Last week, Citrini Research and Lotus Technology Management’s Alap Shah published a piece on AI that went viral, titled: “The 2028 Global Intelligence Crisis.” The piece is a thought experiment that highlighted some potential consequences of rapid AI development (even if not base case) that the conventional view might be missing. They wrote a memo as if we were in June 2028, focusing on the impact of abundant intelligence (the artificial kind) on the global economy and markets.

Some highlights from their “future” memo:

- S&P 500 in a 38% drawdown from October 2026 highs

- Economy in a deflationary spiral, and a recession started in Q2 2027

- Unemployment rate at 10.2%

- Nominal GDP printing mid-to-high single-digit annualized growth

- Fastest productivity growth (real output per hour) since the 1950s

- Owners of compute saw wealth explode as labor costs vanished

- A collapse in real wage growth

They discuss something called “ghost GDP,” which is output that shows up in national accounts but never circulates through to the real economy.

Legacy software companies weren’t the only immediate casualties. Most of the consequences of abundant AI involved the replacement of intermediaries in our daily life, whether it was Doordash, real estate brokers, financial advisors, CPAs, insurance agents, and generally companies who relied on passive renewals (whether it was health insurance or cable service). AI made it easy to replace all of this with repeated optimization for price and fit, and prices (and profit margins) plunged. Even credit card companies like Mastercard weren’t immune, as AI agents looked to eliminate the 2-3% interchange fees by using stablecoins. Revenue models of consumer finance companies like American Express and others were also gutted.

As they write (and I’ll come back to this):

“We had overestimated the value of “human relationships”. Turns out that a lot of what people called relationships was simply friction with a friendly face.”

Meanwhile, capex spending continued to stay strong, increasing at the expense of operating expenditures (OpEx) as companies slashed labor costs and funneled most of the savings into more capex. As a result, AI infrastructure companies continued to flourish, with countries like South Korea and Taiwan benefiting.

On the other hand, displaced white collar workers downshifted and found lower-paying service sector jobs and gig work, increasing supply there and lowering wages. This meant incomes dropped. The top 20% of earners accounted for ~ 65% of consumer spending in the US and so consumption took a hit, as did the $13 trillion mortgage market.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

