Tech investors last week digested earnings reports that largely confirmed prior beliefs: semiconductors remain vibrant, while software remains challenged. Intel’s report highlighted the fundamental strength investors expected as AI agents grow. In contrast, ServiceNow’s report failed to meet expectations despite some optimistic commentary.

Intel’s Agentic Outlook

Shares of Intel traded to a new all-time high on Friday, finally surpassing their August 2000 peak of $75.81. The breakout follows Intel’s earnings report, which suggests a brighter future for the company as AI shifts from GPU-heavy training to CPU-focused agents. While Nvidia’s GPUs have stolen the semiconductor show in recent years, CPUs may be the chip of choice for AI Agents. Intel CEO Lip-Bu Tan explained on the company’s earnings call that “CPU is very important when moving from training to inference…I think the ratio of CPU to GPU used to be one to eight, and now it’s one to four, and I think [going] towards parity or better.”1

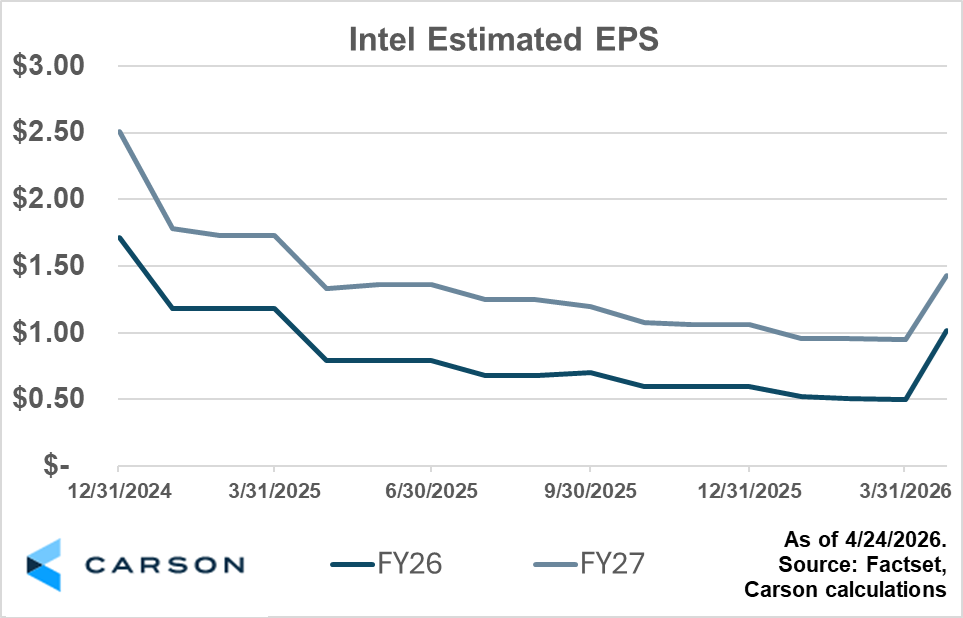

This potential shift in demand has catalyzed both Intel’s share price and earnings expectations. Analysts now expect the company to earn $1.02 per share in 2026, up from prior expectations of $0.50 before this report (FactSet consensus as of 4/24/2026, shown below). Intel’s 2027 EPS forecast was also considerably lifted following the report.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

ServiceNow’s Slump

Shares of ServiceNow slumped nearly 18% the day after its earnings report failed to meet investors’ expectations. While Intel appears to be benefiting from agentic AI growth, ServiceNow’s business model is simultaneously supported by – and pressured by – the same trend.

On the surface, ServiceNow raised its estimated full-year SaaS revenue expectations from $15.550 billion to $15.755 billion, a $255 million increase. That revision alone could have challenged the prevailing ‘software is weakening’ narrative. But investors may be concerned with how AI’s growth is changing the composition of revenue below this headline number. CEO Bill McDermott detailed on the company’s earnings call that “we had a goal to be $1 billion on our AI [revenue] this year…we’re already talking about $1.5 billion…it’s on a run.”2

This comment may have set investors on edge. If total company revenues were revised up by $255 million, and AI-related revenue was revised up by $500 million, does that imply that non-AI revenue potentially was revised down by $245 million? While the trajectory of AI-related revenues at ServiceNow is encouraging, continued cannibalization of legacy revenue streams could keep investors cautious in the near term.

Last week’s earnings reinforced a growing divide within tech: some semiconductors are benefiting directly from AI’s evolution, while software may face a more complex transition. Intel’s results suggest that agentic AI could materially shift compute demand toward CPUs, creating a meaningful tailwind for its business. Meanwhile, ServiceNow highlights a key tension in software – AI may drive growth, but not necessarily incremental growth if it displaces existing revenue. For investors, the critical question is no longer who has AI exposure, but whether that exposure may be additive or disruptive to the core business.

- https://finance.yahoo.com/quote/INTC/earnings/INTC-Q1-2026-earnings_call-544934.html

- https://finance.yahoo.com/quote/NOW/earnings/NOW-Q1-2026-earnings_call-547931.html

For more content by Blake Anderson, CFA®, Director, Portfolio Management, click here.

8895389.1. – 27APR26A