Today, we take a look at what’s worked defensively during the current rising rate period. I’m emphasizing “current” because every rising rate period has its own characteristics.

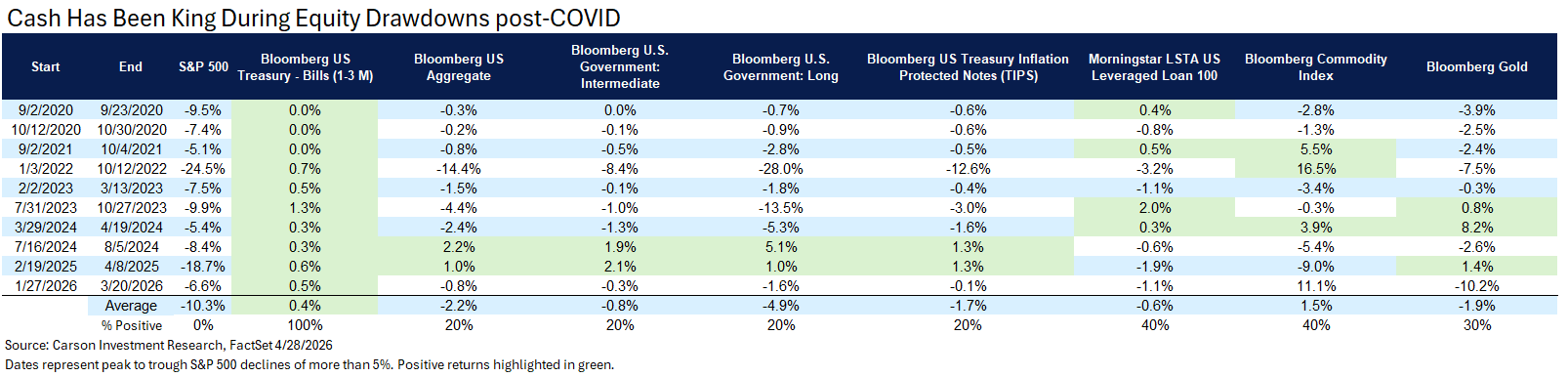

To do this, we’ve looked at all S&P 500 drawdowns of more than 5% since September 2020. In some of these periods, bonds did “work” as a diversifier—in most, they did not, at least in the sense of providing a positive return. Returns were still generally better than the S&P 500, but keep in mind this was a period of strong stock advances overall, so a lot of ground was lost on the upside.

Cash (Treasury bills) was the most consistent at providing a positive return during these drawdowns, but this is true almost by definition. But cash has also had the second-best average return, and that’s more of a surprise. Leveraged loans (below investment grade floating rate debt) and commodities were the next most consistent, although still only positive 40% of the time. Commodities also had the best average. A caution not to expect this in every period of market volatility, even when rates are rising. If there’s a credit shock (loans) or demand shock (commodities), either can see sharp declines. But in an inflationary growth period, where rates are rising, but the economy is staying relatively healthy, it makes sense that these indexes performed better.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

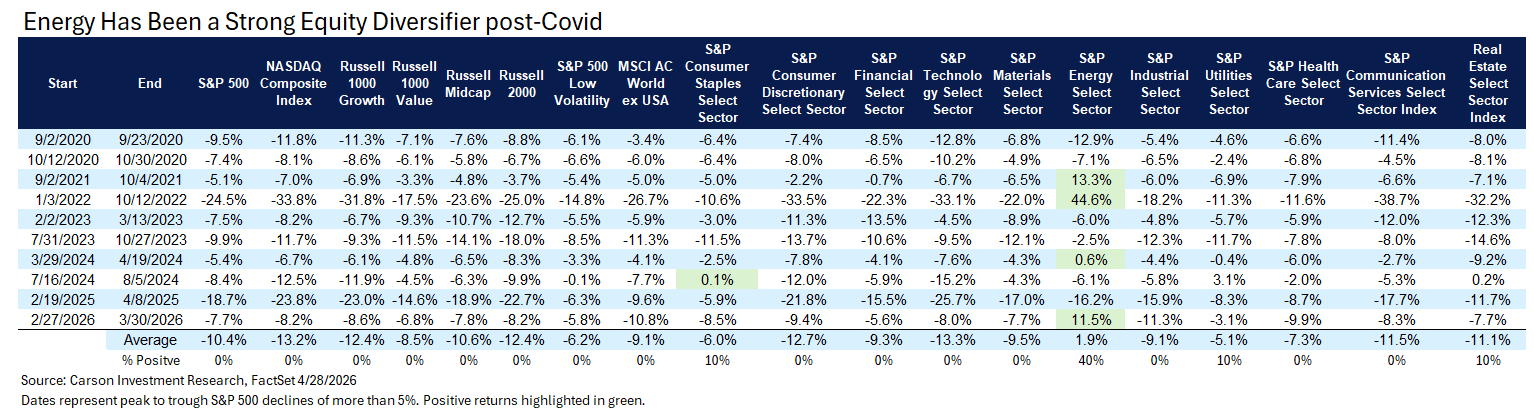

The equity side has mostly been more traditional. Defensive stocks (low volatility, staples, utilities) have usually done better than most other equity indexes when the S&P 500 declined post-Covid, but like bonds, they lose ground to the S&P 500 on the upside. Still, it’s very rare to see a positive return during even the smaller 5%+ drawdowns. There is one surprise, although not much of one if you’ve been paying attention.

Energy has been both the most consistent performer (higher 40% of the time) and the best average performer. It’s also easily been the best performer over the entire period (9/2/2020–3/20/2026), and it’s not even close. The S&P 500 was up 92% over that entire period. The energy sector was up 343%. Next best among the equity indexes listed above was industrials at 115%. (What about technology? The tech sector was up 111% and the Nasdaq 80%, not even topping the S&P 500.) By the way, on the previous chart, the best performers over the whole period were gold (126%) and commodities (119%). The only other index listed that topped Treasury bills (18%) was leveraged loans (39%). I would add a similar caution to the above on energy. Energy underperformed for years in the second half of the 2010s following an extended period of capex overinvestment, and it pushed companies to clean up their balance sheet. The sector was well priced for a rebound if supported by the economic backdrop, and the backdrop we’ve had has been just about ideal.

The bigger point is we’ve seen an important regime change during the post-Covid expansion. Since Covid, we’ve avoided a recession, but rates have shot higher, inflation has been persistently elevated, and we’ve had several supply shocks. Is it over? We don’t think so. For now, we’re still in a period of inflationary growth. That means looking at diversification differently (“diversify your diversifiers”). That’s how we’re still positioned today, with reduced rate sensitivity within bonds and broader diversification beyond bonds using commodities, managed futures (a trend following strategy that invests in a range of assets via futures markets), and even diversifying internationally and incorporating lower volatility stocks. And in some cases, this isn’t even just about playing defense—there’s potential upside in that mix as well. But let’s not forget these are diversifiers. That’s important, but don’t forget that stocks broadly are a significant beneficiary of inflationary growth as well.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.

8900086.1. – 28APR26A