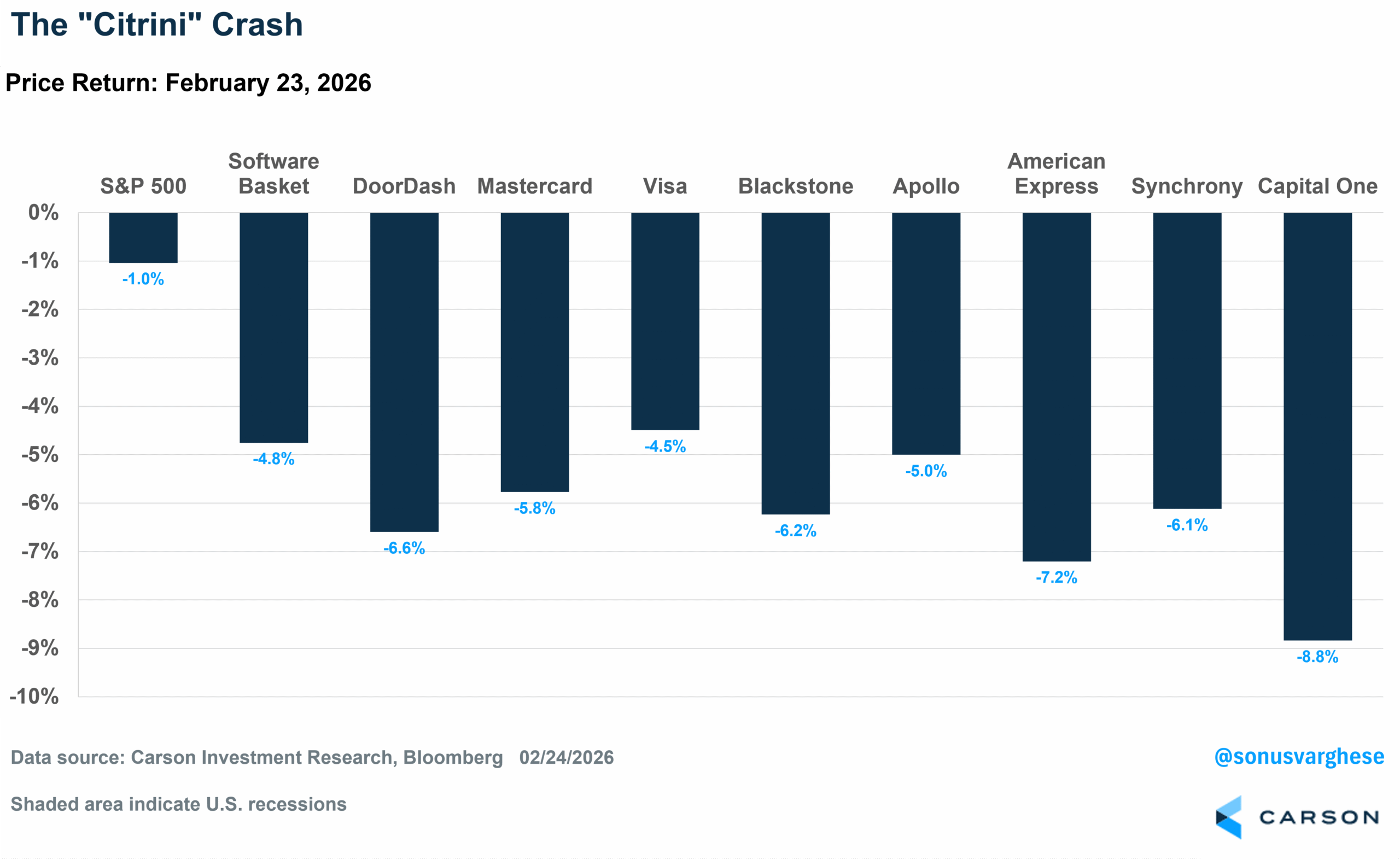

Market Reaction: Sell First, Ask Questions Later

A lot of stocks took a beating this Monday (February 23rd) as investors digested the report. Here’s what happened to share prices of a few companies explicitly mentioned in the report, along with a basket of software stocks and the S&P 500.

This Is Fiction (Yes, Really)

The report was essentially a work of fiction. Don’t get me wrong—it was a fascinating read and quite thoughtful as far as scenario analysis goes. I do recommend reading it. Citrini was also careful to note that this was not their base case or meant to be doomer fiction, but a way to highlight potential tail risk.

Still, I have a lot of “quibbles” with the piece and a lot of it has to do with internal macro inconsistency. Sort of like saying 2 + 2 = 0 or 2 + 2= 5.

The first thing that jumps out is that they say the economy is in the middle of a deflationary recession and real wage growth is collapsing. However, productivity growth is surging, and nominal GDP growth is running between 5-10%.

This doesn’t compute.

