When we wrote our 2026 Outlook: Riding The Wave, one thing we had in mind was surfing the artificial intelligence (AI) wave, not necessarily through immediate productivity gains or direct AI corporate profits, but through the massive infrastructure buildout it required (which does support broad corporate profits). As we noted then, this is a big one – something massive is happening in the economy. Large tech companies are driving a historic wave of capital expenditures to support AI, especially those that provide large-scale cloud compute capacity and operate hyperscale-level data centers (Microsoft, Alphabet, Amazon, Meta, Oracle).

As it turns out, the wave is even bigger than we thought it would be.

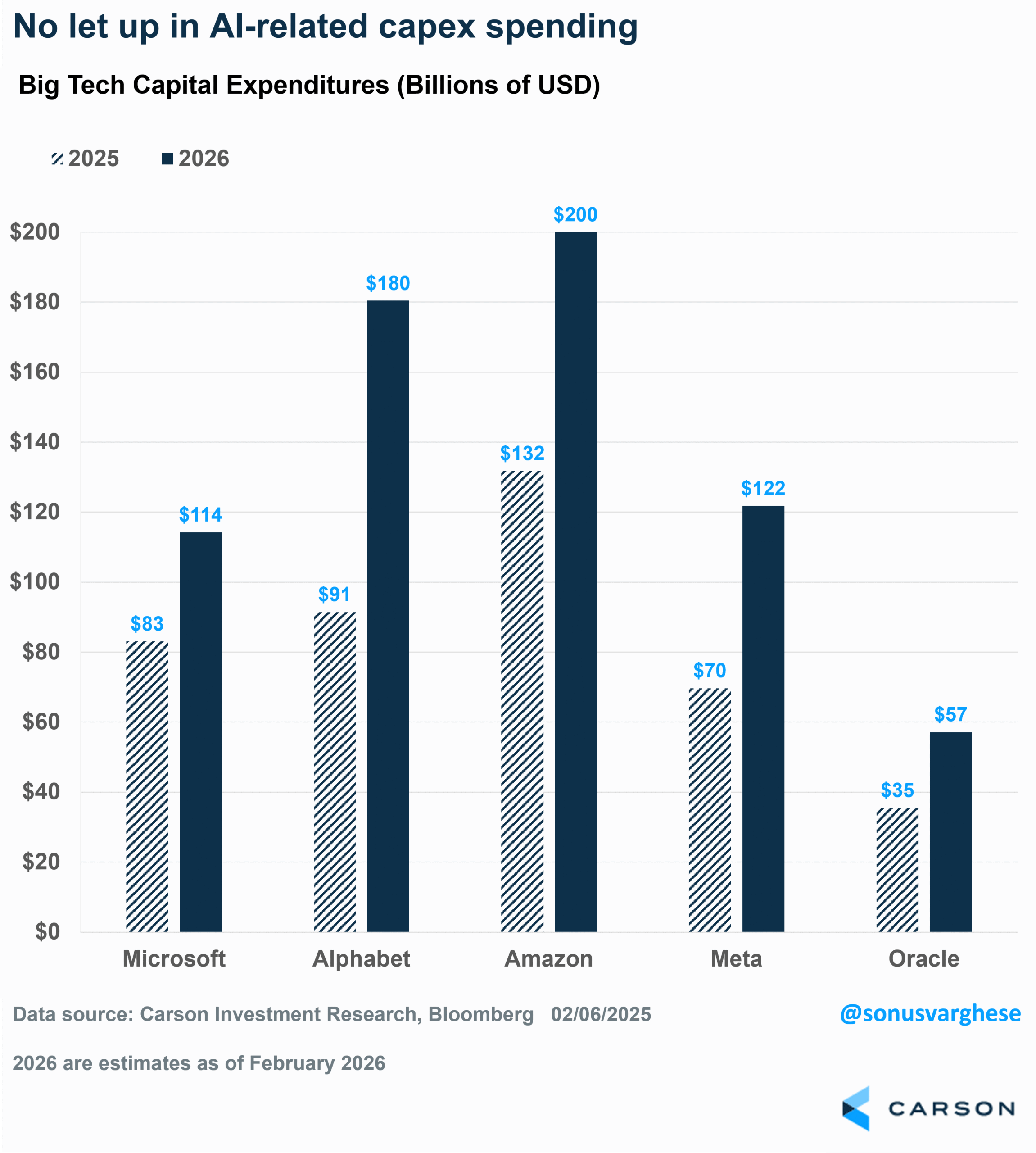

The big tech firms recently reported earnings and they’re ramping up capex to even larger levels. The three big ones:

