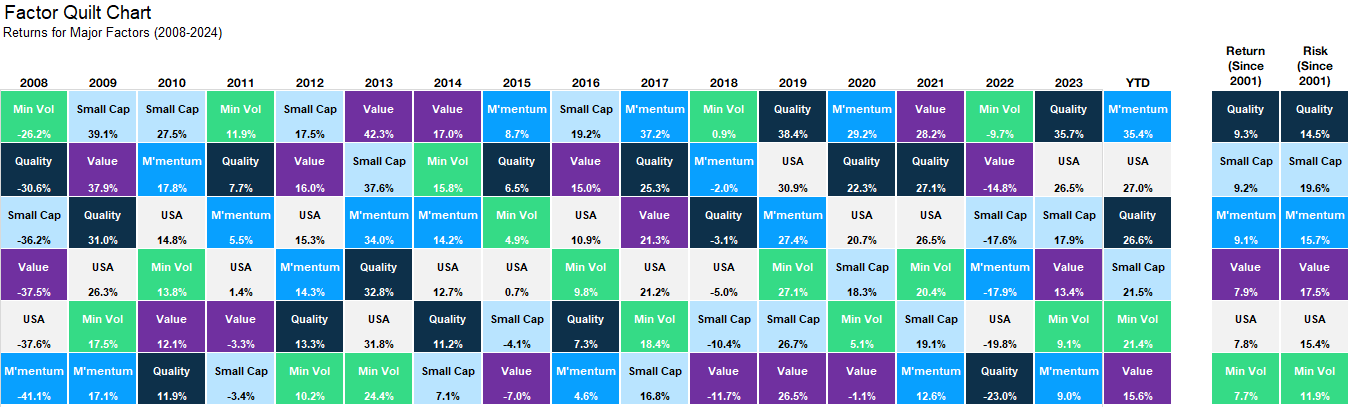

Factors

The world of investment product has evolved in many ways over the years, and that evolution has seemingly accelerated more recently. There are nearly 4,000 U.S. exchange-traded products, each with their own index or objective (for better or worse), this is on top of tens of thousands of traditional mutual funds. It can be overwhelming, to say the least, to figure out the best way to manage portfolios. I will offer a couple of concepts we have gravitated to in recent years.

The first is the inclusion of factor investing in portfolios. Factors are realistically descriptors of individual stocks (or sometimes bonds) that describe their risk and return characteristics. Quality, value, momentum, volatility, size, and sometimes yield are commonly known factors. When utilized appropriately, these factors can enhance returns and often at the same time lower risk in portfolios.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Investment factors have a degree of cyclicality, just like individual stocks, sectors, and even countries. Factors can fall in or out of favor, become over or undervalued, gain or lose momentum, or simply not represent the stocks that are best suited for the current economic or corporate environment.