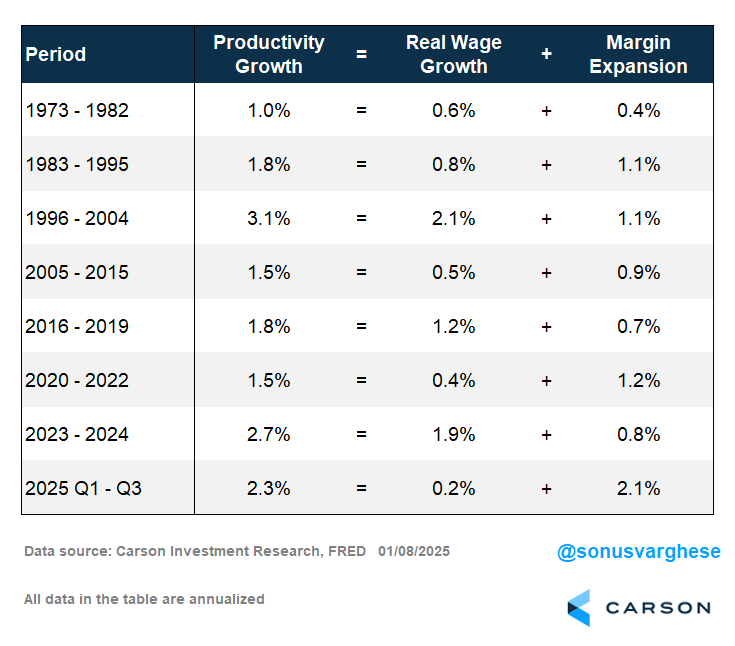

Productivity growth is essentially the sum of “real” or inflation-adjusted wage growth and margin expansion. In other words, companies can pass through productivity gains to workers (in the form of higher wages) or they can take it all and boost profit margins (which will reduce worker’s share of total income). Expanding margins will also show up as inflation and drive real wages lower (since real wage growth is nominal wage growth minus inflation).

Historically, we’ve seen a combination here in the US. The table below shows the math using historical macroeconomic data. During periods of above-trend productivity growth (1996-2004 and 2023-2024), real wages also rose faster than in other periods. In other words, firms didn’t eat up all that productivity growth with margin expansion. A big chunk of that productivity growth passed on to workers too. These were periods of tight labor markets, and strong income growth in turn translated to a positive feedback loop of strong demand and strong profit growth.

Interestingly the one period when productivity ran quite strong (> 2%) but real wage growth was poor was the first three quarters of 2025. Almost all the productivity growth went toward boosting margins. This was also a period in which the labor market cooled, though because of economic uncertainty amid the tariff chaos, and inflation also picked up (also partly because of tariffs). At the same time, this is just three quarters of data and short-term data can be noisy (and subject to big revisions).

All this to say, the historical precedent is that strong productivity growth on the back of technological innovation coincides with strong labor markets—the unemployment rate goes down and wage growth is strong, which boosts demand and profits.

In contrast, the Citrini report argues that companies are in fact going to eat up all the productivity gains and boost margins without workers seeing any benefit. That’s not happened before and I find it extremely unlikely.

Who’s spending and Driving Profit Growth?

Now, maybe all the AI “winners” will spend more on capex and less on OpEx (as they let go of workers) as the authors assume, and that capex translates into revenue and profits for other companies.

But where does profit growth come from?

Aggregate demand would have to increase for that to happen and if firms are growing capex, presumably there’s more demand for AI agents. But what’re they going to do if there are a lot of people unemployed and not buying stuff? Sure, the owners of the machines will have a lot more money, but how much more can they spend than they already do? And why would they bother investing even more money in machines? They’ll pull back, and that’ll pull economic growth lower. Yes, the economy has a lot of productive capacity, but that won’t be deployed and GDP growth will not be running around 5-10%.

The other side of this is that a lot of hyperscalars have massive cash flow generating ad businesses (Alphabet, Meta, and even Amazon) and enterprise software businesses (Microsoft, Oracle). Unemployed workers will clearly have more time to do Google searches or browse Facebook, Instagram, and Amazon, but if they can’t afford to buy stuff why would advertisers spend money on these platforms? Ad sales would crash. On the enterprise side, let’s assume AI has killed the likes of Excel and Powerpoint, and some agentic code has come up with a new “free” version of these tools.

That begs the question: how is new capex growth being funded?

Perhaps with debt. But the authors also tell us that the private credit market, which is the go-to place for debt-financing of AI infrastructure, is dead.

This doesn’t compute.

Let’s take another angle, from the GDP side of things and connect things to the stock market.