- Alphabet: 2025 capex was $91B and they expect $180B in 2026 (analyst estimate 2 months ago was $115B).

- Amazon: 2025 capex was $132B and then expect $200B in 2026 (analyst estimate 2 months ago was $144B).

- Meta: 2025 capex was $70B and they expect $122B in 2026 (analyst estimate 2 months ago was $108B).

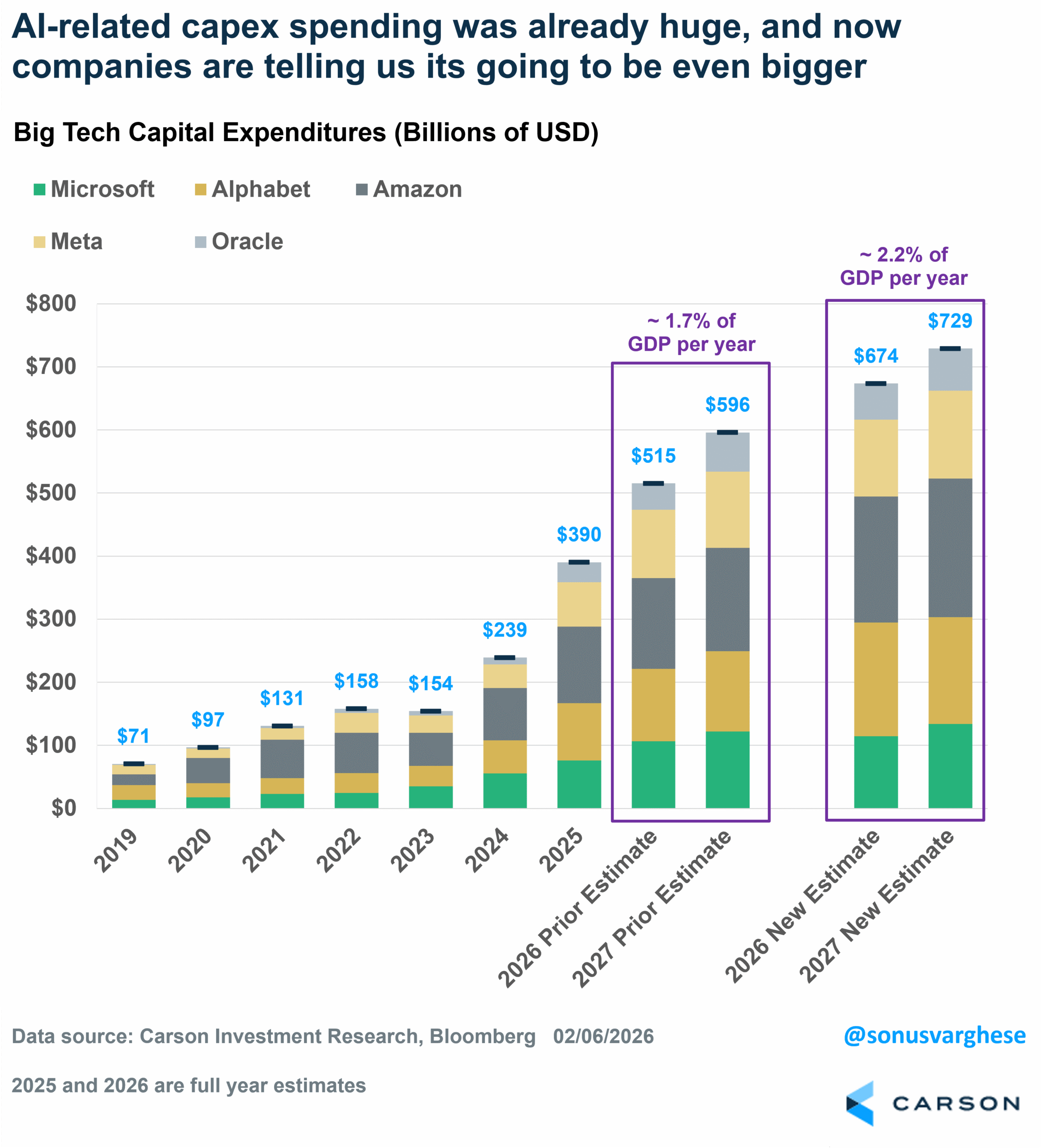

When we wrote our 2026 Outlook, we estimated that these firms will spend a total of $515B on capex in 2026, up from almost $400B in 2025. That amounts to about 1.6% of GDP, which is staggering.

The most recent updates take the 2026 capex estimate to a whopping $674B, which is about 2.2% of GDP (2027 is expected to