“Here I go again on my own. Going down the only road I’ve ever known.”

-Here I Go Again by Whitesnake

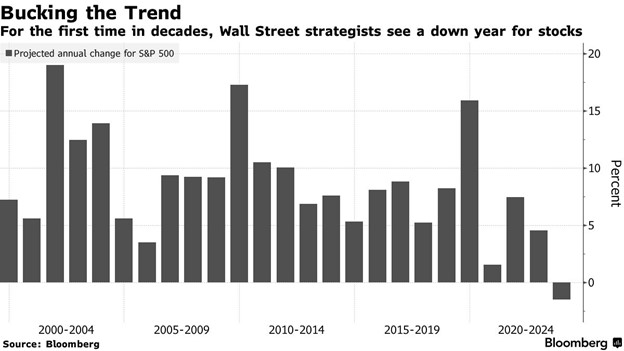

One of the main reasons we came into 2023 overweight equities (when everyone else was talking recessions and bear markets) was the over-the-top negativity. Rarely is the crowd and obvious trade right when it comes to investing and we assumed should we get any good news, stocks could surprise to the upside. One of the most staggering signs of negativity was the median strategist in this Bloomberg survey was looking for negative stock returns in ’23.

As we noted in Is Anyone Bullish? (from December 11, 2022), we’d never seen strategists this bearish heading into a new year. Then layer on the fact that stocks were down close to 20% in 2022 and the odds greatly favored a big bounce back year, as stocks were rarely down two years a in a row. Not to mention, the macro backdrop was on much better footing than the M2 is crashing, LEI is down, and yield curve fearmongers were telling us.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

All that happened was that the first six months of this year was the second best start to a year since 2000 for the S&P 500, best start for the NASDAQ in 40 years and the best start ever for the NASDAQ-100.

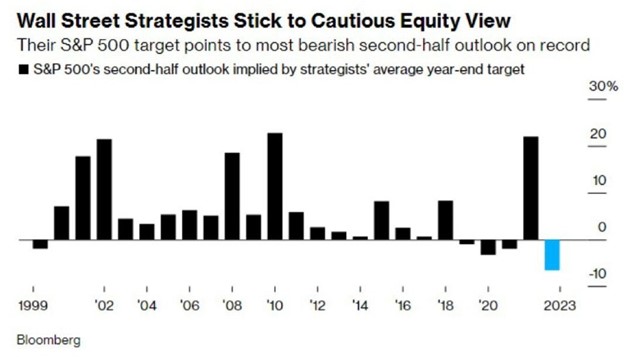

Where are we now? Well, similar to the great Whitesnake song in the quote above, here I go again, down the only road I’ve ever known.

Apparently, the only road these strategists know is doubling down on lower prices, as they expect the most bearish second half EVER. We’ll gladly take the other side to this, as we expect stocks to gain nicely the rest of this year, likely to new all-time highs.

Take note the other years they expected lower prices during the final six months of the year were 1999, 2019, 2020, and 2021. All the S&P 500 did those years was gain 7.0%, 9.8%, 21.2%, and 10.9%, respectively, over the final six months. That comes out to a very impressive 12.2% average, not bad, not bad.

What also has my attention? We have some big inflation data out this week, but we’ve already seen some nice signs that inflation could surprise to the downside. First up, used cars accounted for nearly a third of the jump in inflation the past few years, but it is crashing lower, with used car prices experiencing their largest monthly drop since COVID. Given light auto production is running close to pre-COVID levels, this is another sign supply chains are working again and price pressures are abating.

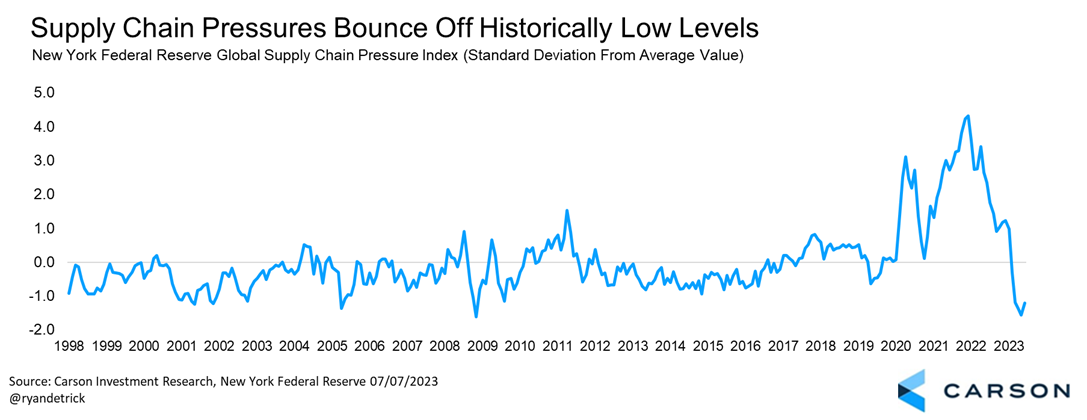

Speaking of supply chains, the New York Fed Global Supply Chain Pressure Index did jump last month, but it was coming off of the lowest level in history. Bottom line, supply chains are back to normal after years of disruptions.

