By Blake Anderson, CFA®, Associate Portfolio Manager

2026’s ‘Tech Wreck’ continues as investors extend their selloff in technology-related stocks. Investors have shied away from this industry as concerns about AI-fueled disruption to their core business models have risen. For investors with exposure to software, it may be informative to assess whether current prices signal valuation compression or a potentially durable deterioration in fundamentals. The data is clear – this drawdown is long and deep enough for investors to prepare for negative earnings revisions.

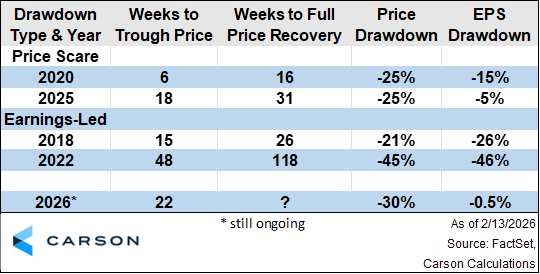

Over the past eight years, the software industry (proxied by IGV) has entered ‘bear market’ territory – defined as a decline of 20% from recent high prices – five distinct times: late 2018, early 2020, 2022, early 2025, and now in early 2026. To say it’s been a bumpy ride for software investors might be an understatement.

However, not all of these drawdowns are created equally. In two cases, the decline was largely a ‘price scare’ – where valuation compressed more than earnings. As shown below, software investors have seen this a few times, such as in early 2020, when IGV fell more than 25% from its highs while trailing-twelve-month EPS declined roughly 15%. A similar pattern emerged during the ‘Tariff Tantrum’ in early 2025, when prices dropped by more 25%, but trailing earnings declined a little more than 5%.

In these cases, the industry took 16 and 31 weeks, respectively, to recover from its price declines. Additionally, the trough of the drawdown occurred 6 weeks and 18 weeks into the drawdown, respectively.

The other two bear markets for software have been driven largely by negative realized earnings. During late 2018, prices declined 21% from highs, and EPS declined 26%. 2022 saw price drawdown by a whopping -45%, with EPS dropping a similar -46%. In these cases, IGV took 26 and 118 weeks, respectively, to recover the price drawdown.

It’s worth noting, however, that during both of these earnings drawdown periods for software, broader market indices, such as the Nasdaq 100, also entered bear market territory.

The table above summarizes key data from the chart – and it’s clear in its summary. 2026’s IGV drawdown length (22 weeks) has eclipsed the trough duration of recent price scares, and this year’s price deterioration (30%) is deeper than either 2020 or 2025. Where are we relative to an earnings-led drawdown? Shorter and shallower than average, so far. Those drawdowns troughed, on average, in week 32, with a 33% average drawdown. Only time will tell how the Tech Wreck of 2026 takes shape.

Software’s Selloff has continued as of late, with the industry now in a roughly 30% drawdown. We’re witnessing the fifth bear market for the industry in the prior eight years – and perhaps there are lessons to be learned from this recent history. Price scares recover quicker than earnings-led drawdowns. But 2026’s drawdown is both longer and harsher than recent price scares, suggesting that the industry’s earnings may be about to take a hit.

For more content by Blake Anderson, CFA®, Associate Portfolio Manager click here.

8774521.1. – 17FEB26A