(Updated as of 3pm CST 4/9/2025) We had the largest tariffs in over 100 years on for about 12 hours, before President Trump paused them for 90 days for countries that did not retaliate. That’s a relief, though we could be right back here in 90 days. But hopefully this gives the White House time to negotiate with everyone and ease the temperature a bit.

Keep in mind that several additional tariffs have already been imposed, including 20% tariffs on Chinese imported goods. 25% tariffs on steel and aluminum, 25% on automobiles, 25% tariffs on non-USMCA compliant goods from Canada and Mexico (and a lot of goods are non-compliant, because costs of compliance were high), and 10% tariffs on all other imports.

These are already having an impact on importers in the US, who are the ones who have to pay the taxes (tariffs!), as opposed to the exporting firm.

Here’s a hypothetical example. A small business owner in the US ordered aluminum parts from China, worth $3,380, and they crossed the border on March 31st. The shipper, DHL, requires $2,483 for import duties (tariffs) to be paid, or they’ll send the shipment back to China. The tariffs amount to a whopping 73% of the cost of goods, and include the 25% tariffs on China from Trump’s first trade war, 25% steel/aluminum tariffs, and 20% tariffs imposed on Chinese goods in March. Needless to say, it’s not easy on a business owner when a $3,380 order comes with an extra $2,483 tax bill.

But it could be worse. Luckily for this small business owner, this shipment came before the additional 84% tariffs on China’s goods go into effect on April 9th. though that’s likely to be small solace since they likely will have to order more parts for the business to continue as before. Or maybe it won’t if they decide they cannot be profitable anymore.

As you can see, its businesses in America who pay the tariffs (not China) and they’re going to have to decide whether to eat the higher cost from their own profit margins, or to pass it on to their customers. And for some owners that will mean a decision about whether they can stay in business.

This is going to be a problem for businesses across America. But when I mentioned that we have a big problem in the title, this is not what I meant (which is not to minimize the tariff problem). There’s something hugely problematic happening in markets, and it’s not even the fact that equities have crashed over the last four days. Instead, it’s the US Treasury bond market, typically the most liquid and deepest market in the world, that is throwing a fit.

Meltdown in The Bond Market

Treasury Secretary Scott Bessent has argued that even if the tariffs create a short-term economic slowdown and volatility in the stock market (check), that wouldn’t be too concerning since only the top 50% of households by income own stocks (note that this isn’t quite true, with lower income households owning at anywhere from $2 – $3 trillion in stocks, which is not nothing). His main goal is to get long-term interest rates to fall, since that would help lower-income households who tend to have more debt service costs. (Note that an economic slowdown, or recession wouldn’t be great for this group either because that could mean they lose their jobs.)

There’s also been an argument that this whole exercise of imposing massive tariffs is to reduce interest costs for the federal government, which has to refinance $9 trillion of debt next year. In reality, the federal government always has a lot of debt to refinance because it issues a lot of short-term debt (which all of us happily purchase, including in money market accounts). However, the interest rate on that depends heavily on short-term policy rates determined by the Federal Reserve (Fed). And if you want the Fed to cut rates, policy that sends inflation the wrong way would not be the way to do it.

In any case, we may have a big problem on our hands. US Treasury interest rates are surging. The 10-year yield has surged to 4.45%, which is the highest level we’ve seen over the past month. On April 1st, the day before Liberation Day, the 10-year yield was at 4.17%. It fell as low as 3.92% as stocks plunged, before surging more than 0.5%-points over the last three days. That’s a massive move.

Is This China’s “Revenge”?

Yields rose sharply on Tuesday (April 8th) after a weak Treasury auction for $58 billion of short-term 3-year debt. There are rumors that this was China’s “revenge,” i.e. they’re selling US Treasuries in retaliation for tariffs. Let me be clear: this is just pure speculation without even a hint of evidence.

