A resounding, and sometimes frustrating, feature of markets is that leadership change is inevitable over any period of time studied. The “A.I. Trade” has been prevalent for the past couple of years, absent some blips here and there (DeepSeek, Liberation Day, etc). In some ways, the A.I. trade has started turning upon itself – previous darlings of software and other areas now facing sure extinction at the hands of Claude, Chat, Gemmy, and Grok (there are plenty of other A.I. models and interfaces, but that quartet seems movie-worthy). What has risen above this world of 1s and 0s are the real, physical assets that power, feed, and support the global economy.

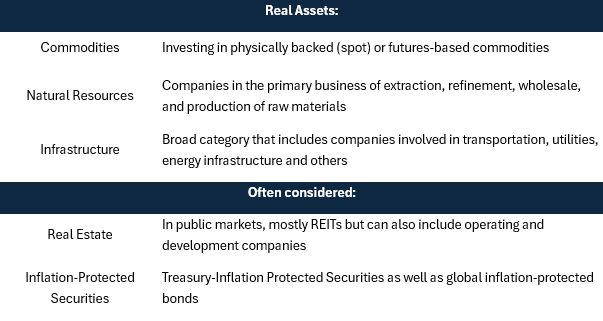

We defined real assets into 3 main categories, as shown below, but others are often considered as well. Raw materials, companies that process them, and the delivery mechanisms for those materials are generally considered real assets. Real Estate also naturally falls into this category, both by name and by its ability to pass through inflationary pressures (we’ll get to that shortly). However, most public real estate investment is through the Real Estate Investment Trust (REIT) structure, which has its own complexities and may dilute some of the inflationary protection we are after. We’d encourage you to consider private options, but that is beyond the scope of this discussion. Finally, as a volatility dampener for these generally cyclical asset classes, fixed-income securities with inflation protection components may also be included in the real asset category. We’d argue that these are beneficial against inflation relative to traditional fixed income (by design), but not much else.

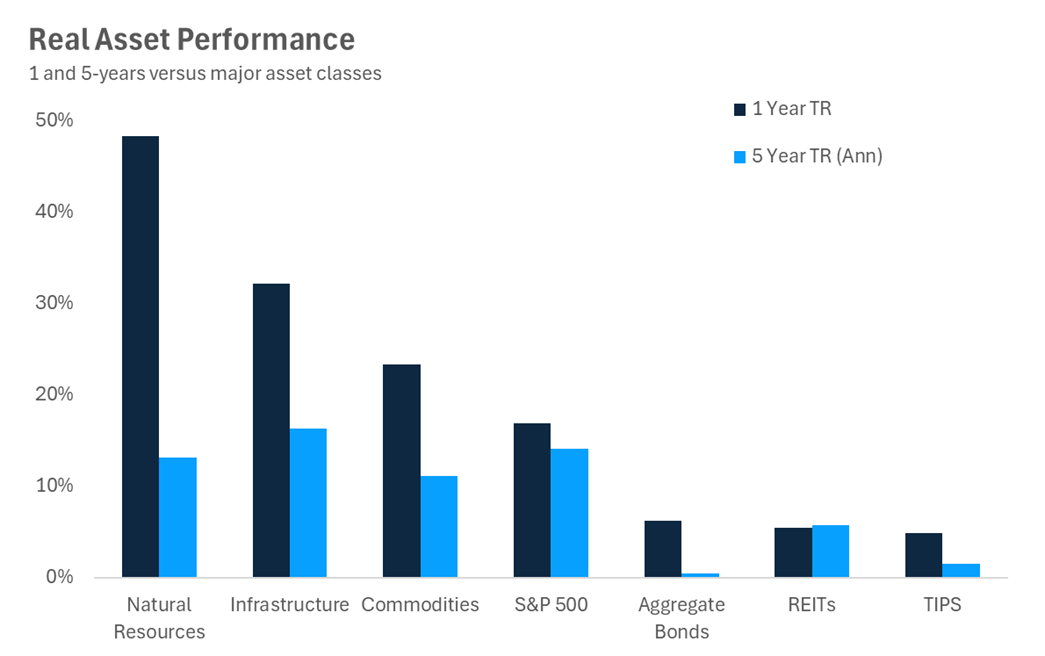

The interest in real assets lately really started back in 2020. If you remember, many of us would like to forget – oil futures actually went negative in April of that year for a brief period. Since that day, energy infrastructure companies (think MLPs, etc) thrown out with the bathwater of negative oil prices have actually doubled the return of the S&P 500! Strength in commodities and natural resources emerged in 2022 as inflation rose precipitously, and in more recent years, it has been gold that has led nearly every asset class. Now in 2026, we are seeing other commodities pick up steam, and most recently, oil prices have jumped globally on the conflict in Iran.

