we wrote in our 2025 Outlook, and the January data underline it. And as I wrote earlier this week, this is where the tariff uncertainty really manifests, as it makes it more likely that the Federal Reserve delays additional rate cuts even longer, as they wait for policy clarity (let alone the impact of these policies). Meanwhile, the hope is nothing breaks before that.

Carson’s Chief Market Strategist, Ryan Detrick and I discussed tariffs from the perspective of markets and Fed policy in our latest Facts vs Feelings podcast. Take a listen.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7616502-0225-A