be similar) – that is over 4x the level of capex in 2023 (0.5% of GDP) and 7x the size of where it was in 2019 (0.3%).

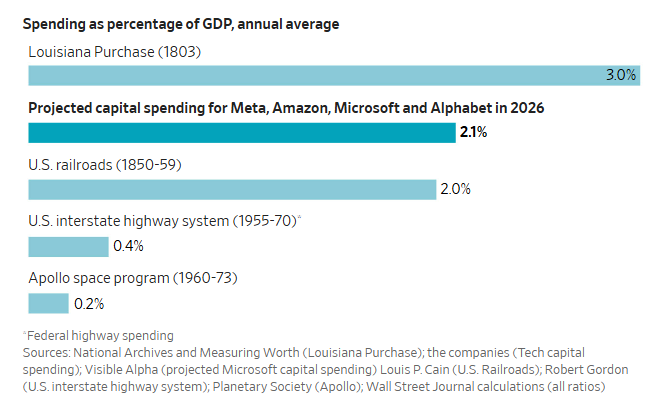

Here’s a nice chart from the Wall Street Journal comparing the scale of the capex spending to prior capital efforts in US history. Expected 2026 AI capex is about the size of the US railroad buildout, 5x the interstate highway buildout, and 10x the cost of even the moon landing! Yes, it’s fair to call the collective AI spending a “moonshot” effort at ramping up a transformative technology. Note that this compares just 2026 capex to the entire level of capex for these other projects across multiple years.