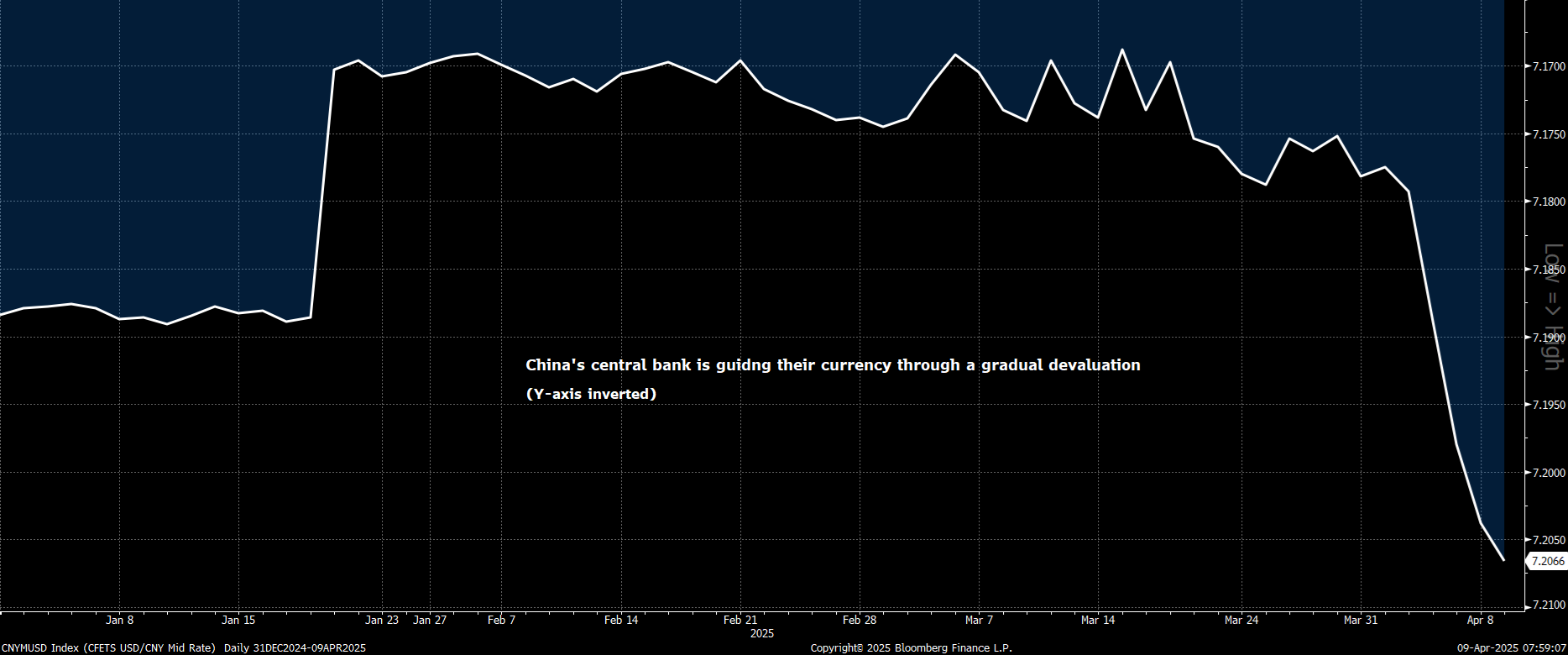

For one thing China does not own a lot of US Treasury debt anymore, just about $760 billion. If they were selling US debt, they would be selling USD and buying yuan, in which case we’d see major appreciation in the yuan. That’s not happening right now — in fact, the opposite. The PBOC (China’s central bank) set the yuan reference rate just above 7.2066, slightly weaker than the prior day’s level of 7.2038, and the fifth straight day of fixing the yuan lower. The yuan is now close to the lowest level in a decade and a half, with the PBOC carefully managing a gradual decline in their currency. Of course, this has the added effect of shielding the economy from tariffs, since it makes Chinese goods even cheaper (though they have a long way to go to overcome a 104% tariff).

