Over the last month, the market conversation has been so dominated by tariffs that it’s been hard to tune into anything else happening in the global economy. This is not to say that the newly implemented tariffs are insignificant—as I wrote recently, the tariffs are unprecedented and a big deal. But their impact on the economy is uncertain (we still don’t think there’ll be a recession) and the reality is that elevated interest rates (including mortgage rates) may ultimately be a bigger drag on the economy.

Markets obviously aren’t happy about tariffs, with the S&P 500 experiencing a 10% pullback from its February 19th high, the first 10% “correction” since October 2023. Most of the damage has occurred amongst the most cyclical areas of the market, and even last year’s technology high flyers. Usually when the US sneezes, the rest of the world catches a cold. But not this time. The MSCI Emerging Markets Index has only pulled back close to 2% during this period. Meanwhile, the MSCI EAFE Index, a proxy for developed markets outside the US, has gained 0.6%. This outperformance has been mostly driven by European stocks, with the MSCI Europe Index rising 1% since February 19th. This is in sharp contrast to US outperformance over the last 15 years (with 2017 a notable exception).

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Of course, we’re barely talking about one quarter here, and the question is whether this will be similar to 2017, when foreign stock outperformance faded just as people started thinking about diversification again. But there may be a reason to think “this time is different,” while recognizing that these are the four most dangerous words in investing.

Germany Wakes Up, and Unleashes a Fiscal Bazooka

Some background here is helpful. Germany’s constitution has something called a “debt brake,” which prevents the central government from taking on a lot of debt (restricting borrowing to 0.3% of GDP). Germany’s 16 states are also required to balance their budgets and prohibited from taking extra loans. No other major economy has such strict limits on borrowing. These requirements were introduced in 2009, though even before that Germany had a core philosophy that ran against taking on debt (perhaps due to scarring from hyperinflation during the 1920s Weimar Republic). In fact, this philosophy made itself into the foundation treaty of the European Union (EU) as well, with EU countries not allowed to take on debt over 3% of GDP (excluding interest payments).

Arguably, this made the post-2009 recovery tough, especially after the euro debt crisis hit in 2010. Europe was restricted by severe borrowing limits, and the one country with a lot of fiscal space, Germany (which had relatively lower debt-to-GDP ratio), refused to take on more debt. Note that Germany’s parliament made an exception to the debt brake after Covid hit, but this amounted to about 200 billion euros in 2021, which wasn’t enough to help.

