Looking at the equity market hitting all-time highs, you could be forgiven for thinking all is well. But you don’t have to look too far to see where there’s pain, by way of the bond market. We’ve been talking about an inflationary growth regime since the start of the year, and equities doing well while bonds struggle is par for the course in this environment. Still, it has been a particularly rough stretch for bond investors (and most people are bond investors with at least part of their portfolio).

Treasury yields surged late last week, but this was not a one-day event. Yields have been climbing across the curve since the U.S./Israel-Iran war began and the Strait of Hormuz was shut. From February 27, the eve of the war, through May 18:

- 2-year yields rose from 3.37% to 4.12%, an increase of 75 basis points (bps)

- 10-year yields rose from 3.94% to 4.67%, an increase of 73 bps

These are significant moves, and they’ve come about in a relatively short period of time.

The Front End of the Yield Curve Says the Fed Is Behind

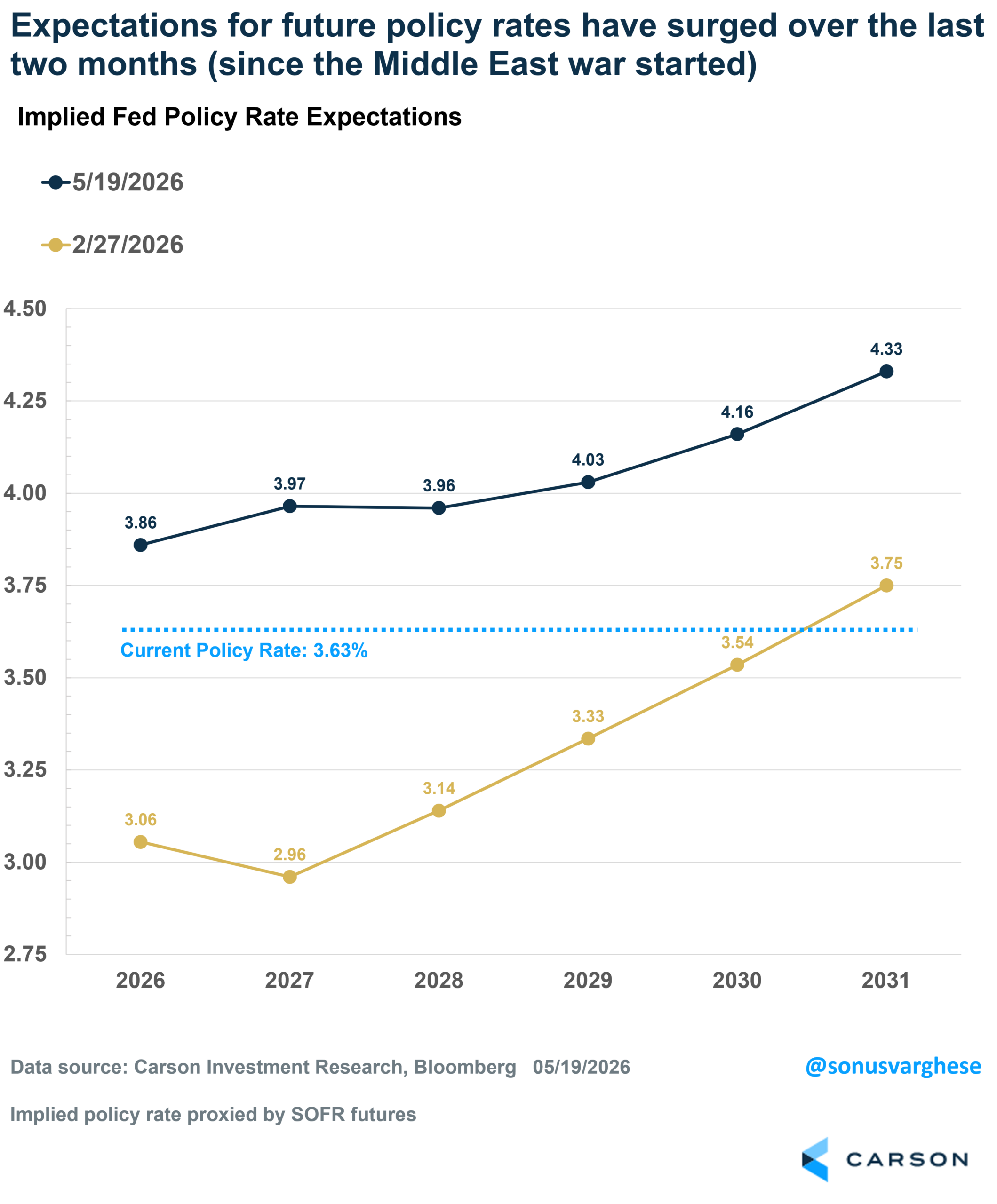

The 2-year yield at 4.12% means that the market expects the short-term policy rate to average that level over the next two years, well above the current policy rate of 3.63%.

In fact, the probability of a rate hike in 2026 has increased to over 60%, making a rate hike this year the base case (barely so, as anything between 35-65% is really a coin toss). Here’s a chart showing market expectations for policy rates over the next several years.

On the eve of the crisis, markets were expecting a couple more rate cuts this year, taking the policy rate to almost 3%. Markets did expect a series of rate hikes from 2028 onwards, but gradually, with the policy rate exceeding its current level only in 2031.

The entire curve has now shifted above the current policy rate of 3.63%, implying markets now expect the Fed to hike rates this year and continue lifting them beyond 2026.