But Investors Are Worried

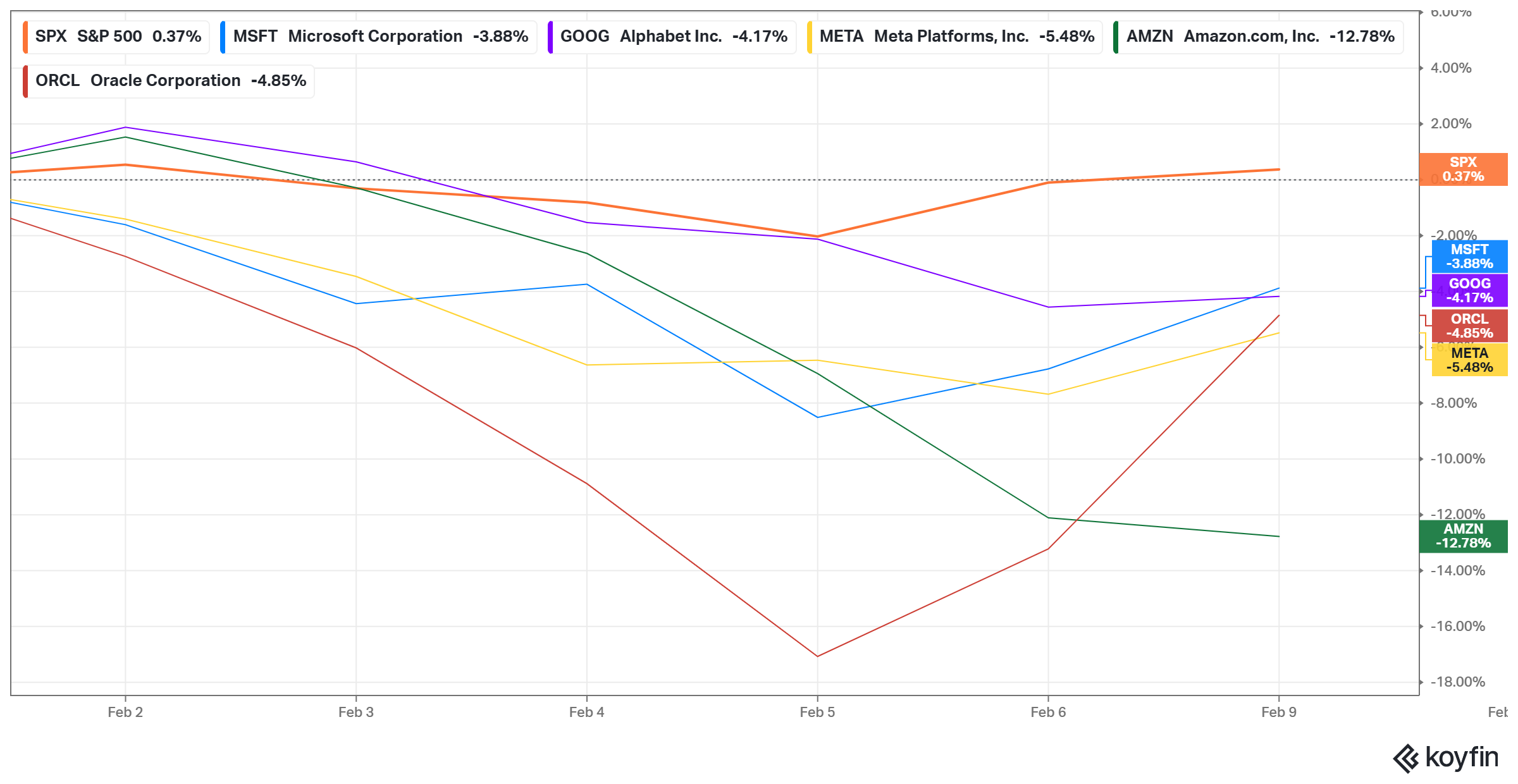

Sentiment toward all this capex spending has clearly turned a corner (for now), and the contrast to last year is striking. Last year investors seemed thrilled about all the capex spending, but the reaction was different last week during earnings. Since the end of January through February 9th, the S&P 500 has gained about 0.4%, but that’s come despite pullbacks across big tech (the following five companies make up 18% of the S&P 500 Index):

- Microsoft fell 3.9%

- Alphabet fell 4.2%

- Oracle fell 4.9%

- Meta fell 5.5%

- Amazon, which announced the largest amount of capex amongst the group, fell 12.8%

The pullbacks are even steeper when you look at how far below 52-week highs these companies are. Keep in mind that the S&P 500 is less than 0.2% off its 52-week high. As of February 9th:

- Alphabet is 7.4% off its 52-week high.

- Meta is 15% off its 52-week high.

- Amazon is 19.3% off its 52-week high.

- Microsoft is 25.5% off its 52-week high.

- Oracle is 54.7% off its 52-week high (not a typo!).

Note that the big chip companies aren’t faring much better either

- Nvidia is 10.4% off its 52-week high.

- Broadcom is 17.1% off its 52-week high.

- AMD is 19.1% off its 52-week high.

One risk here is quite obvious. These tech companies are moving from an asset-lite model, where they had enormous amounts of free cash flow, to an asset-heavy model that involves directing the cash towards capex. And they’re doing it quickly. The hyperscalars are now spending 65% of gross profit on capex. Compare that to:

- An average of 33% across 2023-2024

- An average of 27% across 2017-2022

For perspective, Boeing spends about 69% of gross profit on capex, while Exxon-Mobil spends 62% and Ford spends 60%, so those former “asset lite” technology companies are now matching the spending level of well-known capital-intensive businesses.