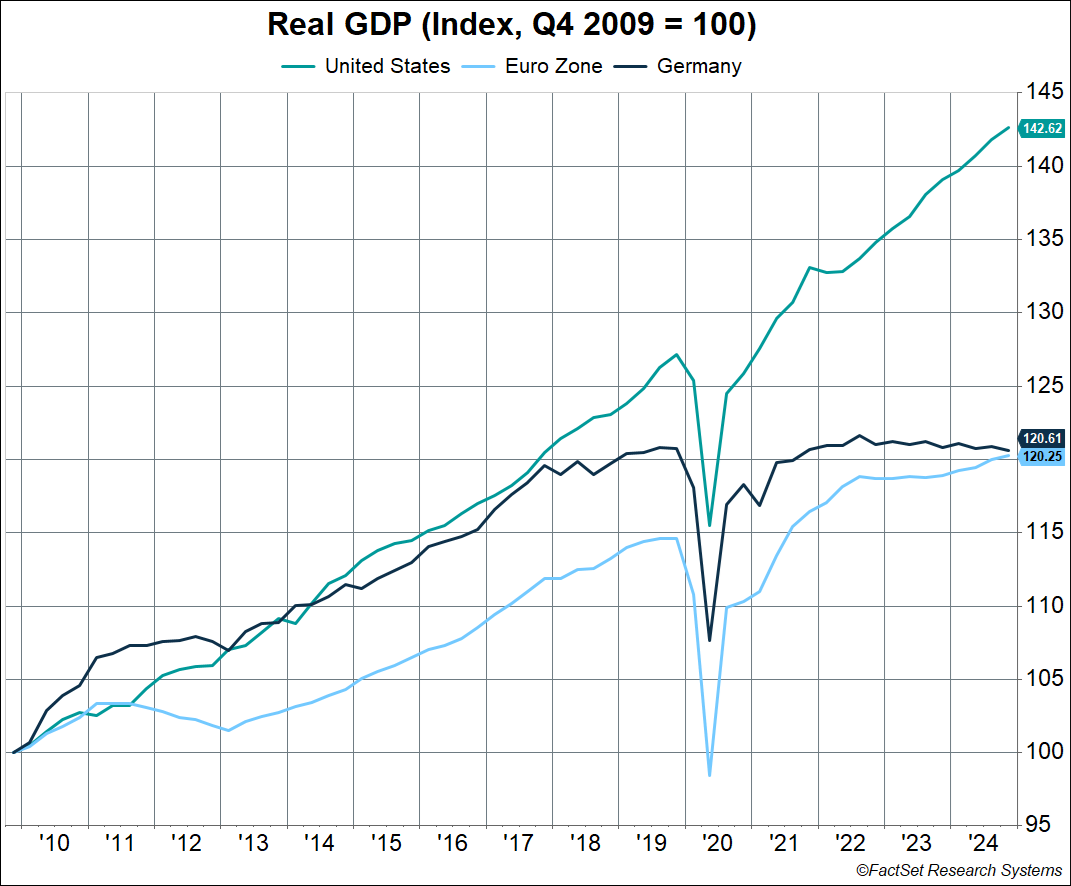

The chart below shows the huge contrast to what happened in the US versus the EU, and Germany. US fiscal spending supported the economy after 2009, and even more so after 2020, in sharp contrast to Europe. Over the last 15 years (2010-2024), here’s how real GDP grew:

- US: 2.4% annualized (+43% cumulative)

- EU: 1.2% annualized (+20% cumulative)

- Germany: 1.3% annualized (+21% cumulative)

Germany’s plight has actually been worse over the last seven years (2018-2024)—it’s barely grown during this time, with real GDP growth clocking in at 0.1% annualized during this period (look at the dark blue line in the chart below). That’s incredible—the third largest economy in the world has flatlined over the last seven years.

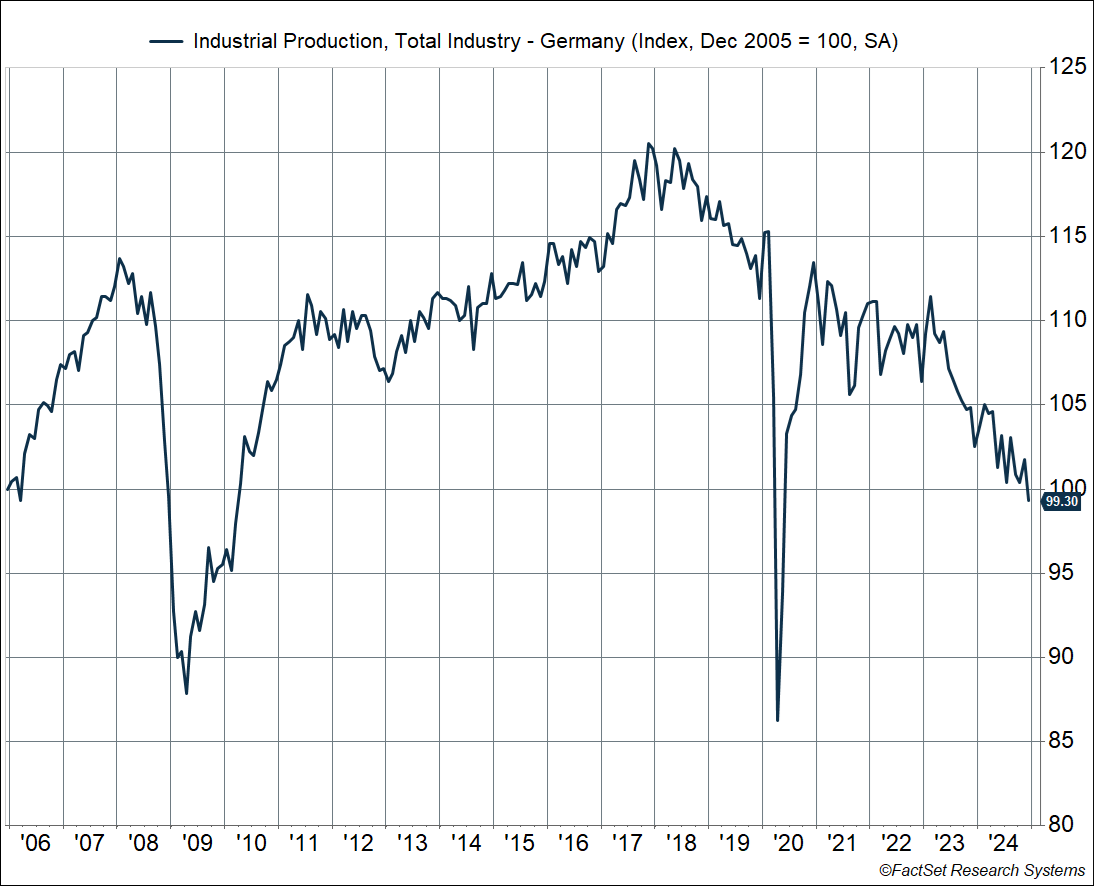

The problem is that German industrial production has collapsed since 2017—production is now lower than where it was in 2006. Remember that Germany is supposed to be an industrial powerhouse. These problems have been long standing, even across the 2010s, as you can see in the chart below. Russia’s invasion of Ukraine made things worse, as energy supplies were cut back. China has also taken over as a manufacturing powerhouse, especially autos, which has hit Germany’s key manufacturing industry. German infrastructure is also in bad shape.