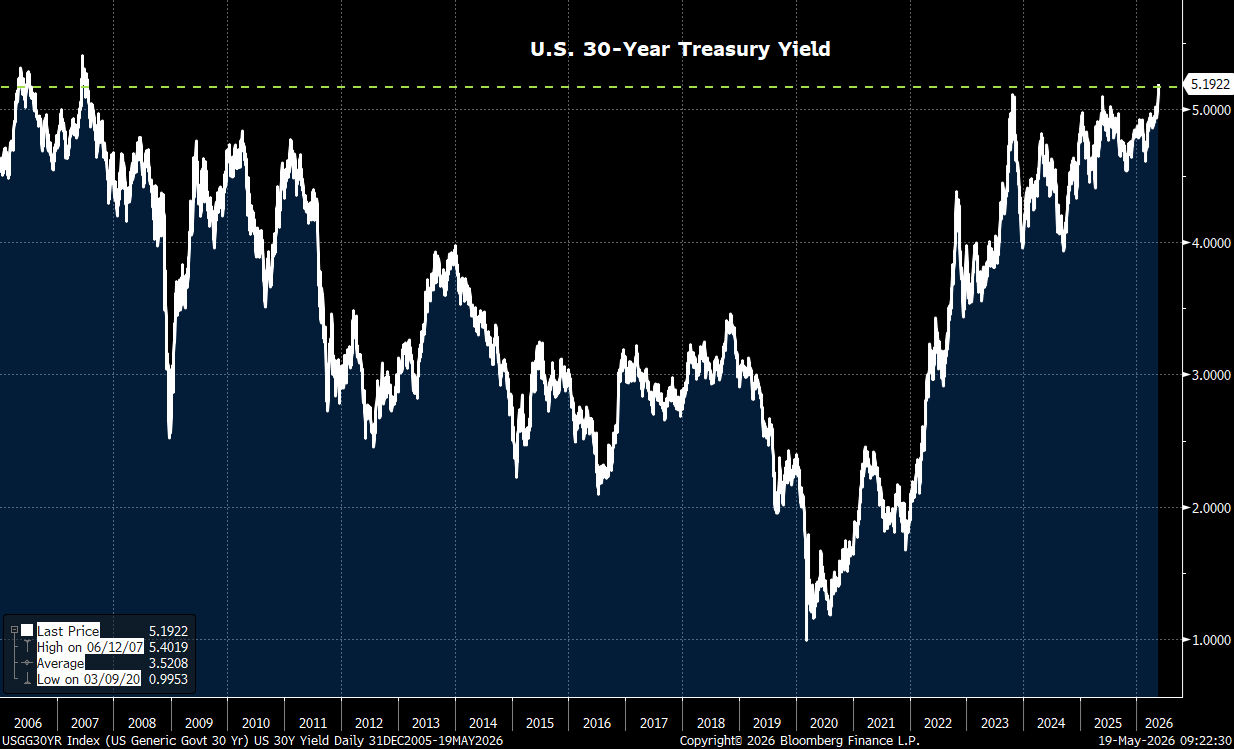

In other words, expect rates to stay higher for longer as the Fed looks to get a grip on inflation. Hence it shouldn’t be a surprise that even long-term rates are rising. On the other end of the yield curve, the 30-year Treasury yield has hit 5.19%, the highest level in 30 years. It was 4.61% on the eve of the war.

The bond market clearly doesn’t like elevated inflation, which is why yields are rising. But there’s also the prospect of falling demand from abroad.

Why Yields Jumped Last Week

Long-term yields are rising for two broad reasons. First, inflation risks are moving higher. Second, demand for Treasuries looks less reliable at the margin, especially as foreign government bond yields rise. To be clear, the Treasury selloff began well before Friday. Yields have been rising since the war began, which points to the bigger driver: oil prices, the Strait of Hormuz, and the inflation impulse that follows (I discussed this in a blog last week). But the sharp move late in the week had two immediate catalysts:

- Japan’s central bank is signaling that more rate hikes may be coming as inflation surges.

- The Strait of Hormuz remains shut, with the U.S.-China summit failing to produce additional pressure on Iran to reopen it.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

