Nvidia investors have envy for the first time in a while. Although Nvidia stock is up +20% year to date, it’s significantly lagging other semiconductor heavyweights. Nvidia’s poor relative performance comes as a new shift in computing towards Agentic AI takes place. However, Nvidia’s results and commentary from their earnings report may remind investors that the company is still a giant in the industry.

Relative Underperformance

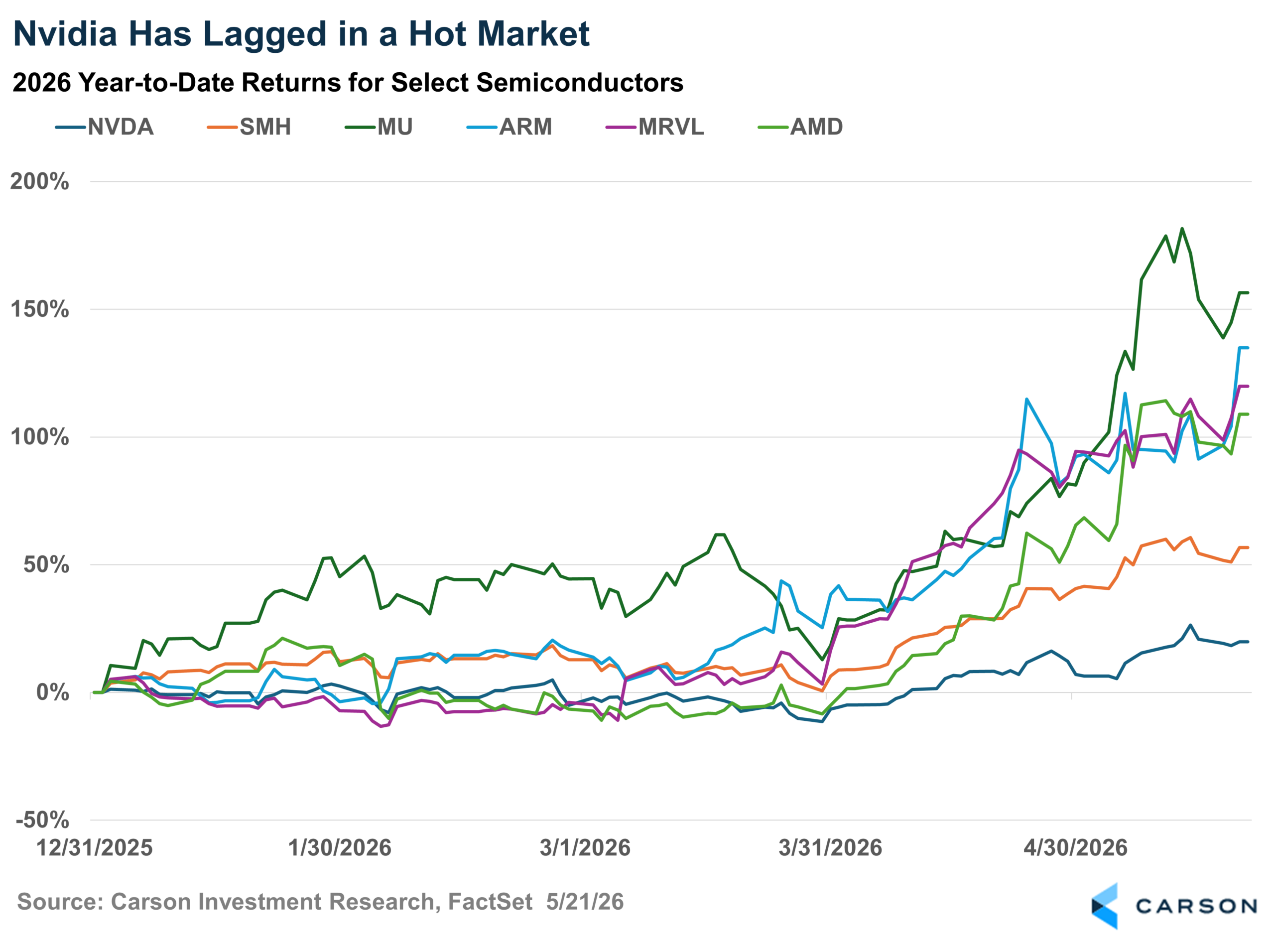

Nvidia stock is underperforming it’s peers so far in 2026. The stock’s +20% year to date return is nothing to scoff at, but it pales in comparison to the VanEck Semiconductor ETF’s return of +57%. As shown below, some of Nvidia’s competitors – such as Micron, ARM, AMD, and Marvell – have seen booming stock price gains this year. Many of these stocks have run up in anticipation of Agentic AI benefiting their position in the market more than Nvidia may stand to benefit.

Record Results

Nvidia’s record results in their latest earnings report handily beat estimates. The company reported $81.6 billion in revenue against expectations of $78.9 billion. This represents a staggering 85% year on year growth in revenue. What’s more, guidance for next quarter’s revenue to be approximately $91 billion would equate to a 95% revenue growth rate!