On top of this, there’s rising fear that the Trump administration may peel away the security umbrella the US has provided for 80 years. There is also the threat of Russia inching closer to Germany’s doorstep if they gain Ukrainian territory amid a US-brokered deal.

All of this is why Germany’s incoming Chancellor, Friedrich Merz of the center-right Christian Democratic Union Party (CDU), announced plans to unleash a massive amount of fiscal spending, mostly focused on two areas, defense and infrastructure. In a breakthrough deal struck with his coalition partners, the Social Democratic Party (SPD) and the Greens, the plan is to “reform” Germany’s debt brake to unleash a fiscal bazooka, including:

- A huge boost for defense spending, with spending over 1% of GDP excluded from the debt brake

- A special 500 billion euro ($544 billion) fund for infrastructure, to be deployed over 10 years for transportation, energy grids, and housing

- Allowing Germany’s 16 states to borrow up to 0.35% of GDP above the debt limit

This is massive and the key here is that it’s not a one-off like during Covid. It’s a sustained wave of fiscal spending as I described to the Wall Street Journal recently, amounting to 10-20% of GDP over the next several years—akin to the US spending $3-$6 trillion of GDP. We could see German defense spending soar to 3% of GDP, which would be more than Germany’s entire fiscal deficit in 2024 (which was 2.8%). For perspective, US defense spending is about 3.7% of GDP, close to an 80-year low. The infrastructure package amounts to about 10% of GDP by itself.

Germany does have a lot of “fiscal space.” Government debt-to-GDP is just about 63%, about half of what it is in the US.

Of course, these plans have to pass through Parliament, but there’s a high likelihood of that happening. That’s a big deal for the global economy, let alone Germany and Europe. In short, the world’s third largest economy Is planning to unleash a massive, sustained wave of fiscal spending.

MEGA (Make Europe Great Again)?