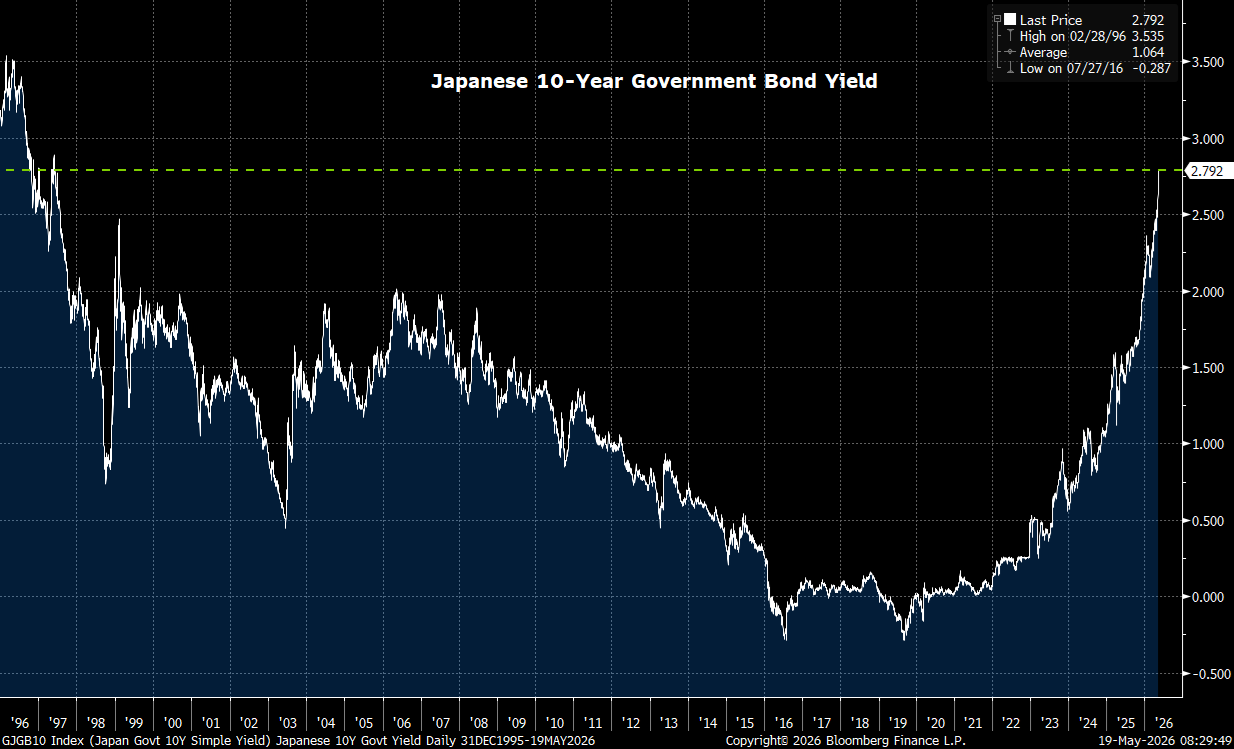

Japan Still Matters

Let’s start with Japan. Japan’s wholesale price inflation, as measured by PPI, surged 2.3% month over month in April, the fastest pace in three years. Expectations were for a 0.7% increase. Instead, prices jumped on the back of higher energy and chemical product prices. The year-over-year pace rose to 4.9%, the fastest since May 2023.

That raised the odds of another Bank of Japan (BoJ) rate hike, with markets pricing a 75% probability of a move by June. One BoJ policymaker called for raising rates “at the earliest stage possible.” The 2-year Japanese government bond yield hit 1.43%, well above the current policy rate of 0.75%. Translation: markets think the BoJ is behind the curve. That is a striking shift from 2022, when inflation spiked, but the 2-year Japanese yield was still below zero. Meanwhile, the 10-year Japanese government bond yield surged to 2.80%, the highest level since 1997. For perspective, the 10-year yield was below 0.25% in 2022, when yield curve control was still in place.

One crucial difference between what’s happening now and the 2022 inflation episode is that we now have significant fiscal stimulus in the works as well, from the relatively new Japanese government headed by Prime Minister Sanae Takaichi.

So, How Does a Move in Japanese Yields Affect U.S. Treasury Yields?

The simplest answer is that higher foreign yields reduce demand for Treasuries at the margin. Japanese investors were starved for yield for years, and that helped support demand for U.S. Treasuries, especially when Japanese and European yields were negative. That world is gone.