A Dash for Cash

Instead, it’s likely due to portfolio managers at hedge funds liquidating positions. For one thing, cash is paying 4.3%, and so with the prospect of inflation (from tariffs), why would you want to take extra risk on long-term bonds? Inflation expectations over the next year, as measured by inflation swaps, have surged to almost 3.6%, which is the highest since mid-2022.

Several hedge fund strategies are also being unwound. There’s something called the “basis trade,” where funds use a ton of margin to take advantage of tiny difference in prices for Treasuries and associated futures. These are very small price differences and you need a huge amount of margin (about 50x) to make real money on it. Hedge funds were expecting Bessent to cut banking regulation this year, and one rule involved something called the “standard leverage ratio,” which makes it more expensive for banks to hold Treasury debt. These funds expected banks to start buying debt again and bet that Treasuries would outperform interest rate swaps (derivatives that are bets on yields). But because of tariffs, and rising inflation expectations, yields have risen, and banks are selling Treasuries instead. And so, interest rates swaps have outperformed Treasuries, forcing funds to delever (reduce margin) and unwind their positions. Oops.

The Fed’s Conundrum

A big part of what’s happening in bond land is the conundrum facing the Fed. Growth expectations are falling, best highlighted by crashing energy prices. WTI oil prices have plunged 20% over the last week to almost $56/barrel. At that price, we’re not going to get new drilling activity in the US, as oil producers need prices near $65/barrel to profitably dig new wells.

Lower growth expectations, or even a recession, should ordinarily lead one to expect the Fed to cut rates (and markets expect five cuts now in 2025). The problem is 1-year inflation expectations, as I noted above, have surged to 3.6%. That makes it very hard for the Fed to cut rates, even if inflation is “transitory.” In fact, Chicago Fed President, Austan Goolsbee, normally the most dovish member of the FOMC, just expressed concerns that inflation could be persistently high for a while — that’s not good.

The market coming to terms with the possibility that the Fed may not cut rates as much as they expect, or at all, could be the next shoe to drop. Of course, if there is a seizure in the Treasury market, like in March 2020 when Treasuries sold off rapidly as funds deleveraged, the Fed may step in to provide liquidity. But that’s different from cutting rates and supporting the economy overall with lower rates, unless their actions are taken as “forward guidance” for upcoming rate cuts. Color me skeptical on that. Now, if the unemployment surges, say to 4.6%, we could see a rate cut, but that would mean the economy is in real trouble. In any case, the Fed is not going to cut rates until they see poor data, which means they’re going to be behind the curve.

This is the problem when you have an inflation constraint — something that didn’t exist for most of the last 30 years. The big exception was in 2022, but the Fed was quite willing to throw the economy under a bus back then to get control of inflation, with Powell and co saying a recession is likely and projecting much higher unemployment rates.