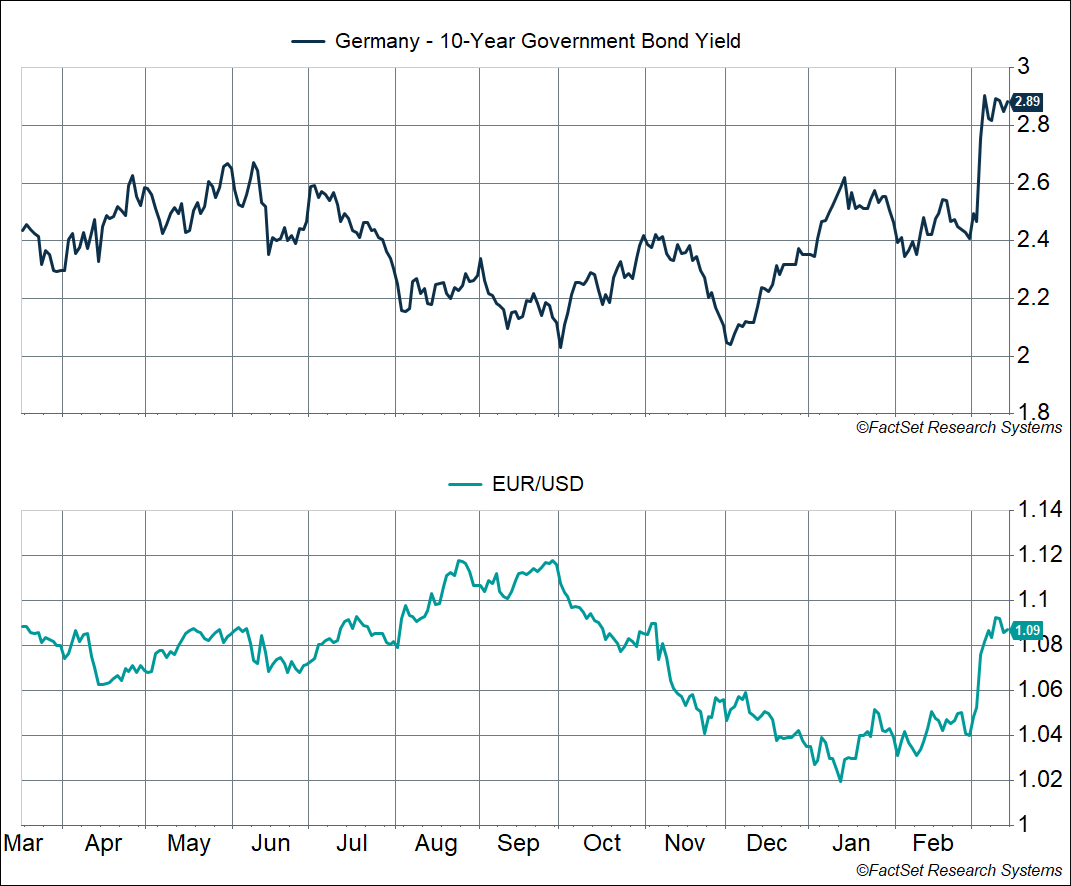

European markets saw mega (pun intended) moves after Merz announced their plans. The biggest move came in German bond markets, with the 10-year government “bund” yield surging by almost 0.4%-points over the two days following the announcement – the largest move since the aftermath of the fall of the Berlin Wall. This really shouldn’t be a surprise. Germany’s wave of fiscal spending means they’ll issue a lot more government debt, in contrast to the last couple of decades when German government debt has been really scarce because of the limited fiscal borrowing – this has implications for US treasuries too, which has really been the only readily available “safe asset” for a while now (since the US government has happily issued them amid massive deficit spending here).

Normally, a surge in yields would be concerning but this is likely coming on the back of higher economic growth expectations. Higher yields attractive capital and we saw a coincident surge in the euro, which surged close to 2% against the dollar after the announcement – the euro has now appreciated over 6% since it’s mid-January lows against the dollar.

To a first approximation, currency moves tend to reflect differential growth rates between countries (or region in the case of the euro). Two things have happened over the last two months, 1) US growth expectations have pulled back, and 2) Euro growth expectations have risen, especially on the back of Germany’s announcement. Though as you can see above, the euro is still well below levels we saw just six months ago, let alone 4 years ago when the EUR/USD was closer to 1.20.

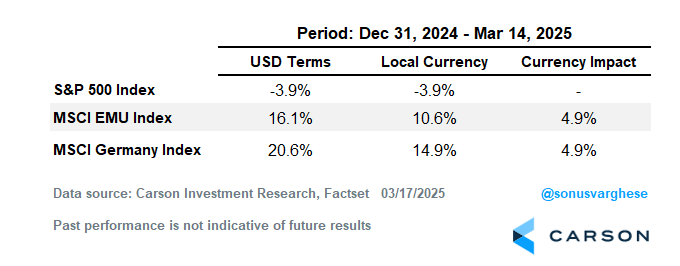

Keep in mind that an appreciating currency, and a lower USD, is also a tailwind for international equity investors (as we wrote in our 2025 outlook). For USD-based investors, this was just icing on the cake. The MSCI EMU (European Monetary Union) Index is up 10.6% year-to-date (through March 14th), but +16.1% in USD terms. This is on the back of a massive boost from the Germany – the MSCI Germany Index is up 14.9% in local currency terms, but +20.6% in USD terms. Meanwhile the S&P 500 is down close to 4% year-to-date.

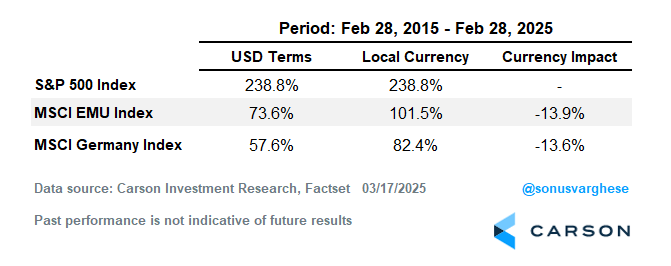

Of course, European equity markets have a lot of catch-up to do. Looking back over the last 10 years, the S&P 500 is up 239%. In contrast, the MSCI EMU Index is up 74% (USD terms) while the MSCI Germany Index is up only 58% (USD terms) – you can see how the euro has been a drag over the last decade amid a strengthening dollar, on top of local equity markets lagging the US.

As I noted above, “this time is different” are the four most dangerous words in investing. But we’re seeing significant policy changes in the US, and across the Atlantic in response (and perhaps even across the Pacific). These have the potential to completely reset how the global economy functions, by design and perhaps inadvertently too. This also has significant implications for markets (including for US treasuries as I pointed out above), and we could see more volatility as investors grapple with these changes. It does have us repositioning both our long-term strategic portfolios, as well as our tactical models, with European equity exposure brought up to neutral (we have been underweight for years). We remain overweight equities across all our models, but this is a time of significant uncertainty, and that’s why we want our portfolios to be as diversified as possible, without leaning too far one way or the other – within our equity allocation but also our diversifiers (including bonds, managed futures, gold, and even cash).

Happy St. Patrick’s Day! Carson’s Chief Market Strategist, Ryan Detrick and I celebrated by talking with Warren Pies, founder and portfolio manager at 3Fourteen Research – on Pi day no less (so we talked pies too). We covered a lot in a great discussion. Take listen.

7755459-0325-A