If Aggregate Profits Surge, Why Is the Stock Market Down?

If nominal GDP growth is clocking in at 8%, and we have deflation, then real GDP growth would have to be higher than that. Real incomes, i.e. nominal income minus inflation, should be growing. But the authors say that real wages are collapsing. Presumably, even as deflation makes things cheaper, nominal earnings are falling even faster. A former lawyer is now driving an Uber and delivering pizza, which barely pays anything because AI has left 100 other potential drivers in the neighborhood on standby, also ready to deliver pizza.

Gross Domestic Income (GDI) is simply another way to calculate GDP and just over 50% of that is worker compensation. If GDI is growing 8%, that would mean worker compensation would have to be rising close to that pace.

OK, maybe all of it is going to corporate profits, but right now corporate profits make up less than 10% of GDI (things like taxes, interest income, rental income, small business income, and depreciation make up the rest of GDI). If GDI was up 8%, corporate profits would have to surge over 80%, assuming everything else including employee compensation was flat and even more than that if employee compensation fell, which presumably would be the case if the unemployment rate was at 10%.

Let’s take the extreme case and say that’s plausible. But if aggregate profits surge at such a fast pace, why would the stock market be in a steep drawdown?

Stock market returns are the sum of profit growth and multiple expansion (or contraction), plus dividend growth (which are profits distributed to shareholders). If market returns are deeply negative while profit growth is surging, that would imply multiples have been crushed, which would happen if interest rates surged.

With nominal GDP running between 5-10%, you’d expect interest rates to be well above where they are now. BUT they’re also saying there’s deflation as prices crash on the back of AI agents running price optimizations 24/7. So why would interest rates surge?

This doesn’t compute.

What About the Policy Response?

One thing the report doesn’t address is the policy response, except in a backhanded way by saying that the government’s ability to stage any sort of rescue has dwindled.

With the unemployment rate running at 10%, you’d think the Federal Reserve would’ve taken rates to zero. In fact, if we have persistent deflation, even the zero bound would be “too tight” as real interest rates (nominal minus inflation) remain elevated. Presumably, the Fed would have to take rates negative in that event.

Meanwhile, across the road Congress and the White House wouldn’t be sitting still. Some sort of relief package for households would be passed, with the goal of putting money in people’s pockets. And why not, since the government can fund spending at negative rates.

Perhaps the government even takes stakes in the AI-infrastructure companies and gets a share of the profits, which are subsequently passed through to households. This is not a hard scenario to imagine given the number of companies the current administration has taken a stake in over the past year (including Intel and U.S. Steel).

But if households are going to get money, presumably they’ll spend it. And one person’s spending is another person’s income.

That’s going to boost demand, including for stuff that has to be produced. AI can disintermediate the intermediaries, but goods and services still must be produced, which means there will be need for workers who can produce this stuff.

Interestingly, one place where we have a very lite version of the Citrini scenario is China. Technology has been advancing rapidly, and the economy is driven by investment spending, even as household consumption pulls back. Real estate has crashed and so Chinese households are reluctant to pour savings back into that sector. Youth unemployment is around 17% as it becomes harder to find jobs. Inflation is close to zero. There’s no policy support and safety net, at least not to the degree here in the US (and other countries). The key difference is that China doesn’t have a democratic system, in contrast to the US and other countries. Perhaps the current crop of lawmakers are out of ideas but I don’t think we should underestimate the ability of people to push back and ultimately push lawmakers to act, or they’ll elect others who will.

While we shouldn’t underestimate the ability of businesses to adapt and reinvent themselves (and the economy as a result), that applies even more so to people. And that applies to politics as well in a democracy.

Stuff Still Has To Get Made

As one X commentator pointed out, the point of the economy is to satisfy human desires, and that’s never ending. Technology can perhaps check off the current list of desires, but news ones will crop up and somebody has to cater to that.