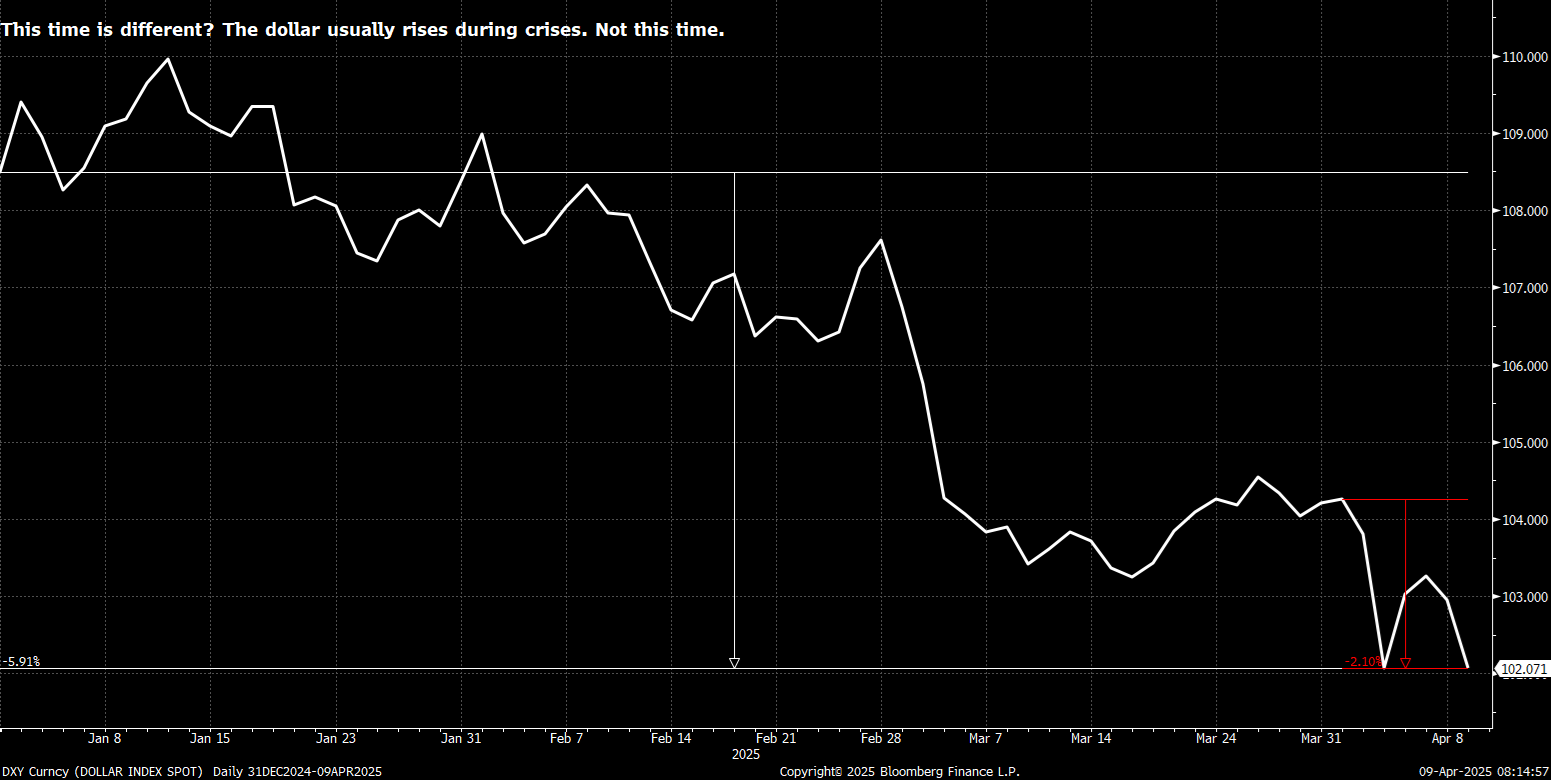

A Weaker Dollar Creates Another Problem

One way to mitigate some of the inflationary impact of tariffs was a stronger dollar, as the current White House Chair of the Council of Economic Advisors, Stephen Miran, has suggested. However, given the magnitude of the tariffs, this was always going to have a minimal effect.

The problem is that the dollar has been going in the opposite direction. It’s been easing this year, with the dollar index down 5.5% year to date. It’s also pulled back almost 2% since April 1, the day prior to Liberation Day. That’s not good, as it makes imports even more expensive.

When people ask me what’s the difference between an emerging market (EM) and developed market, I tell them that my market-oriented perspective is that a country is an EM if the following happens during a crisis:

- Stocks fall

- Sovereign government bond yields rise

- Currency falls

We now have this exact environment in the US. Even in March 2020, as equities crashed, and Treasury yields rose briefly (before the Fed stepped in), the dollar was appreciating. That’s not the case now.

The only way to explain these moves is that investors, and the rest of the world, has lost confidence in America and is no longer flocking to the traditionally perceived safety of the US dollar and Treasuries. These now have a significantly higher risk premium and may no longer be “exceptional.” This is not to say markets won’t recover — they could (but we’re going to need to see a reversal from the White House for that). But going forward the usual expected correlations between different parts of an investment portfolio — US stocks, international stocks, bonds, cash, and even commodities — may need to be adjusted quite significantly.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7839913.2-0425-A