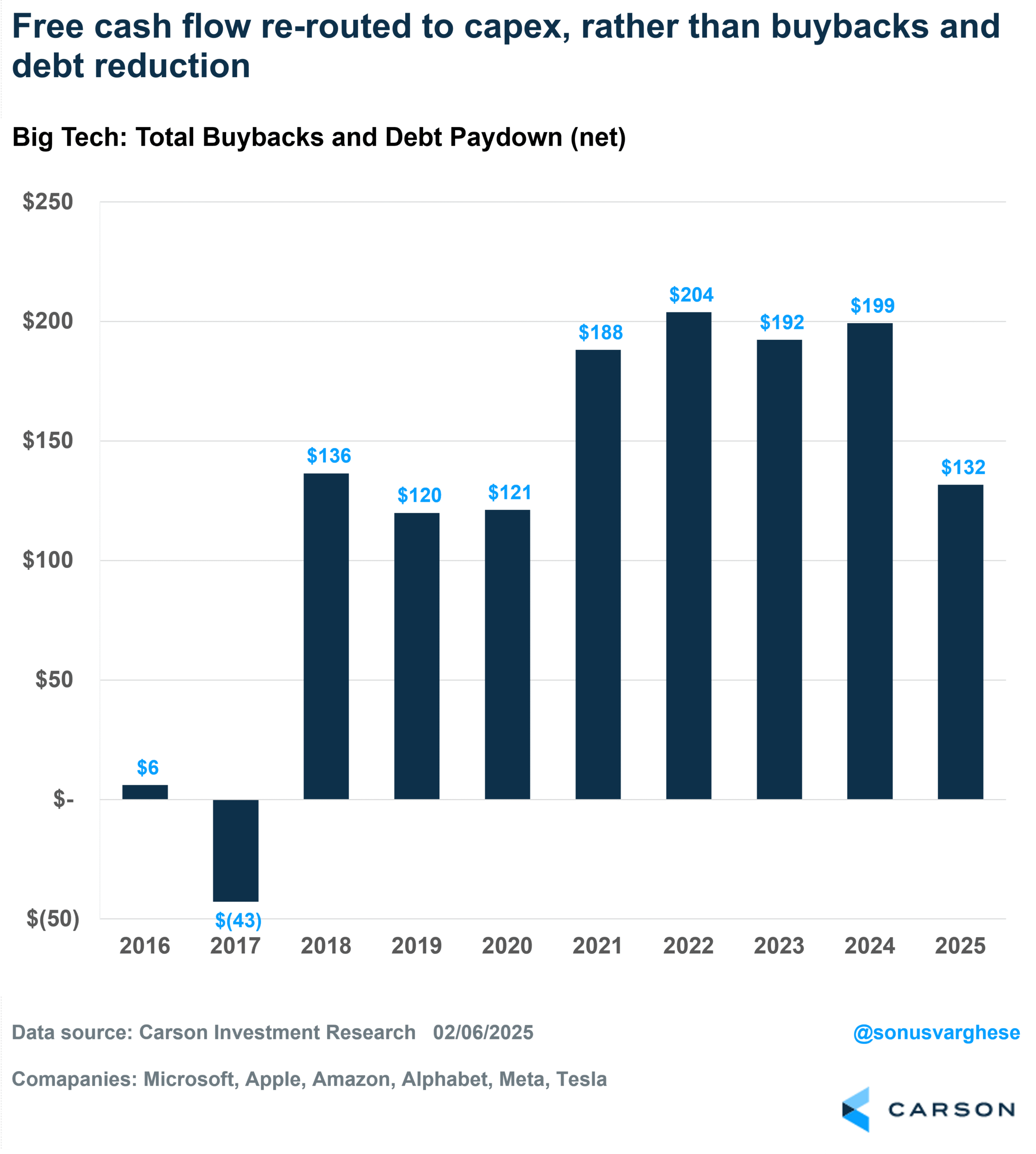

All this comes at the cost of returning money to shareholders, via share repurchases (buybacks) and paying down debt.