Sources: Carson Investment Research, Morningstar 2/28/2025

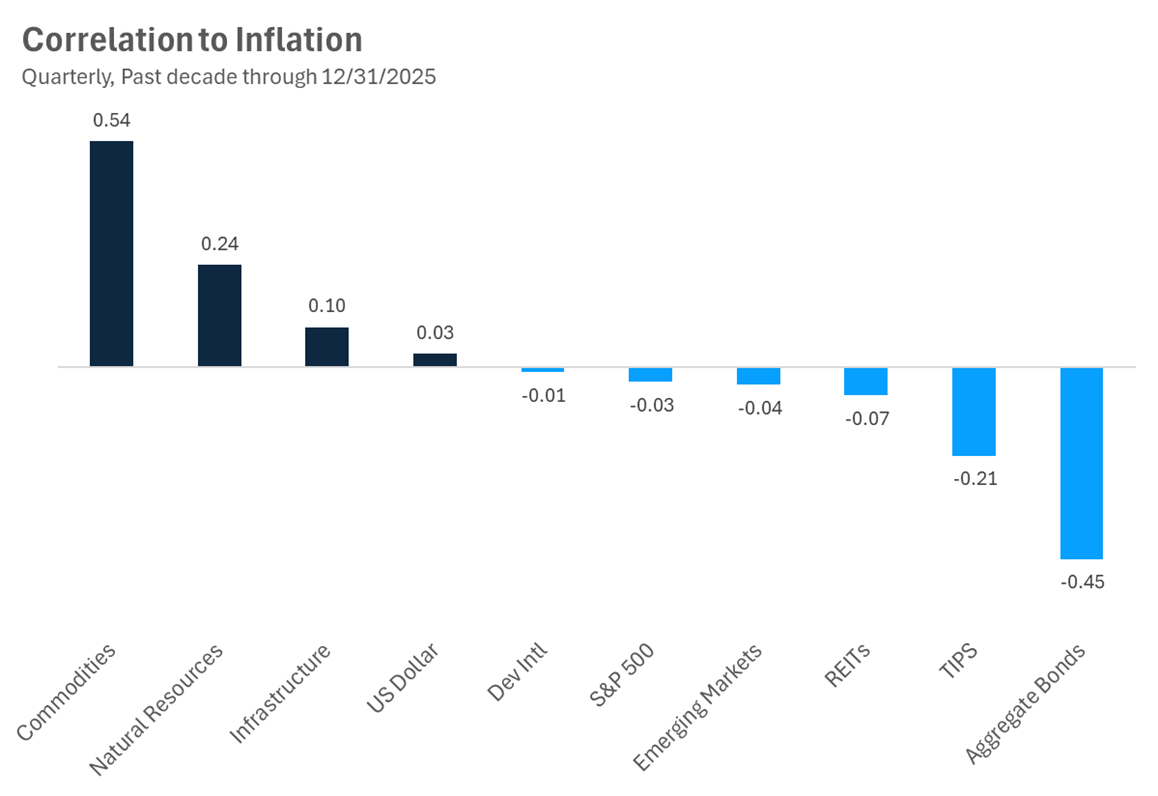

Typically, real assets are less correlated with traditional stocks and bonds because commodity prices and other factors affect their returns. This tends to make them a good complement to portfolios, especially when volatility is controlled for. In addition, a major benefit of including real assets in a portfolio, or at least as part of a client’s overall asset allocation, is their inflation protection. Over the long-run, stocks do a great job of maintaining purchasing power versus inflation, but in short and especially unexpected inflationary episodes, real assets shine.

The chart below illustrates this point. Over the past 10 years, commodities, natural resource companies, and infrastructure have been positively correlated to changes in inflation. On the flip side, fixed income suffers when rates rise – and interest rates are generally tied at the hip to inflation and inflationary expectations. Even TIPS, specifically designed to protect principal from inflation, don’t usually help all that much when inflation is around, but they do behave better compared to traditional fixed income.

Sources: Carson Investment Research, Morningstar 12/31/2025. Correlation measured quarterly to US CPI All Urban SA

The tremendous performance we have seen in many areas of real assets – precious metals in particular – may give investors pause. To alleviate that concern, considering a diversified real asset strategy or expanding your opportunity set beyond just gold may be appropriate. Especially if inflation sticks around longer than expected. We are just two months into 2026, and things just got real – position portfolios appropriately.

For more content by Grant Engelbart, VP, Investment Strategist click here.

8807146.1. – 5MAR26A