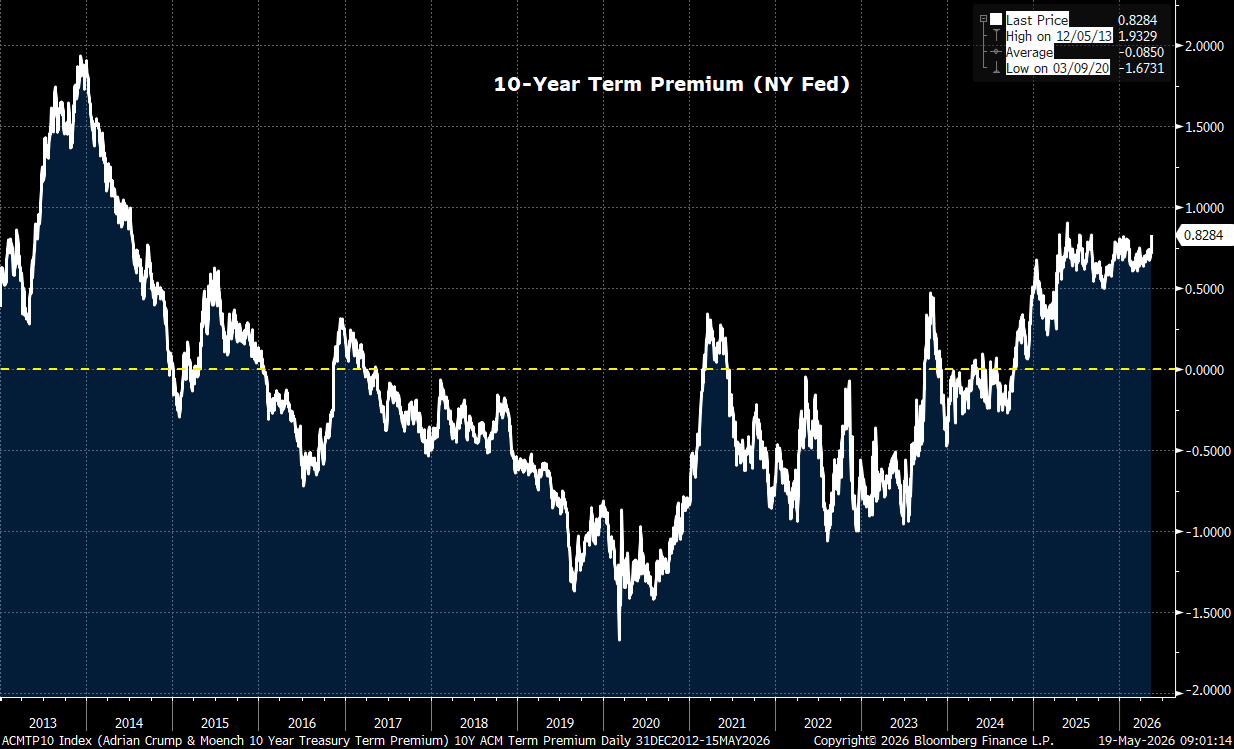

This shows up most clearly in the U.S. term premium. The term premium is the extra compensation investors demand for holding a long-term bond instead of rolling a series of short-term bonds. It reflects inflation uncertainty, but also supply and demand. Right now, the U.S. deficit is running near 6% of GDP, which means Treasury supply is large. At the same time, foreign yields are rising, which reduces the relative appeal of U.S. Treasuries.

The term premium is not directly observable—it has to be modeled. But the New York Fed’s model shows the 10-year term premium is now above 0.80%, close to the highest level in more than a decade.

This is a big regime change. After 2014, the term premium collapsed and eventually turned negative between 2016 and 2020. A negative term premium is odd on the surface. Why would investors accept less compensation for owning a long-term bond rather than a series of short-term bonds? There were two big reasons:

- Inflation was low, and inflation volatility was even lower.

- Demand for Treasuries was enormous, including from foreign buyers and from investors using bonds as a portfolio diversifier when the stock-bond correlation was negative.

The term premium rose after 2020 as Treasury supply surged amid fiscal stimulus, but it dipped back below zero in late 2021 and stayed there even during the 2022 inflation spike. It was only in late 2023 that it decisively moved back above zero. It’s moved higher over the past year, and especially recently.

When the term premium rises, it usually reflects one or more of three things:

- Higher inflation volatility

- Excess Treasury supply

- Lower demand for Treasuries

We have all three right now. That is the problem.