- Buybacks and net decrease in debt across the major tech firms averaged $196B from 2021-2024.

- That fell 33% to $132B in 2025.

- In our opinion, expect that number to plunge even more in 2026.

This does take out some support from the stock prices of these companies, as buybacks reduce supply and typically boost the stock price.

Free cash flow from other operations is not going to cut it by itself. Debt is becoming a larger part of the story as capex plans balloon. Alphabet, Amazon, Meta, and Oracle borrowed about $93B last year, accounting for 6% of corporate bond debt issuance.

Meta’s debt has jumped from $29B in 2024 to $59B in 2025. Alphabet’s debt load rose from $11B in 2024 to $47B in 2025, and they just announced another massive debt issue this week – they’re looking to raise $15B from bond sales, and are also selling a 100-year bond as part of this offering.

If you’re wondering if investors will in fact lend money for 100 years, there’s some precedent for such a long tenor. Last year, Alphabet sold a 50-year bond as part of a $17.5B debt offering, and that attracted $90B of orders, so there’s plenty of demand. Just last week Oracle raised $25B in a bond sale that attracted $125B of orders. The company doesn’t expect to sell more debt in 2026, but they are planning to raise another $25B of equity this year, a move meant to reassure investors that they won’t strain their balance sheet too much to fund their capex spending spree on datacenters. But equity sales also dilute the value of existing equity.

JP Morgan projects another $300B of AI and data center related deals EVERY YEAR FOR THE NEXT FIVE YEARS.

One Company’s Spending Is Another Company’s Revenue (and Profits)

This is what we wrote in the Outlook:

“Private sector investment is a source of corporate profit growth. Since profits are the main driver for stock prices, the key question is whether this level of investment spending will continue. The short answer seems to be yes, and it looks like early innings on that front.”

If anything, we underestimated the level of capex spending in 2026, which means it’s going to be an even bigger boost for aggregate profit growth this year. Don’t be surprised if earnings expectations continue to ratchet higher as we move forward.

While it may look like investors are skeptical of these enormous capex plans, as reflected in stock prices for these companies last week, it doesn’t look like the companies are going to take their foot off the gas pedal. As we discussed in the Outlook, they’re in a bind. Each one sees an existential need to “win” the AI race, and so they’re incentivized to ramp up investment. If one company starts down that path, others feel the need to join the race and go all-in, which is why Google cofounder Larry Page said, “I’m willing to go bankrupt rather than lose this race.”

In short, don’t expect to see any unilateral disarmament. The opposite looks to be the case – we’re in a capex arms race.

Bigger picture, we are in a capex cycle with some strong parallels to those in the past, including the railroad and internet boom. The dynamics are similar: The promise of new technology pushes firms to make massive investments. Historically, investors seem to like that, and stock prices soar, facilitating even more investment. But history tells us that ultimately, demand fails to keep up and there’s excess supply, although that ultimately benefited society, whether it was railroads, high-speed internet that allowed us to connect as never before, new housing to meet the demand of the next generation, or cheap oil. Overcapacity eventually leads to lower stock prices and lower valuations, and investment spending reverses. The dynamic is exacerbated when debt enters the picture, as the unwind becomes ugly.