In any case, the Citrini piece is not even arguing that technology will in fact produce goods and services in lieu of humans. Rather, it’s about taking out the “middlemen,” i.e. taking friction out, and reducing associated costs. But that’s a good thing. It’s unlikely that reducing friction and improving efficiency makes us all worse off, rather than better off. If I have to pay DoorDash less for food delivery, fantastic—I’ll have more money in my pocket which I can use to buy another order of egg rolls. But then somebody must make egg rolls in the restaurant. Same thing if I can pay less for cable service, as I can use the money I save for something more useful.

For businesses, cost savings associated with these frictions being eliminated (for example: having more flexibility with a software contract) will likely translate into better and more efficient processes, including augmenting with AI tools.

At the same time, some of the friction we experience in our lives, even when it comes to an apparent transactional relationship in our business or personal lives, is about trust and confidence. That’s why we accept that friction and likely don’t even see it as a “cost,” whether it’s trusting a good team of lawyers and M&A consultants to help you sell your business and retire or working with a financial advisor to ensure a stress-free retirement.

A More Realistic Scenario?

None of what I said above implies that things will go smoothly. We’ll likely see displacement of workers, perhaps akin to the China shock (which led to a manufacturing downturn in the industrial Midwest), but this is where policy can make a difference. We’re also likely to see a lot of capital re-allocation and rotation, which will cause volatility.

What is more realistic is something we wrote about in our 2026 Outlook: Ride the Wave. We’re currently seeing a massive amount of AI-related capital expenditures driven by large tech companies. I wrote about this in a recent blog. The boom has led investors to draw parallels with other historical periods in which private firms made massive capital outlays to build the infrastructure for transformative technologies—railroads in the 1870s and the internet in the late 1990s.

You don’t have to be a student of history to know what happened with the railroad and internet booms. Railroad stocks rose about 50% before collapsing. Telecom stocks rose 400% in the late 1990s before crashing. The internet boom is not the only economic boom we’ve seen over the last few decades. In fact, just after the internet boom/crash, we got the housing boom from 2003-07 (which was also a financial sector boom, including areas like real estate and insurance). Then we also got a mini-energy boom amid the shale revolution from 2012-15.

The dynamics are similar across these booms. Historically speaking, the promise of new technology pushes firms to make massive investments. Investors like that, and stock prices soar, which in turn facilitates even more investment. But ultimately, demand fails to keep up, and there’s excess supply, although that ultimately benefited society, whether it was railroads, high-speed internet that allowed us to connect as never before (and stream cat videos), new housing to meet the demand of the next generation, or cheap oil. Overcapacity leads to lower stock prices and lower valuations, and investment spending reverses.

Economic growth then takes a hit as the boom leads to a bust. It’s not like any of these areas—tech in the late 1990s, housing/finance in the mid-2000s, energy in the 2010s—were large parts of GDP. But when they were booming, GDP growth benefited, but when the boom ended the flipside was a sharp swing in the other direction.

This is where I think the risk with AI-related job losses lie. If (when?) we do get the next recession, possibly on the other side of a capex bust, we could see a “jobless” recovery as companies employ more AI tools and don’t rehire as many workers as they had during the boom.

But that’s further down the road in our view. As we wrote in our Outlook, we don’t think the negative part of the cycle is a 2026 story, or even necessarily a 2027 one. Right now, AI demand is clearly rising, and that’s boosting the need for AI infrastructure. If anything, there’s not enough supply (including for things like memory chips, and energy) and that’s inflationary.

That’s essentially why we have positioned our tactical, and even strategic, portfolios for an inflationary growth scenario. We want to ride the AI boom, but don’t want to overextend ourselves on that theme with concentrated positioning. In other words, we’re definitely not betting on the Citrini tail scenario that would actually lead us to bet more heavily on AI-infrastructure companies.

For more content by Sonu Varghese, Chief Macro Strategist click here.

8796525.1. – 27FEB26A