Closed Strait = Higher Oil Prices = Inflation Problem

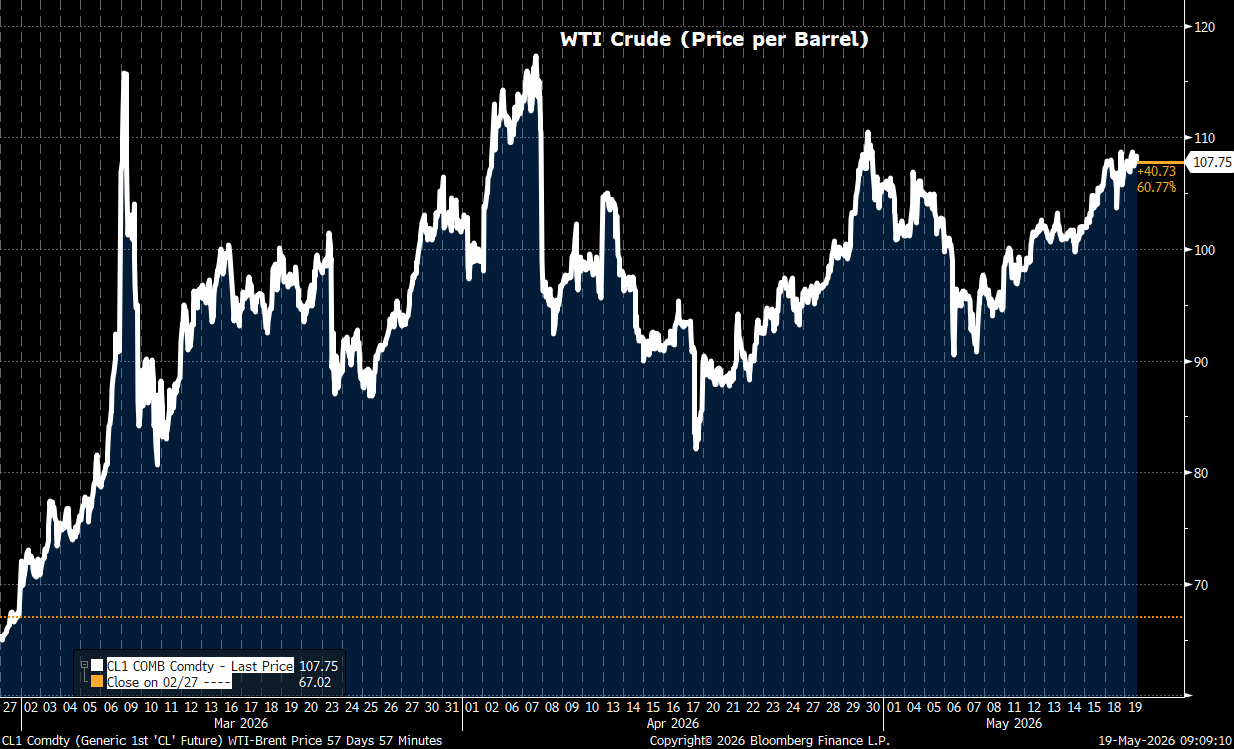

The Strait of Hormuz remains shut, and oil prices are back above $100/barrel. That reverses a big chunk of the decline that followed ceasefire headlines and more constructive signals around U.S.-Iran talks. WTI, the U.S. benchmark, is back above $107/barrel, the highest level in weeks. (It was $67/barrel on the eve of the war.) Brent, the European benchmark, is also back above $110/barrel (up from $72/barrel on the eve of the war).

Higher oil prices mean higher inflation, and higher inflation means higher yields. It really is that simple.

The problem on Friday was that the U.S.-China summit produced no progress on the Middle East front. There was hope that China might pressure Iran to reopen the Strait. That did not happen. China said it wants oil flowing again, but it appears comfortable with Iranian control of the Strait, including the possibility of Iran charging ships a toll to pass through. That remains unacceptable to the U.S., at least for now.

The Bottom Line

The Middle East stalemate continues. And with each passing day, global oil reserves are being drawn down, including in the U.S., which is drawing oil from its Strategic Petroleum Reserve (SPR) at a record pace. That’s keeping a bit of a lid on oil prices, but as you can see, prices are creeping higher the longer this goes on. The likelihood of the inflation problem growing even larger increases as a result, which is why bond yields are surging.

To put a bow on all this, the main takeaway is that the bond market is absorbing the cost of higher inflation. Equities remain strong because we have inflationary growth (rather than stagflation). Nominal GDP growth is running hot, and that benefits corporate revenues and profits. AI-related capex is another tailwind, though this is also pushing inflation higher, as I wrote last week, and putting more upward pressure on bond yields. For now, a Fed led by incoming Chair Kevin Warsh looks set to look past this immediate bout of inflation and let things run hot. We’ll see how long the bond market allows him to remain comfortable with that stance.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

8936378.1. – 19MAY26A