Sources: Carson Investment Research, Morningstar, MSCI 10.31.2024

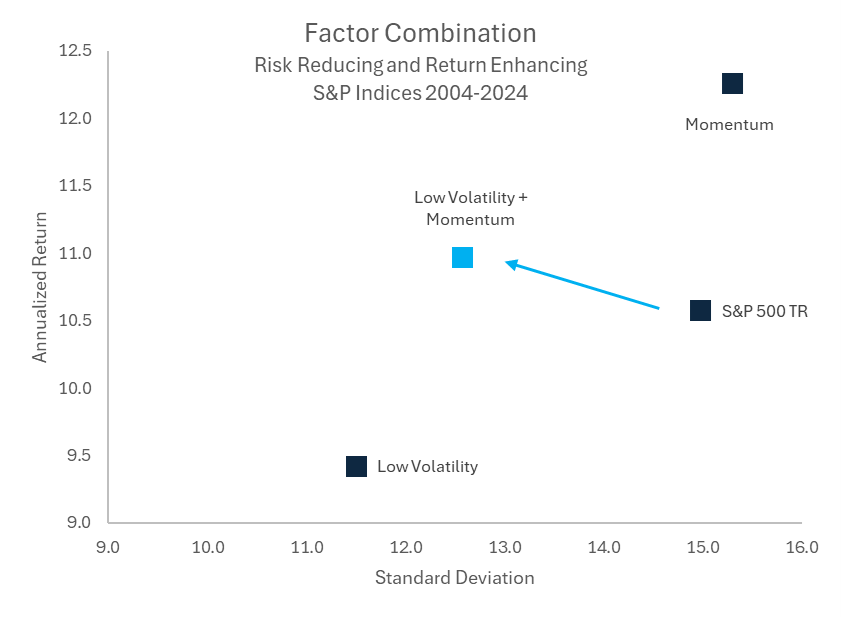

Carefully timing factor allocations requires a discipline process and consistent analysis of variables that affect factor returns. However, factors should exhibit a degree of structural benefit through time that can be beneficial to portfolios. Take for example the combination of low volatility – simply, the lowest volatility stocks in a given index over a given period of time, and momentum – the best performing stocks in a given index over a given period of time. Both are typically subject to additional constraints, but the basic premise remains. Playing offense via momentum, and defense via low volatility. This combination yields strong results particularly through market cycles, as the risk reduction of low volatility becomes clear, and matches up well with the return enhancement of momentum. The chart below shows a simple 50/50 combination of the two factors, with rebalancing parameters, yields a lower risk and higher return profile than the S&P 500.

Sources: Carson Investment Research, Morningstar, S&P

Active Management

In many ways, factor investing was designed to replicate active management, typically at a lower cost and in a way not prone to human error or judgement. In fact, a lot of actively managed equity portfolios can be replicated with low cost factors. That being said, well-vetted active managers have their place in portfolios as well, especially if they provide alpha over well recognized factors. The growth in active ETFs has contributed to this in very positive way, as ETFs almost always have lower expense ratios and tax consequences relative to their mutual fund cousins.

Active management has especially shined in fixed income. For starters, fixed income indices are a lower bogey than market-cap-weighted equity indices in some ways. There would be almost no way to own all 13,731 bonds in the Bloomberg US Aggregate bond index, as bonds do not trade on exchanges or in readily available inventory. Similar to stocks, but often times much more obvious, not all of these bonds are worth owning even if you could. While it takes substantial tracking risk to not own the largest stocks, not owning the largest bonds may very well be a good idea.

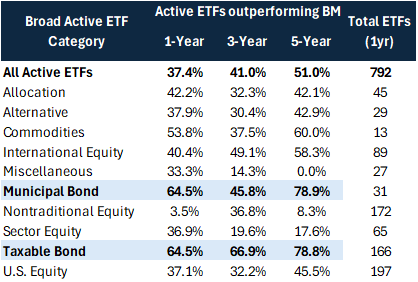

Additionally, many very strong active fixed income managers have come to market in the exchange-traded fund (ETF) wrapper. Active equity managers are following suit, but at a much lower pace due to worries about holdings transparency, front-running, and structural concerns that do not apply in the same way to fixed income. We think these concerns will continue to fade and more top-tier active equity managers will come to the ETF wrapper, but in the meantime active fixed income managers have proven in aggregate to be able to navigate the rocky recent world of bonds quite well. The chart below shows how nearly 2/3rds of all active managers in ETFs across municipal and taxable bonds have outperformed their respective benchmarks.

Sources: Carson Investment Research, Morningstar 10/31/2024

While not an investment philosophy etched in stone, we believe the combination of equity factor exposure and actively managed fixed income positions – all with a careful attention to asset allocation and risk – puts investors in the best place to succeed in today’s markets. The investment business is a lot about figuring out what’s not priced in. Over the last two years, our view was that the economy will avoid a recession, and the bull market will continue – which was beneficial from the perspective of generating excess returns from asset allocation. However, bullishness is more pervasive now and we could see more volatility in 2025. While we remain overweight equities, we are looking to potentially add excess returns by investing in factors like low volatility and momentum within equities, and actively managed strategies on the fixed income side.

For more content by Grant Engelbart, VP, Investment Strategist click here.

02536467-1224-A