If you haven’t read it already, in yesterday’s insightful blog, Carson’s Chief Macro Strategist Sonu Varghese provided an update on inflation expectations given the expanding (for now) conflict in the Middle East. For the basic takeaway, just look at the title: The Inflation Outlook Doesn’t Look Good. Now that’s not 2022 “doesn’t look good.” But progress towards the Fed’s target was already in question, despite an economy showing weak hiring trends and solid, but not booming, growth. Still, there are some similarities to 2022: we were already facing inflation (though not nearly as severe as in 2022), and then a war came along (Russia’s invasion of Ukraine on February 4, 2022) that added new inflationary pressure.

But there are some key differences with 2022. The underlying inflation challenges pre-conflict were worse in 2022 as we continued to work through pandemic supply chain disruptions and excess fiscal stimulus. Also, the Russian/Ukraine conflict is still ongoing, although we didn’t know it would last this long at the time, having recently passed its four-year anniversary. For this conflict, we’re more likely talking weeks rather than years, and energy prices should revert when the conflict ends, although any damage to energy infrastructure or key transportation corridors could slow the process.

But like 2022 inflation, right now is not just about the conflict in the Middle East, as Sonu laid out in his blog. AI demand for energy and chips, fading but still present pro-inflation policy effects (tariffs, immigration, fiscal stimulus), and steadily rising commodity prices pre-conflict were already creating a more challenging inflationary environment that was showing up in pre-conflict numbers. As in 2022, there was already an inflation problem, and that can make new inflationary pressures a multiplier rather than merely additive.

This has shifted rate-hike expectations in a short time, though remember that expectations tend to be noisy. According to CME analysis, since Friday, the fed fund futures-implied end-of-year fed funds rate has climbed about 0.15%-points, or about 0.6 quarter-point rate hikes. That doesn’t have a meaningful impact for now on our outlook for the 10-year Treasury yield, since the market is coming back to us, and our view has been that sensitivity to rate cuts has declined, given our base-case view of an inflationary expansion and persistently elevated inflation uncertainty (which is not the same as elevated inflation). You can view the effects of the conflict in the Middle East as consistent with that belief, with added risk if the conflict expands or becomes extended.

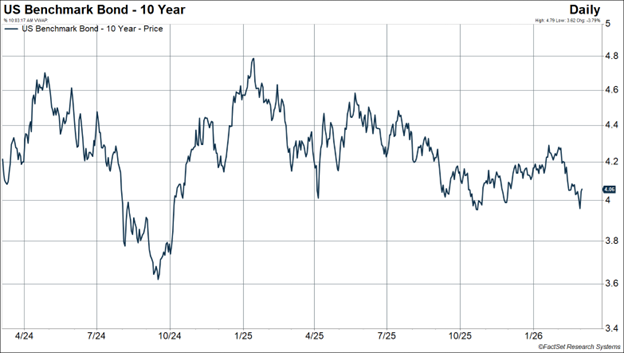

The 10-year Treasury yield finished 2025 at 4.17% and has held a roughly 4-4.25% range since early September, reaching the top of that range in January but declining sharply in February, partly as a risk-off move amid the US force buildup in the Gulf region. While there’s some folly in point estimates, our view is that the 10-year yield ends 2026 closer to the top of that range, especially given what’s happening right now with inflation. If that turns out to be true, a 10-year Treasury would have a total return of about 1.5% over the rest of the year, with a price decline of about 2% cushioned by coupon payments in the mid-3% range. That’s less than you would expect from Treasury bills, but because intermediate Treasuries are a hedge against downside risk in some scenarios, it’s still worth giving them a meaningful weight.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

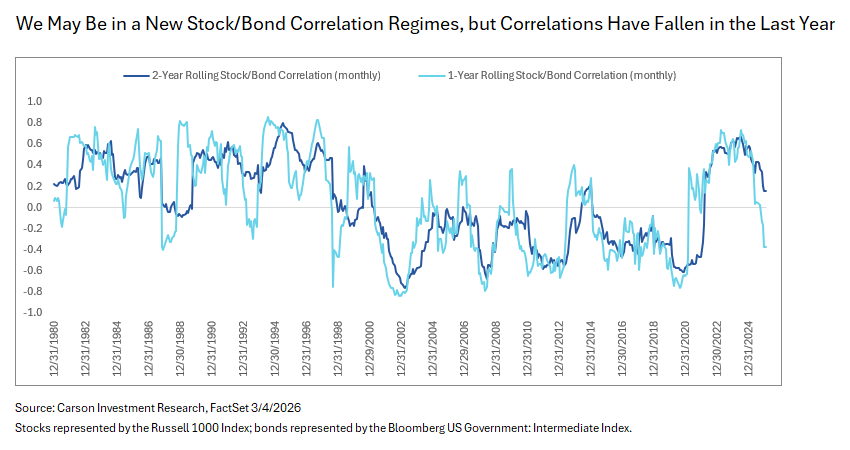

Treasuries have been an effective portfolio diversifier over the last year, including during the post-Liberation Day near-bear market, but looking back two years, it still seems likely that we have shifted to a higher-correlation regime between bonds and stocks. Generally, in tactical allocations, we recommend a roughly 2-1 ratio of intermediate to short-maturity bonds, with an emphasis on Treasuries, preferring to focus equity-correlated risk in stocks rather than credit-sensitive bonds. In strategic allocations, we are underweight bonds but are willing to keep rate sensitivity higher, since, over a strategic time frame, yields are the main driver of returns, and intermediate and longer-maturity yields have become increasingly attractive relative to short-maturity yields as the Fed has cut rates. But because of the below-benchmark bond weight, our expected portfolio risk from bonds in strategic allocations is roughly at benchmark levels.

But both tactically and strategically, we have actively sought ways to enhance diversification other than simply allocating to bonds. That has included an allocation to gold (which we first added in 2023), use of managed futures (a trend-following strategy with a historically low correlation to both stocks and bonds that can have long or short exposure to a range of commodities, currencies, bond indexes, and sometimes stock indexes), real assets, and even low volatility stocks. We still believe bonds play an important role in a portfolio, but the shift away from steady rate declines of 1981-2020 requires a more thoughtful approach.

For more content by Barry Gilbert, VP, Asset Allocation Strategist click here.

8805121.1. – 4MAR26A