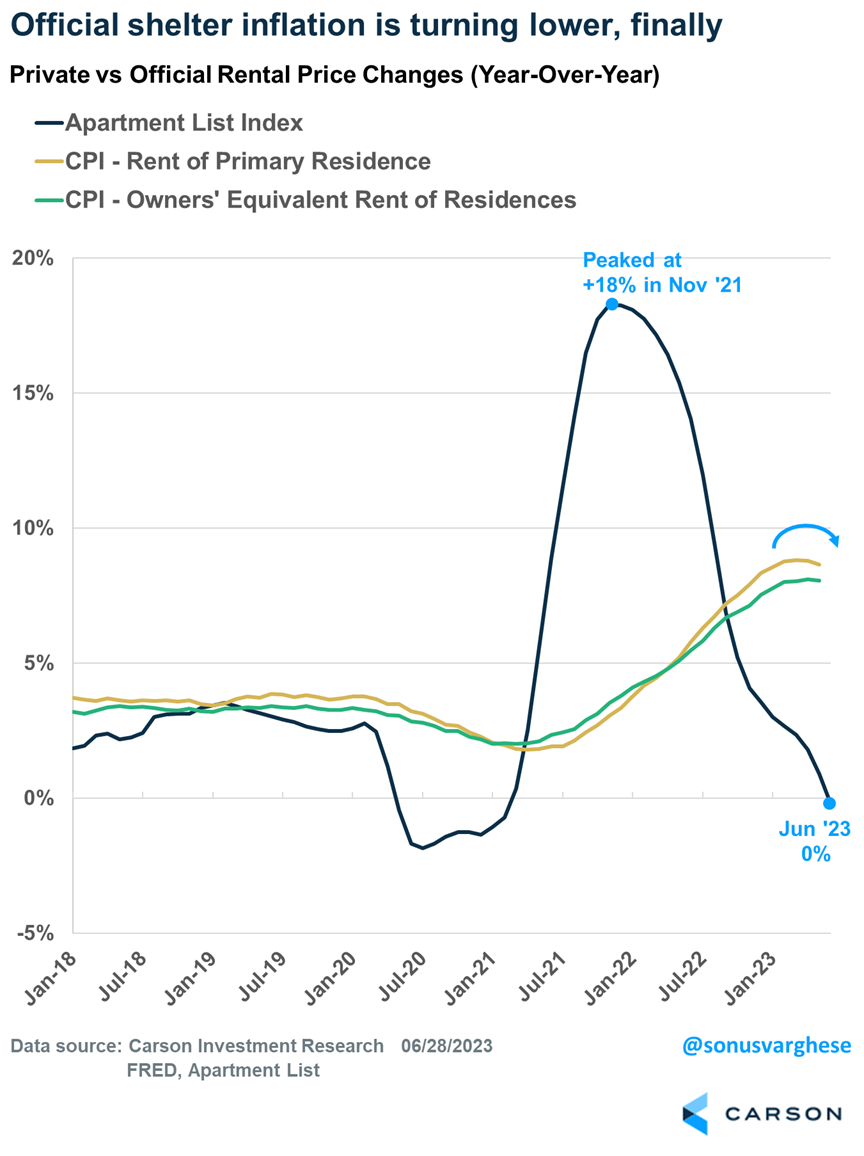

Along with supply chains and used car prices improving, we expect to see shelter take a big dive the second half of this year. Remember, shelter makes up more than 40% of CPI and it has stayed stubbornly high lately. Well, we’ve seen drastic improvements from private data places like Apartment List and Zillow, suggesting that the government’s data will likely follow suit soon.

Lastly, we’ve been hearing a lot that the trillions of dollars in excess savings that consumers had over COVID was nearly all the way gone. The media are spinning this as a bearish event, as it means consumers aren’t saving anymore and they will run out of money to spend and keep the economy growing. Here’s the issue with that, the savings rate has been trending higher the past year and is more than two percent higher than it was in early 2022. The employment backdrop is still healthy, spending is solid and consumer confidence is improving. To us, all of that is positive.

1829415-0723-A