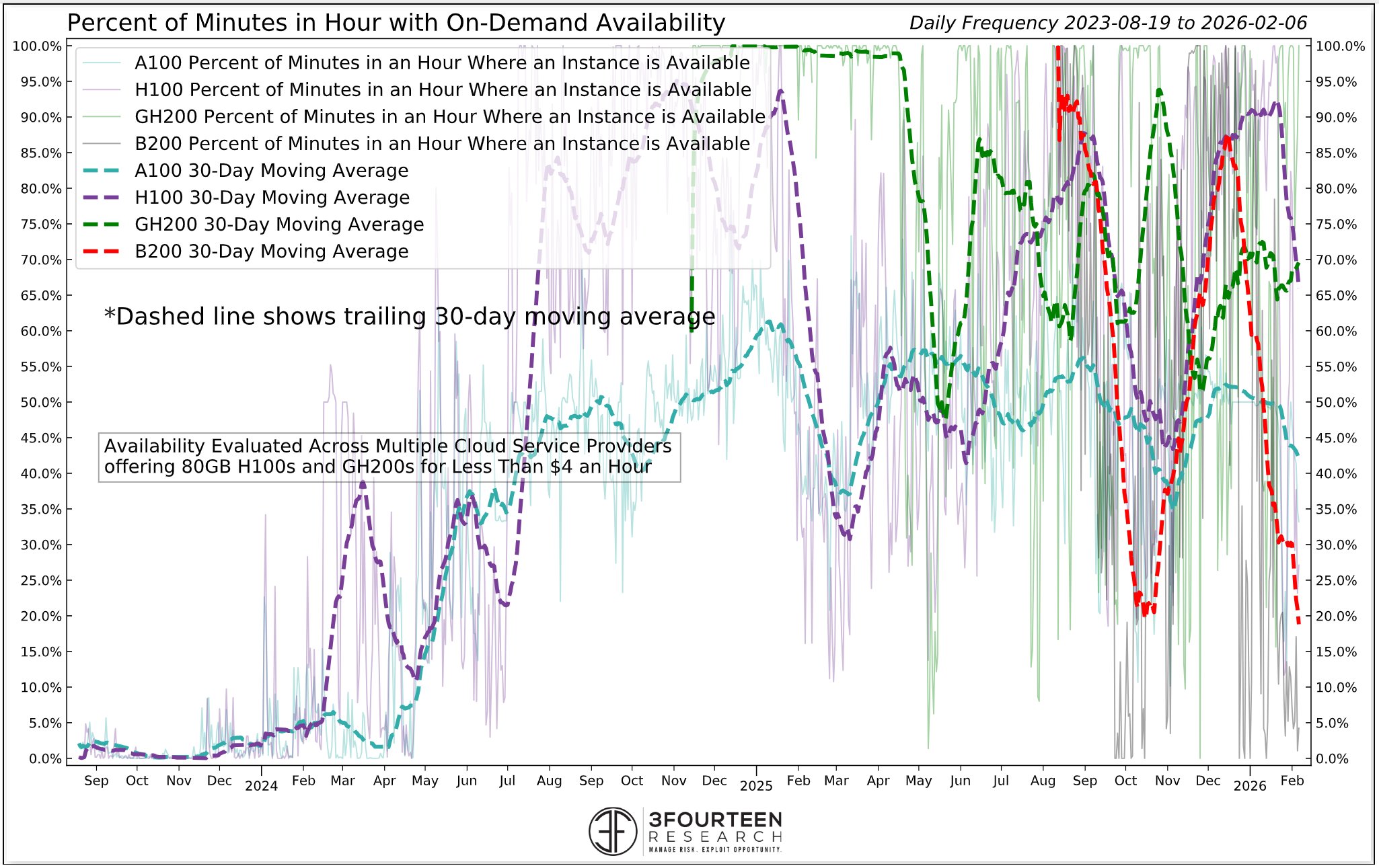

However, we believe the length of the cycle (only a few years old), technology acceleration, and relatively low current debt levels suggest we’re not in the latter part of the cycle. In fact, demand for AI continues to rise, and GPU availability is falling across the board. Here’s a chart from our friend Warren Pies (at 3Fourteen Research) showing availability of Nvidia’s Blackwell B200 chips making new lows.

We don’t think the negative part of the cycle is a 2026 story, or even necessarily 2027. For now, we believe we can ride the AI boom but don’t believe it’s time to chase the AI theme with concentrated positioning—better to tilt in that direction for participation within a broadly diversified portfolio that includes exposure to other areas of the market (like industrials), and even international stocks, all of which could be the ultimate beneficiaries of all this spending.

Ryan and I talked about the “Tech Wreck” in our latest Take 5 video:

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

8765709.1. – 10FEB26A