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

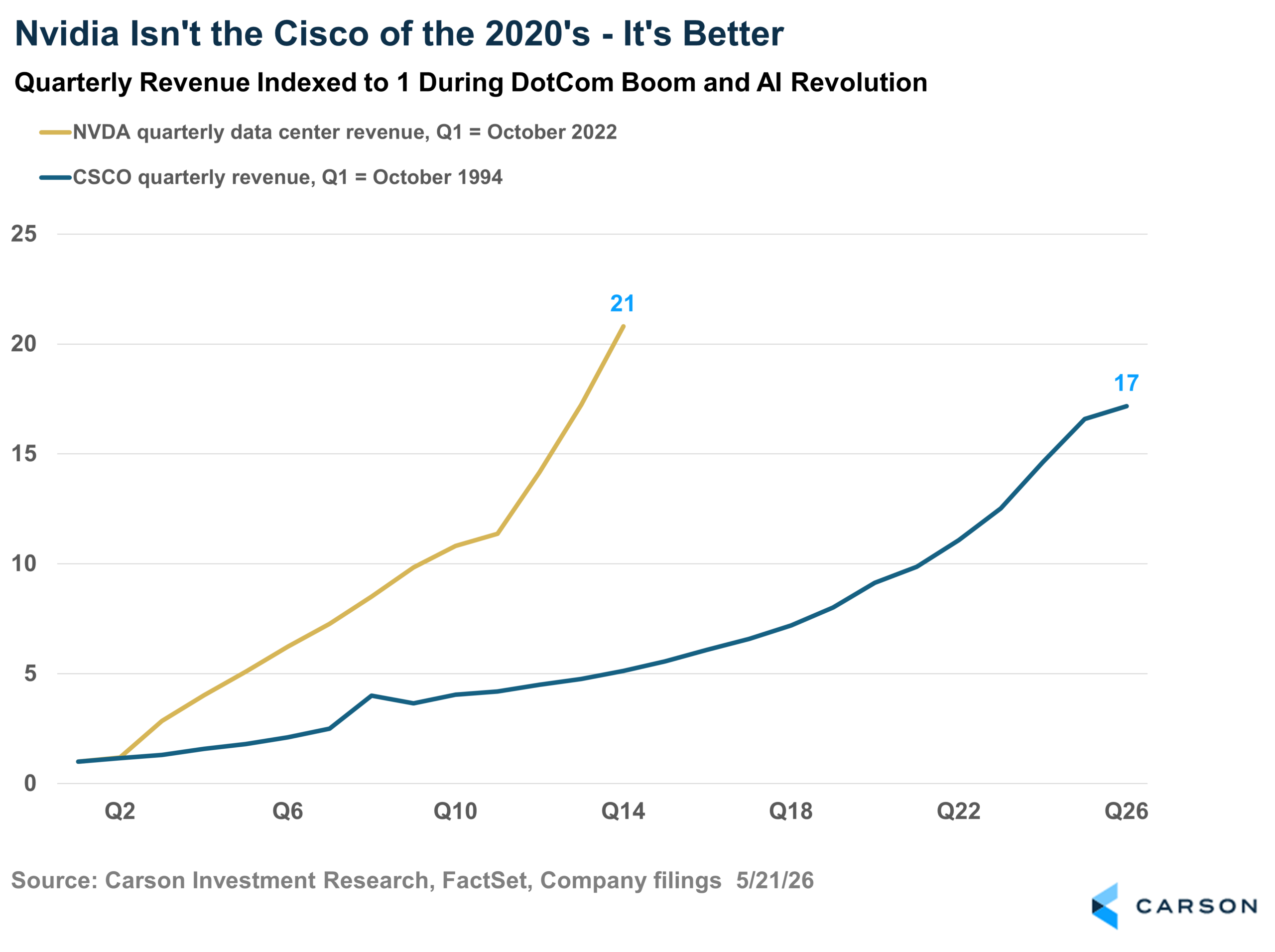

This quarter’s revenue results cement Nvidia’s run in the history books and may dispel any DotCom-type bubble worries. While there were fears that ‘Nvidia is the Cisco of the 2020’s’ – implying that the company’s stock price was disconnected from its fundamentals – this quarter’s results show Nvidia has delivered. From 1994 to 2000 (or 26 quarters), Cisco’s quarterly revenue grew a staggering 17x as the DotCom boom surged, as shown below. Nvidia’s revenue, in just 14 quarters since the start of the AI Revolution, has already grown 20x! Nvidia’s faster growth to a larger revenue level should help dispel worries and show investors that the company is generating staggering results.

The Growth in Agentic

A key reason Nvidia may be lagging behind some of its semiconductor peers so far in 2026 is the growth in Agentic AI. A key detail I highlighted from Intel’s report is that Agentic AI may drastically shift computing demand from GPUs towards CPUs. Nvidia CEO Jensen Huang used the company’s earnings call to detail why Nvidia remains well positioned even as this market grows. Huang noted that “the world has 1 billion human users [of AI]. My sense is that the world is going to have billions of agents…All of the thinking happens on GPUs. All of the orchestration essentially runs on CPUs. What we’re doing is we’re building infrastructure for AI…it needs incredibly great GPUs…and it needs great CPUs. We’ve got it all covered.”1 For investors worried about Nvidia’s growth from here, these comments may help reassure investors that the company remains flexible. Huang also emphasized that inference demand is accelerating much faster than previously expected, with next-generation AI models requiring dramatically more compute per query than chatbot-style systems.

Taken as a whole, Nvidia’s earnings report served as a reminder that the company remains at the center of the AI infrastructure buildout. While investors have rotated into semiconductor companies perceived to benefit more directly from CPU-driven orchestration workloads, Nvidia’s financials continue to exceed expectations. And much of current industry commentary suggests that the rise of AI agents may not reduce GPU demand, but instead brings the potential to massively expand the total amount of compute required across the ecosystem. Nvidia is working to position themselves not just as a GPU leader, but as a full-stack AI infrastructure provider.

For more content by Blake Anderson, CFA®, Director, Portfolio Management, click here.

8940816.1. – 21MAY26A